33 Best Payment Gateways and Processors for Online Stores in 2026

This directory covers the leading payment gateways and processors used by online stores worldwide, from global infrastructure giants like Stripe and Adyen to regional specialists like Razorpay, Paystack, and Mollie. Categories span full-stack processors, buy now pay later providers, open banking networks, digital wallets, and local bank transfer methods. Fees and plan details are verified as of March 2026.

Stripe

Stripe is a developer-first payment platform processing transactions for over 100 countries and supporting 135+ currencies. It powers payments for companies like Amazon, Shopify, and Zoom. Standard US processing is 2.9% + $0.30 per online card transaction with no setup or monthly fees; ACH direct debit costs 0.8% capped at $5. In 2025 Stripe introduced Smart Disputes with AI-powered chargeback response and a $15 counter fee (refundable if won). Custom pricing starts for merchants processing over $80,000 per month.

- • Stripe Radar: built-in ML fraud detection; advanced rules cost $0.07/transaction (waived on standard pricing)

- • Stripe Billing: recurring subscriptions with dunning management, proration, and metered billing at 0.5%–0.8% of revenue

- • Stripe Connect: marketplace and platform payouts with Standard, Express, and Custom tiers

- • Global payment methods: supports 100+ local methods including iDEAL, SEPA, BACS, Klarna, and Afterpay via single API

- • Instant Payouts: receive funds within minutes for 1% fee (min $0.50)

Stripe is the default starting point for any developer-led business or startup launching online payments. Its API quality and ecosystem are unmatched at any volume. As your monthly volume climbs above $100K, evaluate whether Adyen's interchange++ model offers better effective rates for your card mix.

PayPal

PayPal serves over 35 million merchants and 425 million active consumer accounts globally. It functions as both a payment gateway and processor. US merchant rates are 3.49% + $0.49 for PayPal Checkout and Venmo, 2.99% + $0.49 for standard card processing, and 2.29% + $0.09 for in-person Zettle transactions. PayPal's 2023 research found offering PayPal at checkout increased conversion by an average of 46%. International transactions add 1.5% on top of the standard rate.

- • PayPal wallet acceptance: reach 425 million active accounts who can pay with stored balance, cards, or BNPL in one click

- • Venmo for Business: accept Venmo payments at 1.9% + $0.10, reaching 92 million US Venmo users

- • Pay Later (Buy Now Pay Later): offer interest-free installments with PayPal absorbing credit risk; shown to increase purchase intent among 62% of PayPal shoppers

- • Seller Protection: covers eligible transactions against unauthorized payment claims and item-not-received disputes

- • PayPal Complete Payments: single integration for cards, PayPal, Venmo, and Pay Later in one checkout module

PayPal is essential for any US or European e-commerce store as a checkout option because consumers expect to see it — but it should not be your only processor. Run PayPal alongside a lower-cost gateway like Stripe or Shopify Payments to keep effective rates competitive.

Square

Square is used by over 4 million merchants and processed $228 billion in gross payment volume in 2024. It consolidated all business types into three unified pricing tiers in October 2025, raising the Free plan's online rate to 3.3% + $0.30. The Plus plan ($49/month) drops online processing to 2.9% + $0.30, while Premium ($149/month) offers the lowest in-person rate of 2.4% + $0.15. A notable differentiator: Square charges $0 in chargeback fees, unlike most processors that charge $15–$25 per dispute. Custom pricing is available for businesses processing over $250,000 annually.

- • Free POS software with inventory, customer management, and reporting — no monthly fee on the base plan

- • Square Reader for Contactless and Chip: hardware starts at $49; tap-to-pay on iPhone/Android requires no additional hardware

- • Square Invoices: ACH bank transfer payments at 1% (min $1, capped at $10 with Invoices Plus)

- • Afterpay BNPL at checkout: 6% + $0.30 per transaction, letting customers pay in 4 installments with Square receiving full payment upfront

- • $0 chargeback fees across all plans — a unique advantage vs. competitors charging $15–$25 per dispute

Square is the best all-in-one choice for retail and food service businesses that need tight integration between in-person and online sales. The $0 chargeback fee alone can justify choosing Square over Stripe for merchants in hospitality or services. Pure e-commerce businesses without a physical presence will find better rates elsewhere.

