26 Best Robo-Advisors for Automated Investing in 2026

Robo-advisors are algorithm-driven investment platforms that build and manage diversified portfolios on your behalf, typically at a fraction of the cost of a human financial advisor. This directory covers US, UK, Canadian, European, and Asia-Pacific platforms spanning fully automated services to hybrid human-plus-algorithm models. Pricing and availability are verified as of March 2026, and six platforms that shut down between 2022 and early 2026 have been removed from this list.

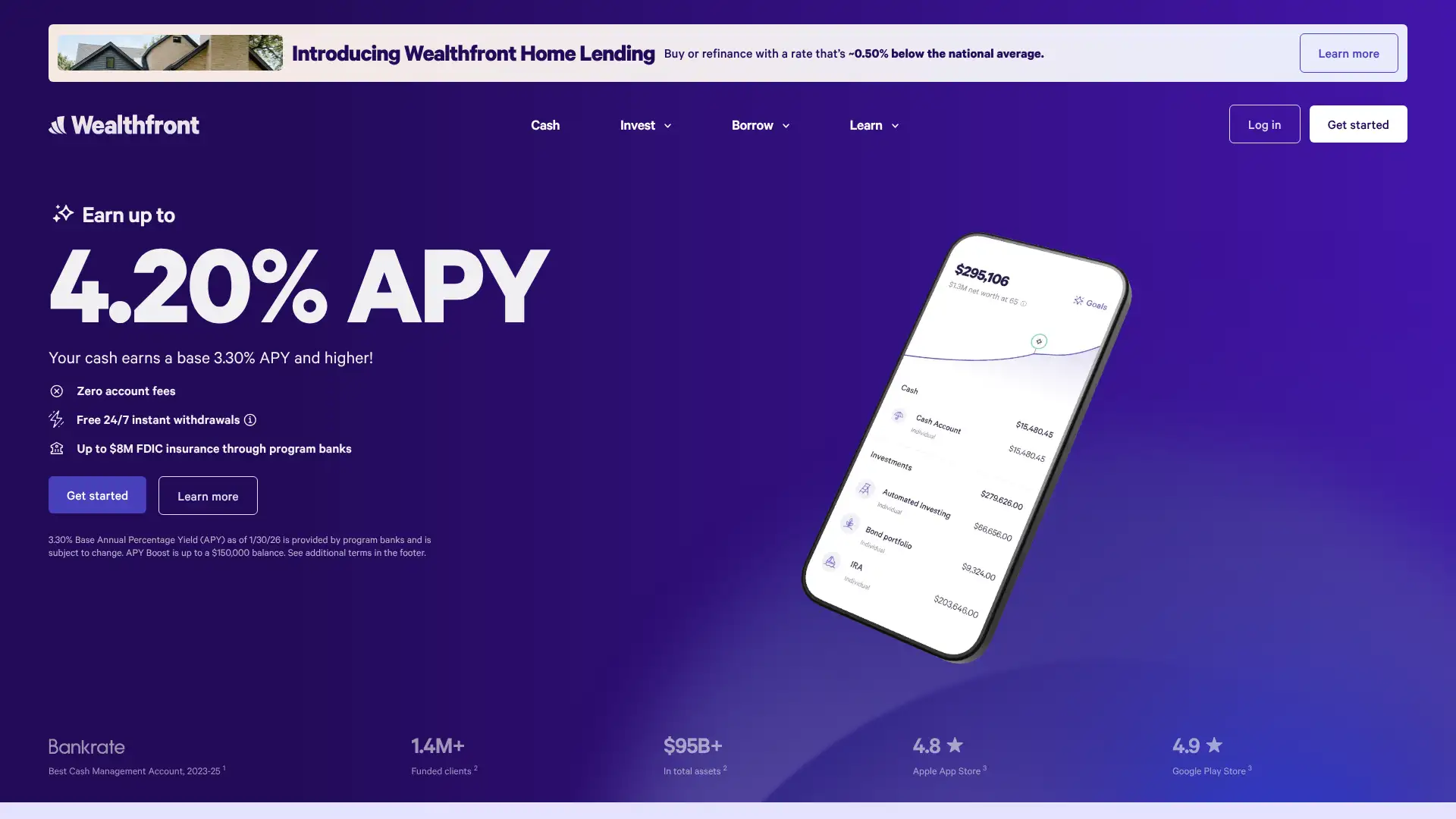

Wealthfront

Wealthfront manages over $90 billion for roughly 1.3 million clients and has repeatedly ranked at or near the top of NerdWallet's robo-advisor rankings since 2022, winning its Best Portfolio Options award in 2026. The platform charges a flat 0.25% annual advisory fee on all invested assets, with a $500 minimum to open an automated investing account. Tax-loss harvesting runs daily on taxable accounts, and accounts over $100,000 can access direct indexing, which Wealthfront claims has covered the advisory fee more than 6x over for typical clients. In late 2025 Wealthfront launched a mortgage lending service in California, Colorado, and Texas, extending its financial ecosystem well beyond investing.

- • Daily tax-loss harvesting: automatically sells underperforming ETFs and replaces them with equivalents to generate tax savings, available on all taxable accounts

- • Direct indexing: accounts over $100,000 can hold individual stocks instead of a US equities ETF, unlocking more tax-harvesting opportunities

- • Path financial planning tool: free retirement and goal-planning simulator that pulls in outside account data

- • 529 college savings plans: one of the few robo-advisors offering a fully automated 529, managed in a Nevada-sponsored plan at 0.42-0.46% total fees

- • Portfolio line of credit: borrow up to 30% of your account value at competitive rates against your invested portfolio

Wealthfront is the strongest pick for US investors with $500 or more who want sophisticated, fully automated tax optimization without paying for human advisors. The flat 0.25% fee is fair at any balance, and direct indexing at $100k+ is genuinely differentiated. Skip it if you have only a few hundred dollars to start or if you want to speak to a financial planner.