Adyen

Adyen is the payment platform behind Uber, Spotify, eBay, and McDonald's, processing $1.3 trillion in annual volume. It uses Interchange++ pricing — merchants pay the exact card network interchange rate, scheme fees, and Adyen's own markup (starting at $0.13 + 0.60% for Visa/Mastercard). There are no monthly, setup, or closure fees, but a minimum monthly invoice applies (typically €1,000) depending on industry. The average total fee for European consumer card transactions is approximately 1%. Adyen also supports 250+ payment methods and direct connections to card schemes in 35+ countries.

- • Interchange++ pricing passes exact interchange rates to merchants, offering full fee transparency and typically lower costs than flat-rate models at scale

- • Unified Commerce: single platform for online, in-store, and app payments with shared customer data and reporting across all channels

- • Network tokens and Adaptive Acceptance: AI-driven authorization optimization shown to increase acceptance rates — especially useful for recurring billing

- • Direct acquiring licenses in 30+ countries, reducing reliance on third-party acquirers and improving authorization rates

- • 250+ local payment methods including iDEAL, SEPA, Boleto, Alipay, and WeChat Pay via single integration

Adyen is the right choice for mid-market and enterprise businesses processing hundreds of millions in annual volume who want maximum fee transparency and global acquiring capability under one contract. Below roughly $2M/year in processing, Stripe's simplicity and zero-minimum model will almost always cost less on a total-cost basis.

Braintree

Braintree is PayPal's developer-focused payment platform, serving enterprises including Airbnb, Uber, and GitHub. It supports PayPal, Venmo, Apple Pay, Google Pay, ACH, and all major cards through a single API. Standard US card processing is 2.9% + $0.30 per transaction with no setup, monthly, or hidden fees. PayPal transactions through Braintree carry PayPal's standard rates (not Braintree's card rate). Interchange-plus pricing and custom flat rates are available for merchants processing over €60K/month in Europe or high volumes in the US. Braintree's documentation is migrating to the PayPal Developer portal as of May 2026.

- • Drop-in UI and Hosted Fields: pre-built checkout components with full PCI SAQ-A compliance that can be deployed in under 30 minutes

- • Vault: securely store customer payment methods with tokens that can be reused for subscriptions, one-click checkout, and cross-platform purchases

- • Kount fraud detection integration: advanced fraud scoring available to Braintree merchants for additional cost

- • PayPal and Venmo native checkout: enables one-touch PayPal and Venmo payments within Braintree-powered checkouts without separate integration

- • Multi-currency settlement: supports 130+ currencies; additional 1.5% fee for scheme-currency settlement, 3% for exotic currency settlement

Braintree is the most logical choice for businesses already deep in the PayPal ecosystem who want developer-grade card processing and native PayPal/Venmo support in a single integration. For net-new businesses without existing PayPal ties, Stripe's more independent ecosystem and better standalone documentation make it a stronger starting point.

Authorize.net

Authorize.net, a Visa subsidiary, is one of the oldest US payment gateways with over 400,000 merchants and has earned Forbes' award-winning fraud protection recognition in 2025. It offers two primary models: the All-in-One plan at $25/month + 2.9% + $0.30 per card transaction (includes a merchant account), and a Gateway Only plan at $25/month + $0.10/transaction + $0.10 daily batch fee for merchants who have their own merchant account. No setup fee and no early termination fee. The platform is particularly well-suited for recurring billing and advanced fraud detection via its configurable Advanced Fraud Detection Suite.

- • Advanced Fraud Detection Suite (AFDS): 13 configurable filter rules including IP velocity, shipping/billing mismatch, and card CVV verification at no additional cost on all plans

- • Customer Information Manager (CIM): securely vault customer payment profiles for recurring billing without storing card data on merchant servers

- • Automated Recurring Billing (ARB): native subscription management supporting fixed and variable billing without custom development

- • Virtual Terminal: accept phone and mail order payments directly from a browser without hardware; included in all plans

- • Account Updater: automatically keeps stored card details current using network card-update services, reducing failed recurring charges

Authorize.net is a reliable choice for traditional US businesses — especially those in B2B, freight, or subscription services — that want a gateway with deep fraud tools and recurring billing without needing a modern API. For businesses starting fresh in 2026 without a legacy merchant account, Stripe's zero monthly fee model is likely cheaper and easier to integrate.

Verifone (2Checkout)

2Checkout, rebranded as Verifone after a 2020 acquisition, is a global monetization platform for digital and SaaS products with over 20,000 business customers. It operates as a Merchant of Record in the 2Monetize plan, handling global tax compliance, VAT, and local payment methods across 200+ territories. Three plans exist: 2Sell at 3.5% + $0.35 per transaction (physical and digital goods), 2Subscribe at 4.5% + $0.45 (subscription lifecycle tools), and 2Monetize at 6.0% + $0.60 (full MoR with tax management for digital goods only). No monthly or setup fees on any plan. An additional 2% cross-border fee applies for international transactions in most countries.

- • Merchant of Record on 2Monetize: Verifone handles VAT, sales tax, GST, and global compliance in 200+ countries, eliminating merchant tax liability

- • ConvertPlus checkout: optimized checkout supporting cards, PayPal, and 45+ local payment methods for higher global conversion

- • 2Bill: subscription management with account updater, smart retries, and involuntary churn reduction tools

- • 2Recover: revenue recovery automation that retries failed charges using AI-driven timing logic

- • Chargeback fee: $36/€31/£30 when chargeback rate is below 0.65%; rises to $50/€50/£50 above that threshold

Verifone (2Checkout) is the right choice for digital and SaaS companies that want a single vendor to handle global tax compliance without building internal tax infrastructure. The 2Monetize plan's fees are high, but the cost of managing VAT registrations across 50+ countries manually often exceeds the fee premium for growing businesses.

Worldpay

Worldpay, formerly part of FIS and currently in the process of being acquired by Global Payments, processes over 110 million transactions daily across 146 countries and 135 currencies. It is one of the largest acquiring banks globally, particularly dominant in the US and UK. Worldpay uses interchange-plus pricing but does not publicly list rates — merchants receive custom quotes based on industry and volume. From January 2026, Worldpay implemented a $35 monthly minimum fee for most accounts. UK merchants on the Simplicity plan pay 1.5% in-person and 1.3% + £0.20 online for under £75,000/year turnover, dropping to as low as 0.75% for high-volume accounts.

- • Direct acquiring in 146 countries: operates own acquiring licenses across key markets, reducing third-party dependencies and improving authorization rates

- • Worldpay iQ reporting portal: analytics and data insights covering transaction performance, trends, and reconciliation across all channels

- • Multi-currency processing: accepts 135 currencies with dynamic currency conversion at the point of sale for international customers

- • 300+ payment method integrations: cards, digital wallets, ACH, SEPA, and alternative methods via a single integration

- • Support for high-risk industries: iGaming, travel, and crypto merchants can access Worldpay where many processors decline

Worldpay suits large enterprises in the US and UK that need omnichannel acquiring under one contract and have sufficient volume to negotiate favorable interchange-plus rates. Its lack of pricing transparency and 3-year contracts make it unsuitable for businesses that want predictability without long-term commitment. Verify all fee details in writing before signing.

Checkout.com

Checkout.com is a Leader in the Forrester Wave for Merchant Payment Providers in Q1 2026 and is valued at over $11 billion. It provides direct acquiring in 50+ countries and supports 150+ processing currencies. Major clients include SHEIN, Netflix, and Klarna. Fees are not publicly listed and are negotiated per merchant; indicative rates start around 2.9% + $0.30 per transaction for smaller accounts, with volume discounts for enterprise clients. The platform provides AI-driven payment optimization, real-time analytics, and granular transaction-level reporting.

- • AI Payment Optimization: machine learning-powered acceptance rate improvement through smart routing, network tokens, and adaptive acceptance

- • Direct acquiring in 50+ countries: in-country acquiring reduces cross-border fees and typically raises authorization rates for domestic transactions

- • Flow: embedded checkout with built-in 3DS2 authentication and one-click payment for returning customers

- • Real-time reporting: granular transaction-level analytics with itemized fee breakdowns across interchange, scheme fees, and processor markup

- • Checkout.com for Platforms: embedded payment infrastructure for marketplaces with automated split payments and payouts

Checkout.com is best suited for large-scale global e-commerce and fintech businesses that have dedicated payments teams and need in-country acquiring across multiple markets. Mid-market businesses without an internal payments engineer should start with Stripe and migrate to Checkout.com when volume justifies the integration investment.