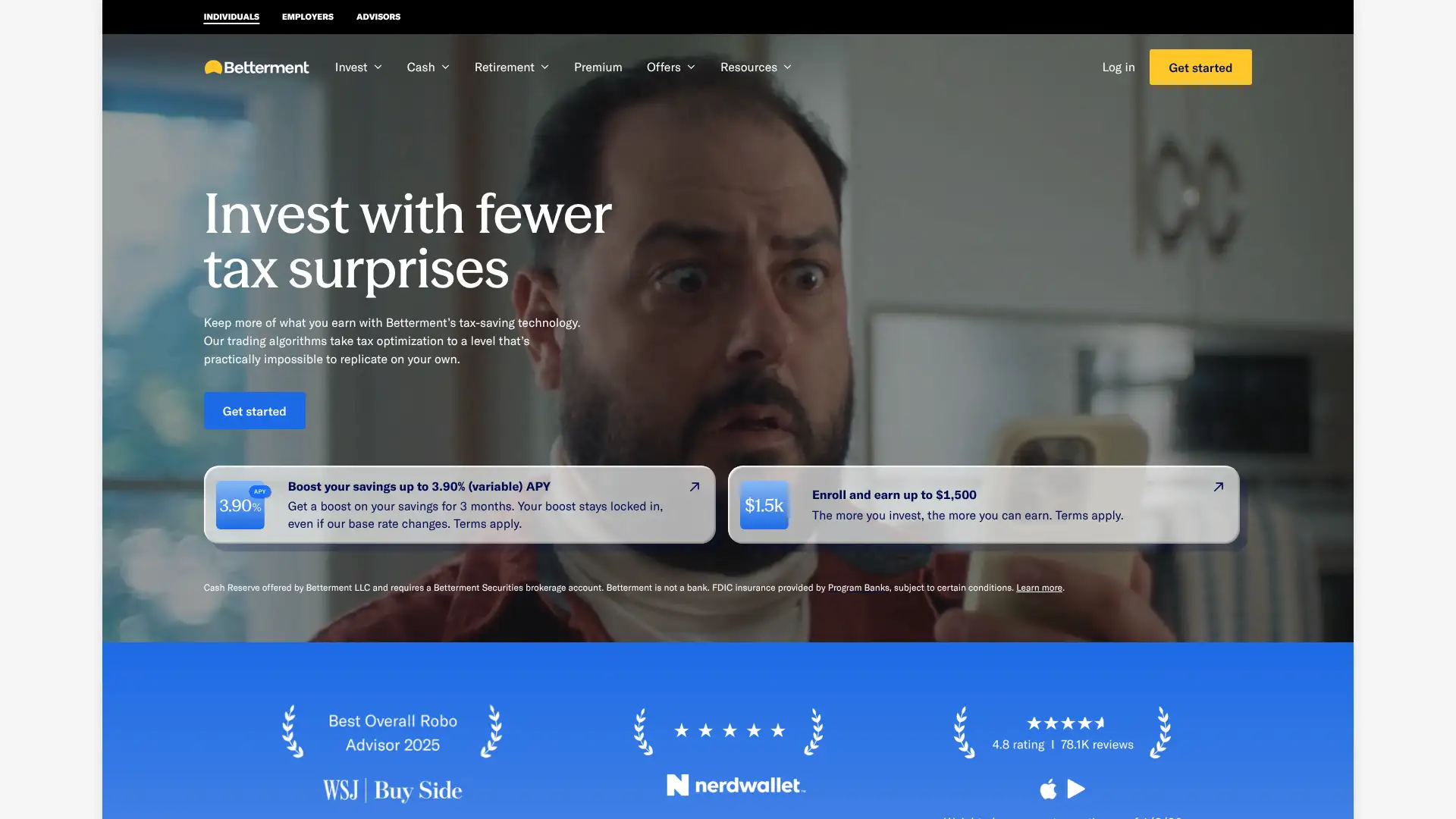

Betterment

Betterment is the largest independent digital financial advisor in the US, managing over $55 billion for more than 900,000 customers as of early 2025. It operates on a tiered fee structure: $4 per month for accounts under $20,000 (unless you set up $250+ in recurring monthly deposits), then 0.25% annually above that threshold. In early 2025, Betterment acquired Ellevest's automated investing accounts and in 2024 absorbed Goldman Sachs Marcus Invest, cementing its position as the consolidation hub for the industry. The platform offers tax-loss harvesting on all taxable accounts, goal-based investing, and a Crypto ETF portfolio (1% fee) invested in spot Bitcoin and Ethereum ETFs. Premium tier clients with $100,000+ pay 0.65% annually for unlimited CFP access.

- • Tax-loss harvesting: automated on all taxable accounts at no extra charge, with fractional shares ensuring every dollar is invested

- • Tax-coordinated portfolio: bonds and income-generating assets are placed in IRAs while stocks go in taxable accounts to reduce overall tax drag

- • RetireGuide: free retirement planning tool that synthesizes multiple linked accounts into a single projection

- • Crypto ETF portfolio: an automated portfolio holding spot Bitcoin and Ethereum ETFs, rebalanced to market cap weights, available to all Digital clients

- • CFP access on Premium: unlimited phone and email consultations with Certified Financial Planners, included in the 0.65% annual fee above $100,000

Betterment works best for investors who expect to quickly cross the $20,000 threshold where the fee converts from $4/month to a competitive 0.25% annually, or who want Crypto ETF exposure within a managed account. For balances that will stay small, Fidelity Go or SoFi are cheaper; for tax-advanced investors above $100k, Wealthfront's direct indexing and flat fee structure are stronger.

Schwab Intelligent Portfolios

Schwab Intelligent Portfolios charges no advisory fee and no trading commissions for its standard digital-only service, making it one of the few genuinely free robo-advisors in the US. Schwab earns revenue instead through the cash allocation built into every portfolio (typically around 10% in cash swept to Schwab Bank) and through ETF management fees on its proprietary funds. The platform requires a $5,000 minimum and builds portfolios from approximately 51 ETFs across more than 20 asset classes. Tax-loss harvesting is available for accounts over $50,000. Notably, in early 2026 Schwab discontinued its Intelligent Portfolios Premium tier, which had offered unlimited CFP access for a $300 one-time fee plus $30/month, citing profitability pressures in the hybrid advice model.