Mollie

Mollie is a Netherlands-based PSP processing tens of billions of euros annually for 200,000+ European businesses. It is founder-led, backed by Blackstone, EQT Growth, and General Atlantic, and reported €214 million in revenue in 2024 (28% growth). Mollie charges no monthly fees on its free plan — only per successful transaction. European Economic Area consumer card rates are 1.8% + €0.25; commercial cards are 2.9% + €0.25. SEPA Direct Debit and Bank Transfer are €0.25 flat. iDEAL costs €0.29 per transaction. Volume pricing with lower transaction rates and fixed monthly fees is available through paid plans. Mollie is available to EEA, UK, and Swiss registered businesses only.

- • Single integration for all major European payment methods: iDEAL (transitioning to Wero in 2026), Klarna, SEPA, Bancontact, Giropay (discontinued), cards, and 25+ others

- • Mollie Dashboard: real-time payment insights, transaction history, and settlement reporting with no additional analytics fee

- • No monthly minimum or lock-in contract — account can be opened and used without any commitment or minimum volume

- • Klarna integration: Klarna Pay Later (4.99% + €0.35), Klarna Pay Now, and Klarna Slice It available directly within Mollie checkout

- • Subscriptions and recurring billing: automated mandate-based recurring payment collection via SEPA and card

Mollie is the recommended starting gateway for European SMBs that need iDEAL, Klarna, and SEPA alongside card acceptance without monthly fees. Its simplicity and no-commitment model make it easy to start. As volumes grow and you add more currencies, evaluate whether Adyen or Stripe offers better total cost of acceptance.

Klarna

Klarna is the world's largest BNPL provider with 93 million active consumers and 500,000+ retail partners, processing $105 billion in GMV in 2024. It listed on the NYSE in September 2025 at a $15 billion valuation. Merchant fees in the US are 5.99% + $0.30 per transaction for all BNPL products (Pay in 4, Pay in 30, Financing) — significantly higher than card processing. High-volume merchants with $5M+ annual revenue can negotiate rates down to approximately 3.29% + $0.30. No monthly or setup fees. Klarna assumes 100% of fraud and default risk and pays merchants upfront in full.

- • Pay in 4: four interest-free installments over 6 weeks; increases average order value by a reported 45–68% for participating merchants

- • Pay in 30: 30-day deferred payment; popular in fashion for try-before-you-buy use cases

- • Klarna Financing: long-term loans up to 36 months at 0–29.99% APR for customers; merchant fee is lower at ~3.29% + $0.30

- • Merchant portal analytics: tracks conversion lift, order value impact, and cart abandonment data attributed to Klarna

- • Klarna app shopping: Klarna's app and browser extension expose merchant products to Klarna's 93 million active shoppers as a built-in discovery channel

Klarna is worth offering if your products are in categories (fashion, beauty, home goods, electronics) where BNPL meaningfully increases basket size and conversion. Run a 30-day A/B test before committing — if Klarna's AOV lift doesn't offset the 5.99% fee vs. your standard card rate, it is not profitable.

Afterpay

Afterpay, owned by Block (formerly Square), is a major BNPL platform integrated into Block's Cash App ecosystem. It operates in Australia, New Zealand, the US, UK, and Canada with tens of millions of active users. Merchant fees average 4%–6% + $0.30 per transaction, depending on volume, region, and merchant category. High-volume retailers can negotiate lower rates. Afterpay pays merchants in full within 1–2 business days, absorbing customer default risk entirely. The platform has driven documented sales uplifts — Factory Buys reported a 66% sales increase and Arms of Eve saw a 273% surge during Afterpay Day in March 2025.

- • Pay in 4: four equal interest-free installments over 6 weeks; customers pay 25% upfront and merchants receive the full order total immediately

- • Afterpay Day: bi-annual shopping events that drive significant traffic to participating merchants through Afterpay's app and promotional channels

- • Cash App integration: Afterpay is natively integrated with Cash App's 56 million+ active users, expanding the available buyer pool for Block-ecosystem merchants

- • Afterpay Card: virtual Mastercard allows customers to use Afterpay at any contactless in-store terminal without prior merchant integration

- • Merchant dashboard: real-time insights on Afterpay-specific sales volume, average order value, and customer demographics

Afterpay is the best BNPL choice for retailers already on Square or deeply embedded in the Block ecosystem, and for Australian merchants where Afterpay has the strongest consumer brand recognition. For businesses outside the Square ecosystem, compare Klarna and Affirm on a per-category AOV lift basis before committing.