- • Zero advisory fee on the standard tier: no management, rebalancing, or commission charges, which is rare among robo-advisors

- • 20+ asset classes: portfolios include US and international equities, fixed income, commodities, and real estate, spanning roughly 51 ETFs

- • Automatic daily rebalancing: portfolio is monitored and rebalanced whenever allocations drift outside their target bands

- • Tax-loss harvesting: available for taxable accounts above $50,000 with manual opt-in; harvesting can offset up to $3,000 of ordinary income annually

- • Schwab branch access: 300+ US branches for in-person support alongside digital account management, unique among major robo-advisors

Schwab Intelligent Portfolios is ideal for cost-focused investors above $5,000 who are comfortable with a meaningful cash allocation in their portfolio and don't need a human advisor. The $0 advisory fee is compelling, but the cash drag is a hidden cost worth quantifying for your specific portfolio size and risk tolerance. With Premium discontinued, it is a weaker choice for anyone who values CFP access.

Fidelity Go

Fidelity Go is the robo-advisor arm of Fidelity Investments, one of the largest financial services companies in the US. It charges no advisory fee on balances under $25,000, and a flat 0.35% annually once the balance crosses that threshold. Unlike most robo-advisors, Fidelity Go invests exclusively in Fidelity Flex mutual funds, which carry zero expense ratios themselves, meaning investors below $25,000 pay nothing at all in fees. There is no account minimum to open, and investing begins with as little as $10. Kiplinger named Fidelity Go the Best Robo-Advisor of 2025 in its annual survey. Above $25,000, clients gain access to unlimited 1-on-1 coaching sessions with licensed Fidelity advisors.

- • Zero fees under $25,000: no advisory fee and Fidelity Flex funds charge zero expense ratios, making the true all-in cost $0 for smaller accounts

- • Human portfolio oversight: investment decisions are managed by Strategic Advisers LLC (a Fidelity subsidiary), not a pure algorithm

- • 16 portfolio options: eight taxable and eight retirement portfolios covering domestic, foreign, bond, and short-term asset classes

- • Unlimited coaching sessions above $25,000: 30-minute 1-on-1 calls with Fidelity advisors covering retirement, debt payoff, and financial planning

- • Tax-loss harvesting on taxable accounts above $25,000, using the proprietary Flex fund lineup

Fidelity Go is the best robo-advisor for investors under $25,000 because zero fees and zero expense ratios make the math unambiguous. Above $25,000, the 0.35% fee is slightly above competitors, but the unlimited coaching sessions partially justify the premium. Best for existing Fidelity customers who already have their banking, 401(k), and brokerage there.

Vanguard Digital Advisor

Vanguard Digital Advisor is the robo-advisory service from Vanguard, the firm that manages over $10 trillion in assets and pioneered index fund investing in 1975. The service charges a gross advisory fee of 0.20%, but credits back ETF expense ratios paid to Vanguard affiliates, resulting in a net advisory fee of approximately 0.15% annually. Morningstar ranked Vanguard Digital Advisor first overall in its 2025 Robo-Advisor Landscape report, the same ranking it received in 2022 and 2023. The $100 minimum (for IRAs) and 90-day fee waiver for new accounts make it accessible. Clients who grow to $50,000 can upgrade to Vanguard Personal Advisor at a net 0.30% fee with dedicated CFP access.

- • All-in fee of ~0.15%: among the lowest total cost of any managed robo-advisor when advisory fee and ETF expense ratios are combined

- • Morningstar #1 overall ranking in 2025: evaluated on price, process, provider quality, and breadth of services across 16 robo-advisors

- • ESG portfolio option: launched as an alternative portfolio selection alongside All-Index and Active/Index strategies

- • Tax-loss harvesting on taxable accounts and fractional share trading: introduced in recent platform updates

- • Upgrade path to Personal Advisor: seamless transition to a hybrid human-plus-algorithm service at $50,000 with dedicated CFPs

Vanguard Digital Advisor is the best choice for fee-obsessed, long-term investors who want the Morningstar-top-ranked platform at roughly 0.15% all-in. The limited fund universe is a real constraint, but for investors who trust Vanguard's index-fund philosophy, there is no cheaper managed alternative among major US robo-advisors.

SoFi Automated Investing

SoFi Automated Investing charges a 0.25% annual management fee, introduced in November 2024 after several years of operating fee-free. Portfolios are built in collaboration with BlackRock and come in three themes: Classic (low-cost stock and bond ETFs), Classic with Alternatives (adds real estate and private markets), and Sustainable. SoFi members get a complimentary 30-minute session with a Certified Financial Planner; SoFi Plus subscribers get unlimited CFP access. The platform requires a $50 minimum, and a 1% IRA match on rollovers and contributions is available for both automated and active accounts. SoFi also charges a $100 outgoing transfer fee, which is steep compared to most competitors.

- • BlackRock-managed portfolios: investment committee includes BlackRock, with three distinct themes including alternatives and sustainable investing

- • 1% IRA match: SoFi matches 1% of IRA contributions and rollovers, available in both automated and active accounts

- • Complimentary CFP session: all SoFi members get one 30-minute session with a certified financial planner, regardless of account size

- • SoFi ecosystem integration: connects with SoFi banking, credit cards, loans, and student refinancing in one app

- • Automatic rebalancing: quarterly and dividend-driven rebalancing is included at no additional cost

SoFi Automated Investing makes sense for existing SoFi members who value the integrated financial ecosystem and the IRA match. For standalone robo-advisor use, Wealthfront or Betterment offer more features at the same 0.25% cost, particularly tax-loss harvesting which SoFi lacks entirely.

M1 Finance

M1 Finance bills itself as a Finance Super App combining brokerage, automated investing, and high-yield cash. The platform uses a 'Pie' system where each portfolio is a custom slice of ETFs and stocks, automatically invested and rebalanced via Dynamic Rebalancing. As of March 2026, M1 manages approximately $10 billion in assets for over 320,000 users. There are no trading or management fees, but a $3/month platform fee applies unless your total M1 assets exceed $10,000 or you have an active M1 Personal Loan. The high-yield cash account earns 4.00% APY. A $100 outgoing ACAT transfer fee and a $100 IRA termination fee apply if you close accounts.

- • Pie investing system: build a portfolio from any combination of stocks, ETFs, and pre-built expert pies; each deposit auto-fills slices proportionally

- • Dynamic Rebalancing: deposits and dividends are directed to underweight slices rather than triggering forced sell trades

- • Two trading windows: morning (9:30am ET) and afternoon (3:00pm ET) windows; accounts above $25,000 equity can use both

- • 14 cryptocurrencies available through a separate Crypto Account powered by Bakkt, including Bitcoin, Ethereum, and Solana

- • M1 Borrow: margin loans available on accounts with at least $2,000 invested at competitive rates

M1 Finance is the best choice for investors above $10,000 who want custom portfolio automation with zero fees and believe in a buy-and-hold philosophy. It is not a good fit for beginners with small balances (the $3/month fee is punishing), active traders who need real-time execution, or investors who want tax-loss harvesting without manual effort.

Acorns

Acorns uses a flat monthly subscription model with three tiers: Bronze ($3/month), Silver ($6/month), and Gold ($12/month). The platform's signature feature is Round-Ups, which rounds card purchases to the nearest dollar and invests the difference once $5 accumulates. Acorns manages portfolios of low-cost ETFs with expense ratios typically between 0.04% and 0.22%. The Gold plan adds a 3% IRA match on new contributions in the first year, kids' investment accounts (Early Invest), and a $10,000 life insurance policy. No advisor access is offered on any tier. The flat fee structure becomes relatively expensive as a percentage of assets for small accounts: at $3/month, a $500 portfolio is paying 7.2% annually in fees.

- • Round-Ups: automatically rounds linked card purchases to the nearest dollar and invests the spare change once it reaches $5

- • ESG portfolio option: socially responsible portfolio built from ETFs screened for environmental, social, and governance criteria

- • Acorns Early Invest: UTMA/UGMA custodial accounts for children, available exclusively on the Gold plan

- • 3% IRA match on Gold: new contributions during the first year receive a 3% match, potentially adding up to $225 for someone maxing out their annual IRA limit

- • Bitcoin ETF access: Gold subscribers can add a Bitcoin ETF allocation to their portfolio

Acorns is a useful first step for absolute beginners who wouldn't invest anything without a frictionless nudge mechanism, but it is not a long-term home for serious wealth building. Once your balance exceeds roughly $14,400, the Bronze plan's $3/month fee equals 0.25% annually, at which point Betterment or Wealthfront offer far better features for the same effective cost.

Stash

Stash is a hybrid platform combining a guided brokerage account with an automated Smart Portfolio robo-advisor, all for a flat monthly subscription. It offers two plans: Stash Growth ($3/month) and Stash+ ($9/month). Stash Growth includes a personal and Roth IRA with automated Smart Portfolio management, banking with the Stock-Back debit card, budgeting, and access to a registered financial advisor for guidance. Stash+ adds custodial investment accounts for kids and a $10,000 life insurance benefit. Stash has over 1.2 million users. The Smart Portfolio does not support IRAs, meaning IRA automation must be handled separately. A $75 ACAT fee applies to outgoing account transfers.

- • Smart Portfolio: automated, diversified robo-advisor portfolio with ETF expense ratios averaging 0.06-0.08%, rebalanced automatically

- • Stock-Back debit card: earns fractional shares in companies you shop at as rewards (e.g., buying at Amazon earns Amazon stock)

- • Guided stock and ETF investing: access to thousands of stocks and ETFs with in-app educational context for each investment

- • Registered Financial Advisor access: Stash Growth subscribers can consult a registered financial advisor for investment guidance

- • Recurring investments: set automated weekly or monthly contributions to any stock, ETF, or Smart Portfolio

Stash makes sense for investors who want to learn investing hands-on while having an automated portfolio safety net, all in one app. It is not the right choice for anyone focused purely on robo-advisor portfolio optimization or tax efficiency. Once your balance outgrows the $3/month fee structure, migrating to Betterment or Fidelity Go will be the more cost-effective path.

Empower Personal Strategy

Empower (formerly Personal Capital) is a digital wealth manager that pairs algorithm-driven portfolio management with dedicated human financial advisors. It requires a $100,000 minimum and charges 0.89% annually on the first $1 million, declining to 0.79% between $1M and $3M, and to 0.49% above $10M. The platform is best known for its free Personal Dashboard, which aggregates all financial accounts into one view and is used by millions of people even without a managed account. Portfolio management uses ETFs and, above $200,000, individual stocks for enhanced tax-loss harvesting. Estate planning, personalized tax strategies, and alternative asset access are available above $1 million.

- • Free Personal Dashboard: aggregates bank, investment, and debt accounts across institutions into one net worth view with fee analysis and retirement projections

- • Smart Weighting: proprietary portfolio methodology that re-weights holdings to reduce over-concentration in mega-cap stocks versus standard index weighting

- • Dedicated advisor team: all clients receive access to financial advisors (dedicated pair above $250,000) who are fiduciaries

- • Tax optimization: asset location, tax-loss harvesting, and personalized tax planning strategies included in the advisory fee

- • Alternative assets and private equity: available above $5 million balance for diversification beyond public equities and bonds

Empower is the right choice for high-net-worth investors above $250,000 who want the discipline of a robo-advisor combined with the personalized guidance of a dedicated fiduciary advisor. The 0.89% fee is hard to justify below that threshold when Betterment or Vanguard offer hybrid access for far less. The free Dashboard is worth using regardless of whether you open a managed account.

Ally Invest Robo Portfolios

Ally Invest Robo Portfolios offers two distinct structures: a Cash-Enhanced portfolio with no advisory fee (30% in interest-earning cash) and a Market-Focused portfolio charging 0.30% annually with approximately 2% in cash. Both require only a $100 minimum and are available as individual, joint, IRA, and custodial accounts. The platform supports four portfolio themes: Core (globally diversified), Income (higher dividends, conservative bias), Socially Responsible, and Tax-Optimized. Ally's seamless integration with Ally Bank accounts is its primary competitive advantage, allowing direct transfers with no delays. There is no tax-loss harvesting and no access to human financial advisors within the robo service.