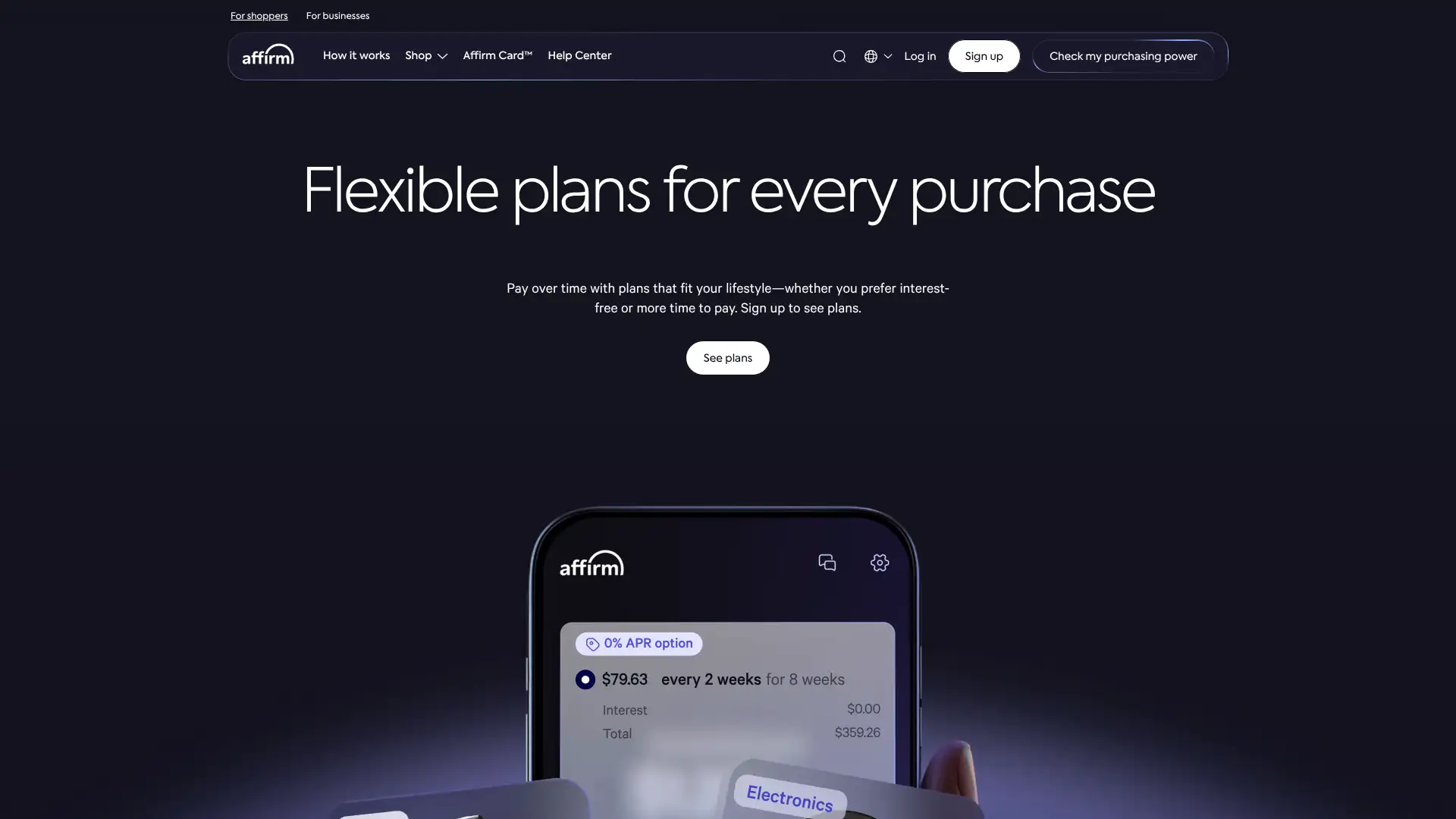

Affirm

Affirm is a US-focused BNPL provider with 36+ million active consumers and partnerships with Walmart, Amazon, Shopify, and thousands of direct merchants. It offers Pay in 4 (interest-free, 0% APR for $50–$1,000 purchases), monthly installment plans (0%–36% APR), and a dedicated Affirm Card. Merchant fees are a percentage + flat fee per transaction, with exact rates based on business type, size, and risk profile — publicly referenced at approximately 6% + $0.30 per purchase. No integration, annual, or monthly fees are charged. Affirm settles to merchants via ACH within 1–3 business days. Maximum transaction value is $17,500, the highest among major BNPL providers.