- • Cash-Enhanced Portfolio: zero advisory fee with 30% interest-earning cash buffer, suitable for near-retirement investors who want stability

- • Four portfolio themes: Core, Income, Socially Responsible, and Tax-Optimized strategies for different investor priorities

- • Ally Bank integration: one-stop shop for banking and investing with instant fund transfers between accounts

- • Low $100 minimum: one of the lowest entry points for any robo-advisor offering multiple account types including IRAs and custodial accounts

- • Automatic rebalancing: portfolios are monitored daily and rebalanced after withdrawals to maintain target allocation

Ally Invest Robo Portfolios is a reasonable choice for existing Ally Bank customers who want seamless banking-to-investing integration and are comfortable with either the 30% cash allocation or the 0.30% market-focused fee. As a standalone robo-advisor for new investors, Betterment or Fidelity Go are better options.

Interactive Advisors

Interactive Advisors is the robo-advisory arm of Interactive Brokers, the global brokerage firm with approximately $14 trillion in client equity. Clients invest in portfolios managed by third-party portfolio managers, who are registered investment advisors running strategies on the Interactive Advisors marketplace. Management fees range from 0.10% to 0.75% annually depending on the portfolio, with Interactive Advisors retaining 0.25% and passing the rest to the portfolio manager. Over 70 portfolios are available, with minimums as low as $100 for some strategies. A key differentiator is that all investments are held in the client's own Interactive Brokers brokerage account, providing full transparency and custody control.

- • Third-party portfolio manager marketplace: roughly 70 professionally managed strategies available, ranging from passive ETF portfolios to active stock-picking approaches

- • Co-trading technology: portfolio manager trades are replicated in the client's own brokerage account in real time

- • All investments held in client's own IBKR account: full custody transparency with no funds commingled

- • International availability: accessible to investors in the US, Switzerland, and select other countries with an IBKR account

- • Low minimum entry: some portfolios require as little as $100, though minimums vary by strategy

Interactive Advisors is best for investors who already use Interactive Brokers, want access to actively managed strategies beyond index funds, and are comfortable navigating a complex marketplace. For most consumers seeking simple automated investing, any of the major US robo-advisors offers a better user experience.

Wealthsimple

Wealthsimple is Canada's largest robo-advisor and digital wealth manager, serving over 3 million clients and managing assets that surpassed $100 billion (CAD) by October 2025. The company operates three tiers based on total assets: Core (under $100,000 at 0.50%), Premium ($100,000-$499,999 at 0.40%), and Generation ($500,000+ at 0.20-0.40%). All accounts support TFSAs, RRSPs, FHSAs, RESPs, LIRAs, and non-registered accounts, the most comprehensive registered account coverage of any Canadian robo-advisor. Wealthsimple has diversified aggressively into cryptocurrency trading, direct indexing, private assets, and mortgage services, though these expansions have drawn criticism from users who valued its original low-cost passive investing focus.

- • Halal and SRI portfolios: ethical investing options including a Shariah-compliant portfolio and ESG-screened socially responsible portfolios

- • Summit Portfolio: launched for high-balance clients, combining ETFs with private asset exposure including a private infrastructure fund

- • Self-directed trading: commission-free stock and ETF trading alongside the managed portfolio, all within the same app

- • FHSA support: First Home Savings Account is available on all tiers, supporting Canadian first-time homebuyer savings

- • Fractional shares and zero trading commissions: available on the self-directed side, including for Wealthsimple's own clients

Wealthsimple remains the most convenient and feature-complete Canadian robo-advisor for investors who value a single app covering managed investing, self-directed trading, and every registered account type. Cost-focused investors with balances under $100,000 should compare Questwealth's 0.20% fee structure before committing.

SigFig

SigFig is a hybrid robo-advisor that manages investments held in partner brokerage accounts rather than opening a new custodial account. Clients connect their existing Fidelity or Charles Schwab accounts, and SigFig overlays its management on those assets. A $2,000 minimum is required, and accounts up to $10,000 are managed for free; above $10,000, the fee is 0.25% annually, in line with industry benchmarks. SigFig also offers a free Portfolio Tracker that analyzes up to any number of linked accounts for fee analysis and asset allocation, available without a managed account. Unlimited access to human investment advisors is included for all paid clients, a differentiator at this price point.

- • Partner brokerage model: assets remain in your existing Fidelity or Schwab account; SigFig overlays management without requiring a transfer

- • Free management on first $10,000: unique among US robo-advisors with a meaningful waiver for early account growth

- • Unlimited human advisor access: all paid clients can schedule calls with investment advisors at no extra charge

- • Tax-loss harvesting: available on taxable accounts alongside automatic rebalancing

- • Free Portfolio Tracker: syncs with 3,000+ financial institutions to analyze holdings, fees, and asset allocation

SigFig is best suited to investors who already use Fidelity or Schwab and prefer to add automated management to existing accounts without moving assets. The free first $10,000 and unlimited advisor access are genuine advantages. For investors starting fresh, most major robo-advisors offer a smoother experience and lower minimums.

Axos Invest

Axos Invest is the robo-advisory arm of Axos Financial, operating since 2019 after the acquisition of WiseBanyan. The platform charges a flat 0.24% annual advisory fee on accounts above $500, with a $1/month fee if the balance falls below that threshold. It offers Managed Portfolios with over 30 asset class options including US and international equities, corporate bonds, high-yield bonds, real estate, inflation-protected securities, and commodities. Investors can accept the algorithm's recommended portfolio, modify it, or build a completely custom Pie from scratch. Self-directed trading (commission-free stocks and ETFs) is available alongside the managed accounts in the same platform. Tax-loss harvesting requires a $25,000 minimum and an additional 0.20% annual fee.

- • Portfolio Plus customization: investors can add or remove individual ETFs across 32 asset class categories without additional charges

- • 30+ asset classes: one of the broadest investment menus of any US robo-advisor, including high-yield bonds, REITs, commodities, and inflation-protected securities

- • IRAutomation: automatically optimizes IRA contribution and investment decisions on a recurring basis

- • Commission-free self-directed trading: buy and sell stocks and ETFs at no cost alongside the managed portfolio

- • Axos Bank integration: direct deposit up to two days early, seamless transfers between bank and investment accounts

Axos Invest is a solid choice for investors who want unusual asset class diversification (commodities, high-yield bonds, REITs) in a customizable robo-advisor wrapper. The base 0.24% fee is reasonable, but the tax-loss harvesting surcharge makes the TLH-enabled fee 0.44%, at which point competitors are better value. Best for investors who won't use TLH and value the customization.

WealthNavi

WealthNavi is Japan's largest robo-advisor by assets under management, managing over ¥1.8 trillion (approximately $12 billion USD) for 450,000 active users as of January 2026. The platform invests in a globally diversified portfolio of seven ETFs from providers including Vanguard, iShares, and State Street, covering US equities, non-US equities, bonds, real estate, gold, and more. In December 2024, Mitsubishi UFJ Financial Group (MUFG) acquired WealthNavi for approximately ¥99.7 billion ($664 million), cementing its status as the dominant digital wealth management platform in Japan. The standard fee is 1.0% annually (1.1% with Japanese consumption tax); clients using NISA tax-exempt accounts pay a weighted average of 0.63-0.67% depending on risk tolerance.

- • Robo-NISA: fully automated use of Japan's NISA tax-exemption system, investing regular deposits in a diversified ETF portfolio inside a tax-free account

- • DeTAX (automated tax optimization): proprietary patented algorithm that identifies and harvests tax losses to reduce the client's Japanese tax liability

- • Five risk levels: clients choose from risk 1 (conservative) to risk 5 (aggressive) through a five-question questionnaire, with the algorithm managing the resulting ETF mix

- • MUFG backing: acquired by Japan's largest bank in December 2024, providing deep institutional backing for the platform's long-term stability

- • AI wealth management advice: in-app guidance on savings goals, contribution amounts, and risk adjustments

WealthNavi is the obvious first choice for Japanese retail investors wanting passive global diversification in a NISA account with automated tax optimization. The 1.0% fee is market-standard for Japan and the MUFG acquisition ensures institutional permanence. Non-Japanese investors should look elsewhere.

Nutmeg

Nutmeg was the UK's first digital wealth manager, launched in 2012 and acquired by J.P. Morgan in 2021. As of late 2025, J.P. Morgan has announced the Nutmeg brand will be retired and migrated to J.P. Morgan Personal Investing, with the transition underway through 2026. Nutmeg grew to over £8.5 billion in AUM and 150,000+ clients before the rebrand. Four portfolio styles are available: Fully Managed (0.75% up to £100k, 0.35% above), Smart Alpha (powered by J.P. Morgan Asset Management), Fixed Allocation, and Thematic. Clients above £250,000 gain access to dedicated relationship managers. Account types include Stocks and Shares ISA, Lifetime ISA, Junior ISA, SIPP, and GIA.

- • Lifetime ISA (LISA): one of the few UK robo-advisors offering a LISA, allowing first-time buyers and retirement savers to receive a 25% government bonus on contributions

- • Smart Alpha portfolios: powered by J.P. Morgan Asset Management algorithms, providing an additional layer of active factor-based investment management

- • Thematic portfolios: launched in 2024, covering investment themes like Technological Innovation and Resource Transformation within a managed account framework

- • Free guidance sessions: all clients can book a session with a Nutmeg Wealth Manager at no additional charge

- • FCA regulated and FSCS covered: client assets are protected up to £85,000 under the UK Financial Services Compensation Scheme

Nutmeg remains a strong UK robo-advisor with broad account type coverage and genuine portfolio variety, but the brand migration to J.P. Morgan Personal Investing introduces short-term uncertainty. For investors committed to the UK market, checking the current J.P. Morgan Personal Investing fee structure before opening a new account is advisable.

Moneybox

Moneybox is a UK savings and investment app founded in 2015, best known for its Round-Up feature that invests spare change from card transactions. The platform has over 250,000 users and offers three ready-made investment portfolios (Cautious, Balanced, Adventurous) plus DIY fund and stock access. Fees consist of a £1/month subscription (free for the first three months, waived for users with £5,000+ in a Moneybox Cash ISA or Simple Saver) plus a 0.45% annual platform fee. Pension accounts carry a reduced 0.15% platform fee on balances over £100,000. Account types include Stocks and Shares ISA, Lifetime ISA, Junior ISA, Personal Pension, and GIA, making Moneybox one of the most account-complete beginner platforms in the UK.

- • Round-Ups: links to debit/credit cards and automatically rounds up purchases, investing the difference once £1 accumulates

- • Lifetime ISA: available for first-time buyers and retirement savers, with the 25% government bonus applied automatically

- • Personal Pension: automated pension with automatic rebalancing and a simplified drawdown option as the client approaches retirement

- • US stock fractional shares: commission-free access to 20 major US stocks including Apple, Tesla, and Google through fractional share investing

- • 3% AER Cash ISA: the Moneybox Cash ISA offers competitive cash interest alongside the investing options

Moneybox is the best UK savings-to-investing gateway for beginners who respond well to automated nudges. The Round-Up feature, Lifetime ISA, and pension in one app justify the slightly higher fee structure for new investors who might not invest at all without the friction-reducing tools. Investors above £10,000 should review whether cheaper platforms like InvestEngine better suit their evolving needs.

Scalable Capital

Scalable Capital is one of Europe's largest fintech investment platforms, headquartered in Munich and regulated by BaFin. It offers two distinct products: a digital wealth management (robo-advisor) service charging 0.75% annually, and a brokerage service under the FREE and PRIME+ models. The FREE broker charges €0.99 per trade (free for ETF savings plans); PRIME+ offers unlimited trades above €250 for a flat €4.99/month. Uninvested cash earns 2.50% APY on both plans. Assets are custodied by Baader Bank, a regulated German institution, with deposits protected up to €100,000. The platform is available in Germany, Austria, the Netherlands, Italy, Spain, France, and the UK.