- • Split Pay (Pay in 4): interest-free four-installment plan for $50–$1,000 purchases; Affirm reports zero late fees to consumers

- • Monthly financing: installment loans from 3–60 months at 0%–36% APR, enabling customers to finance purchases up to $17,500 — the highest BNPL ticket in the industry

- • Affirm Card: Visa debit card that lets consumers initiate Affirm financing for any in-store or online purchase without merchant pre-integration

- • Shopify integration: Affirm is available as a native payment option on Shopify's Shop Pay Installments, reaching millions of Shopify merchants

- • Real-time underwriting: Affirm makes a credit decision per transaction without impacting the customer's credit score, with approval decisions in seconds

Affirm is the best BNPL provider for merchants selling products in the $200–$17,500 range where long-term financing drives purchase decisions — think fitness equipment, mattresses, dental treatments, or home improvements. For standard e-commerce categories with average orders under $200, Klarna or Afterpay typically offer comparable conversion lift.

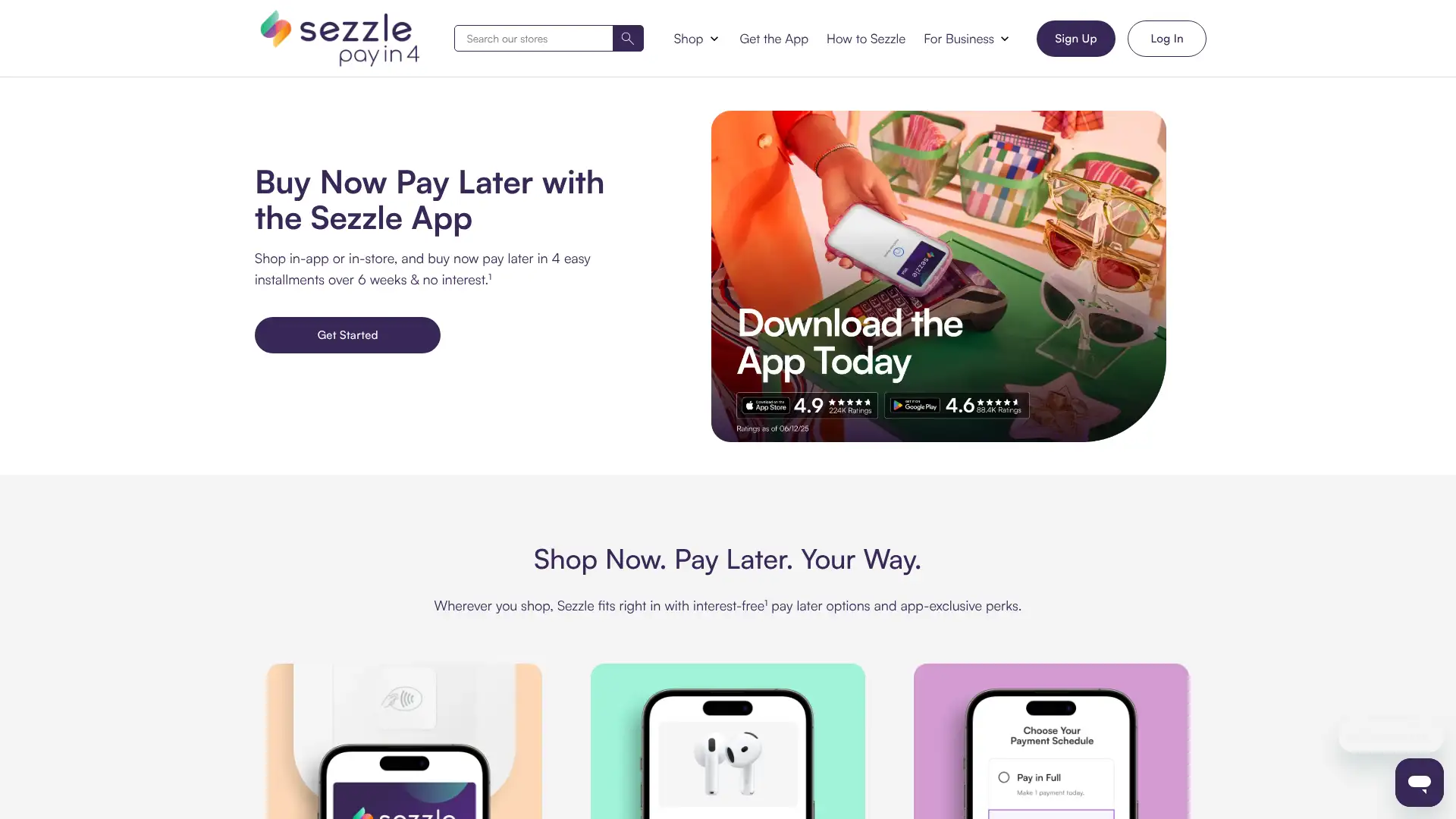

Sezzle

Sezzle is a Minneapolis-based BNPL provider and certified B Corporation, publicly traded on NASDAQ (SEZL) with an A+ Better Business Bureau rating and 4.9-star App Store rating from 148,000+ reviews. It serves 47,000+ stores in the US and Canada and uniquely reports payment history to all three credit bureaus via Sezzle Up, making it the only major BNPL provider with this credit-building feature. Merchant fees are approximately 6% + $0.30 per transaction; volume discounts are available. Merchants receive full payment at checkout; Sezzle absorbs all customer default risk. A $0 monthly minimum account management fee waiver applies when active.

- • Sezzle Up: optional credit reporting to all three bureaus (Equifax, Experian, TransUnion) for consumers, giving merchants a differentiated BNPL offering that attracts credit-conscious shoppers

- • Pay in 4: four equal interest-free payments over 6 weeks; zero interest for consumers who pay on time

- • Virtual card: customers receive a Sezzle virtual Mastercard for use at any store, expanding merchant reach beyond direct Sezzle integrations

- • Instant approval: real-time credit decisions at checkout without hard credit checks, preserving consumer credit scores

- • Sezzle Mobile app: 4.9-star rating from 148,000+ reviews indicating strong consumer retention and repeat usage

Sezzle is the right BNPL choice for US/Canada merchants whose customer base skews toward younger shoppers or those actively rebuilding credit, particularly in categories like clothing, electronics, and household goods. For merchants prioritizing pure consumer reach over credit-building differentiation, Klarna's 93 million active users will typically drive better conversion volume.

Razorpay

Razorpay is India's leading payment gateway, trusted by over 10 million businesses including Indian SMBs, D2C brands, and SaaS companies. Founded by IIT Roorkee alumni, it holds an RBI license and is PCI-DSS compliant. Domestic card, UPI, netbanking, and wallet transactions are priced at 2% + 18% GST on the platform fee. Premium methods like EMI, Amex, Diners, and corporate cards are 3% + GST. International cards cost 3% + GST with optional chargeback protection at 4% + GST total. There are no setup or annual maintenance charges. UPI has zero MDR for bank-to-bank transactions as mandated by NPCI. Razorpay settles domestic payments in T+2 days.

- • UPI-first routing: Razorpay routes to optimal UPI rail in real time, achieving ~99% success rates on UPI vs. 90%–95% on cards

- • Razorpay Payment Links: create and share payment links via email, WhatsApp, or SMS without requiring website integration

- • Razorpay Subscriptions: automated recurring billing with 0.99% additional subscription fee per transaction on top of the gateway rate

- • Smart Collect: virtual accounts for business bank transfers, enabling automated reconciliation of NEFT/RTGS/IMPS payments

- • Razorpay Capital: working capital loans for eligible merchants, disbursed within 24 hours based on transaction history

Razorpay is the default payment gateway for Indian businesses of any size due to its complete payment method coverage, zero setup costs, and UPI performance. The main tradeoff is customer support quality — businesses with complex integration needs or recurring support requirements should assess the Premium support plan or consider Cashfree for faster settlements.