- • ETF savings plans from €1: automated monthly contributions starting at €1 with no order fees, spanning stocks, ETFs, and crypto ETPs

- • Dynamic risk management: the robo-advisor uses Value at Risk (VaR) methodology to dynamically adjust portfolio allocation during periods of market stress

- • PRIME+ trading flat rate: unlimited commission-free trades above €250 for a fixed €4.99/month, appealing for active European traders

- • Interest on uninvested cash: 2.50% APY on unlimited cash balances, distributed across multiple partner banks for deposit protection

- • Multi-country availability: accessible from Germany, Austria, Netherlands, Italy, Spain, France, and the UK under a unified European regulatory framework

Scalable Capital is best suited for German and Austrian investors who want either a no-frills ETF savings plan (FREE broker) or a flat-rate unlimited trading account (PRIME+). The 0.75% robo-advisor fee is a weaker value proposition for passive investors compared to cheaper European alternatives, but the platform's breadth and regulatory standing make it one of the most credible European options.

Moneyfarm

Moneyfarm is one of Europe's largest independent digital wealth managers, with over £5 billion in AUM as of late 2025 following its acquisition of Willis Owen. The company operates in the UK and Italy under FCA regulation and offers three portfolio management styles: actively managed (fees starting at 0.45% for up to £50,000, declining to 0% above £1.5 million), fixed allocation (0.15% flat), and Liquidity+ (0.30% platform + 0.05% management for short-duration investments). In August 2025, Moneyfarm restructured its pricing into three Wealth tiers: Core (digital advice), Premium (investment consultant access above certain thresholds), and Private (dedicated Wealth Manager at £12.99/month add-on or by AUM threshold). Fund costs average 0.16% annually on top of the management fee.

- • Seven risk-rated portfolios: actively managed portfolios across seven risk levels from very conservative to very aggressive, reviewed quarterly by the investment team

- • Fixed Allocation portfolios: passively managed strategy with annual rebalancing, launched in 2022 as the lower-cost alternative to active management

- • Investment Consultant access: Premium and Private tier clients can book calls with dedicated investment consultants for portfolio discussion and guidance

- • DIY Share Investing: available within ISA or GIA accounts; £3.95 per trade for UK stocks, funds, and ETFs; 0.35% custody fee (capped at £45/year) for ISA holders

- • Liquidity+ short-term portfolio: invested in money market funds for low-risk capital preservation, suitable for 2-year or shorter time horizons

Moneyfarm offers good value for UK investors with £50,000 or more who want active portfolio management alongside investment consultant access, especially given the sharp fee reductions above that threshold. For balances under £50,000, the combined ~0.86% all-in cost is less competitive than InvestEngine or Vanguard UK's passive alternatives.

Sarwa

Sarwa is the UAE's leading robo-advisor, founded in 2017 and dual-regulated by the Dubai Financial Services Authority (DFSA) and the Financial Services Regulatory Authority (FSRA) in Abu Dhabi. The platform serves investors in the UAE, Kuwait, Bahrain, and Saudi Arabia with over $800 million in AUM. It offers four investment strategies: Conventional, Socially Responsible, Halal (Shariah-compliant), and Crypto (5% Bitcoin ETF allocation within a broader portfolio). Management fees range from 0.40% to 0.85% depending on account size, with a $500 minimum and no withdrawal or local transfer fees. Portfolios are built from Vanguard and iShares ETFs and custodied at Saxo Bank. Sarwa is expanding in 2026 with a desktop application and open banking funding.

- • Halal portfolio: Shariah-compliant investment strategy excluding interest-based institutions, alcohol, gambling, and other prohibited sectors, supervised internally

- • Socially Responsible portfolio: ESG-screened ETFs for investors who want to align investments with environmental and social values; minimum $2,500

- • Sarwa Save: high-yield cash account in USD with no lock-in period and competitive yield, useful for MENA investors holding US dollar savings

- • Dual DFSA and FSRA regulation: dual regulatory oversight provides strong investor protection standards in the UAE financial ecosystem

- • Automatic rebalancing and dividend reinvestment: all Sarwa Invest portfolios include rebalancing and reinvestment at no additional charge

Sarwa is the best choice for UAE and MENA investors seeking a regulated, fully automated robo-advisor with a genuine Halal portfolio option. The dual regulatory oversight and institutional backing are reassuring in a market with fewer investor protections than the US or UK. The 0.85% fee on small accounts is the primary drawback relative to global benchmarks.

Syfe

Syfe is a Singapore-based robo-advisor founded in 2019 and regulated by the Monetary Authority of Singapore (MAS) under a Capital Markets Services Licence. The platform offers multiple portfolio types: Core (globally diversified ETF portfolios), REIT+ (focused on Singapore REITs tracking the SGX iEdge S-REIT Leaders Index), Income+ (high-yield bonds and dividend equities), and Custom portfolios. Management fees are tiered by AUM: 0.65% for under S$50,000, declining to 0.25% above S$5 million. There is no minimum investment, and SRS (Supplementary Retirement Scheme) funds are accepted. Assets are held with HSBC Institutional Trust Services as custodian.

- • REIT+ portfolio: Singapore-focused real estate investment trust portfolio tracking the SGX iEdge S-REIT Leaders Index, unique among major Singapore robo-advisors

- • Income+ portfolio: designed for regular income distribution with a blend of high-yield bonds and dividend-paying equities, targeting monthly payouts

- • SRS investing: supports Supplementary Retirement Scheme funds, allowing tax-deductible contributions to be invested through the robo-advisor

- • Cash+ account: short-duration bond fund cash management account with competitive yield and no lock-in, separate from investment portfolios

- • No minimum investment: unlike Endowus ($1,000 minimum), Syfe allows investors to start with any amount in SGD

Syfe is the best Singapore robo-advisor for investors who want REIT exposure or a passive income-oriented portfolio alongside a standard globally diversified core holding. For CPF OA investing, Endowus is the only option; for the lowest all-in fees on cash portfolios, FSMOne's RSP is worth comparing.

Endowus

Endowus is Singapore's leading digital wealth manager for CPF, SRS, and cash investing, founded in 2017 and regulated by MAS. It is the only digital advisor in Singapore that allows investors to grow their CPF Ordinary Account (OA) and Special Account (SA) savings in institutional-grade unit trusts. Cash management fees range from 0.60% annually for up to S$200,000 to 0.25% above S$5 million, with a separate 0.40% annual rate for CPF and SRS portfolios. A notable feature is that Endowus rebates 100% of trailer fees (commissions paid by fund houses to distributors) back to clients, effectively reducing the net cost. The minimum investment for cash portfolios is S$1,000, with S$100 top-ups.

- • CPF OA and SA investing: only digital advisor in Singapore enabling investment of CPF Ordinary Account and Special Account savings in diversified fund portfolios

- • 100% trailer fee rebate: all fund distribution commissions (typically 0.3-0.8% annually) are passed back to clients, meaningfully reducing net investment costs

- • 300+ institutional funds: access to unit trusts from Dimensional Fund Advisors, PIMCO, Fidelity, and other institutional managers not available through retail channels

- • Cash Smart portfolio: capital preservation product investing in short-duration bond and money market funds at a flat 0.15% annual fee

- • Flagship Portfolios: globally diversified portfolios across different risk levels, benchmarked against global market indices

Endowus is the essential choice for any Singapore investor with CPF OA or SA savings who wants to invest beyond the CPF default OA 2.5% rate. The CPF access monopoly and trailer fee rebate structure make it uniquely valuable in the Singapore market. For pure cash investing, Syfe and StashAway are competitive alternatives worth comparing on fees at your expected AUM level.

StashAway

StashAway is a multi-market digital wealth manager founded in Singapore in 2016 and now operating across Singapore, Malaysia, the UAE, Bahrain, and other MENA markets. The platform is regulated by MAS in Singapore and the FSRA in Abu Dhabi. It manages investments using a proprietary framework called ERAA (Economic Regime-based Asset Allocation), which dynamically adjusts portfolio allocation based on macroeconomic data. Annual management fees range from 0.20% to 0.80% based on AUM. StashAway Simple, a cash management account, charges 0.15% annually. There is no minimum investment for managed portfolios, and a 1% IRA match equivalent (1% on SRS contributions in Singapore) is offered through partnership programs.

- • ERAA (Economic Regime-based Asset Allocation): proprietary macroeconomic framework that reallocates between equities, bonds, and defensive assets based on observed economic regimes

- • Goal-based investing: create multiple separate goal portfolios (retirement, home purchase, education) each with their own allocation and time horizon

- • Flexible Portfolios: from 2022, investors can build single-ETF portfolios from a curated list, with a flat 0.30% management fee

- • SRS investing: supports Supplementary Retirement Scheme funds in Singapore for tax-deductible contributions

- • Multi-market availability: operates across Singapore, Malaysia, UAE, Bahrain, and other regional markets under appropriate local regulation

StashAway is a strong all-around platform for Singapore and MENA investors who want macro-informed portfolio management and multi-country accessibility. The ERAA framework is a genuine differentiator, but the 0.80% starting fee is expensive for small balances. Investors growing toward S$200,000+ will see fees drop to more competitive levels. For CPF OA investing, Endowus remains the only option.

Rebellion Research

Rebellion Research is a New York-based SEC-registered investment adviser and AI research think tank founded in 2003, widely recognized as one of the first firms on Wall Street to apply artificial intelligence and Bayesian network algorithms to portfolio management, beginning in 2006. The firm is registered to operate in New York, Texas, Kentucky, and other states where registered or exempt. Rebellion Research positions itself as both an AI investment manager and a not-for-profit educational think tank focused on AI development, conference programming, and financial research. Specific retail pricing is not publicly listed; prospective clients are directed to contact the firm directly for advisory terms.

- • Bayesian network AI: pioneered machine learning investment management in 2006, using probabilistic network models to generate portfolio recommendations from macro data

- • Not-for-profit research mission: Rebellion Research operates as both an investment adviser and an educational think tank, publishing research on AI, economy, and market trends

- • Star algorithm: the proprietary AI algorithm provides a portfolio manager with a ranked list of buy/sell recommendations each morning for human execution

- • Multi-state registration: licensed to operate across several US states as an SEC-registered investment adviser under the Investment Advisers Act of 1940

- • Research and educational content: publishes articles on AI development, financial modeling, and investment strategy through its website and affiliated events

Rebellion Research is a genuinely pioneering AI investment firm but operates more as an institutional or high-net-worth advisory service than a consumer robo-advisor. Investors drawn to AI-driven investing should verify current fee structures and state registration directly with the firm before proceeding.

Titan

Titan launched in 2018 as an actively managed investment platform using hedge-fund-style stock selection, and by 2025 had pivoted significantly toward a comprehensive wealth management model pairing human advisors with automated portfolios. The current platform charges $25/month plus a 0.20% annual advisory fee on all managed investment products. This covers both free automated Stocks and Automated Bonds portfolios and actively managed strategies (Flagship, Opportunities, Offshore) built by Titan's investment team. Alternatives including venture capital, private real estate, and private credit are available through interval funds from Apollo, Carlyle, and ARK. In August 2023 Titan was fined $1 million by the SEC for advertising misleading hypothetical performance metrics.

- • Active stock strategies: Flagship (large-cap US), Opportunities (small-cap growth), and Offshore (international) are managed by Titan's investment team, not algorithms

- • Alternative asset access: Apollo real estate, Carlyle private credit, and ARK Venture Fund available to retail clients through interval fund structures

- • Smart Cash: automatically moves uninvested cash between Treasury money market funds to optimize after-tax yield

- • 1-on-1 human advisors: membership includes access to experienced financial advisors for equity compensation, liquidity events, and financial planning

- • Equity compensation focus: advisors specialize in RSU vesting, stock option decisions, and pre-IPO planning for tech professionals

Titan is best suited to high-earning tech professionals with meaningful equity compensation who value access to alternatives and specialized human advice on liquidity events. The $25/month membership is hard to justify for investors under $50,000 or those seeking straightforward passive investing, where the flat fee creates a disproportionately high effective expense ratio.