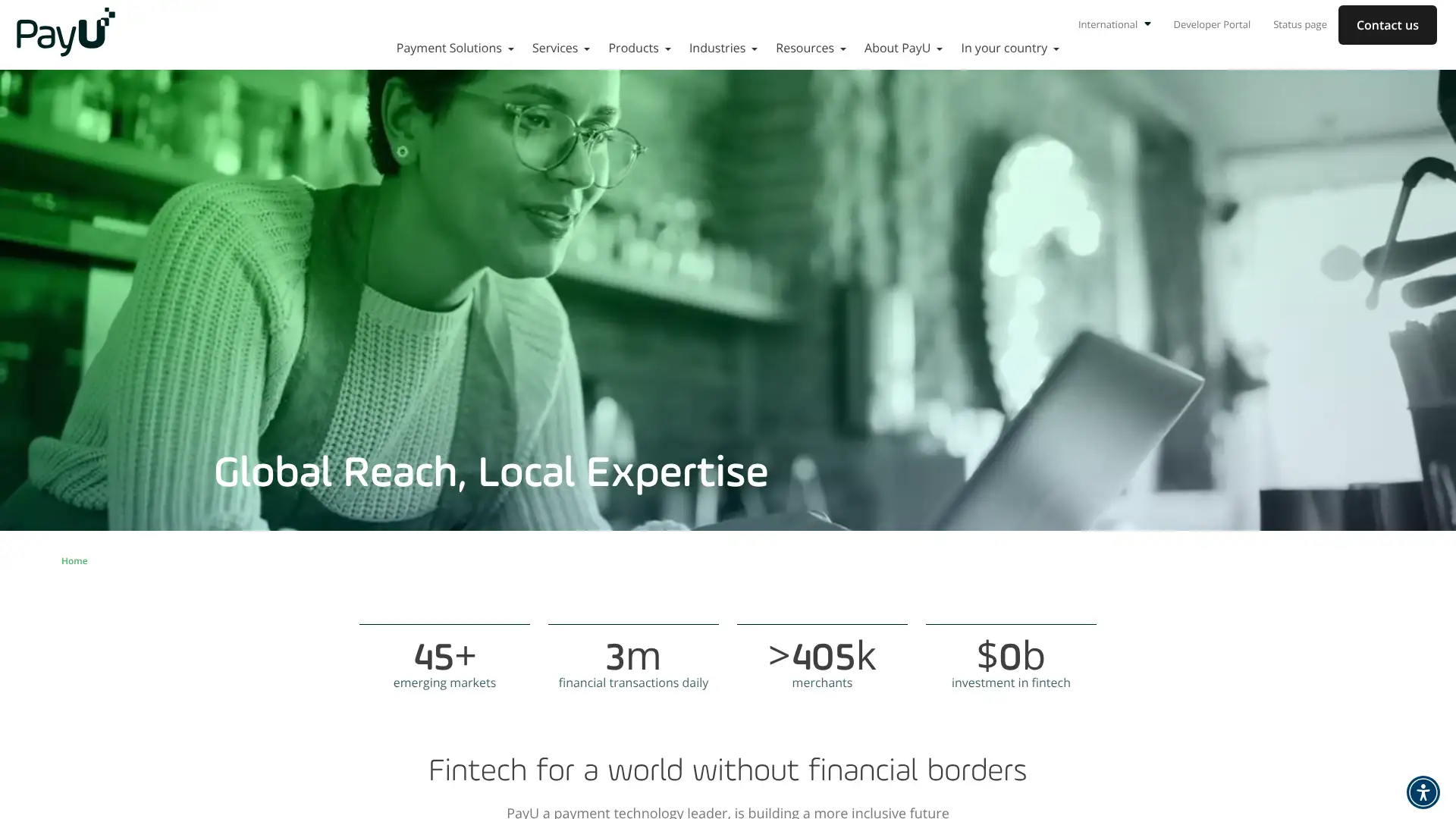

PayU

PayU is a global payment processor operating in 50+ high-growth markets, serving 300,000+ merchants in regions underserved by Western processors including India, Poland, Czech Republic, Romania, Colombia, and Egypt. In India (PayU India), the standard rate is 2% + 18% GST flat for all domestic methods, with volume discounts available after ₹10 lakh/month. Internationally, PayU uses region-specific pricing and custom quotes — no public rate card is available. PayU's platform covers cards, BNPL, wallets, and 100+ alternative payment methods suited to specific markets.

- • Multi-market single API: one integration to accept payments across India, Latin America, Central/Eastern Europe, and MEA simultaneously

- • 100+ local payment methods: covers cash-based payments (Boleto in Brazil, OXXO in Mexico), mobile money, and regional wallets per market

- • Real-time payment optimization: smart routing across acquirers to maximize authorization rates per market and card type

- • PayU LazyPay: embedded BNPL product for Indian merchants, offering customer financing without additional BNPL provider integration

- • Advanced fraud detection: risk scoring and 3DS2 support across all active markets

PayU is most valuable for businesses that need genuine multi-region payment coverage across India, LATAM, and Eastern Europe from a single provider. For India-only operations, Razorpay's better developer experience and support resources are preferable. For global enterprise operations, Adyen's direct acquiring in more markets offers stronger authorization performance.

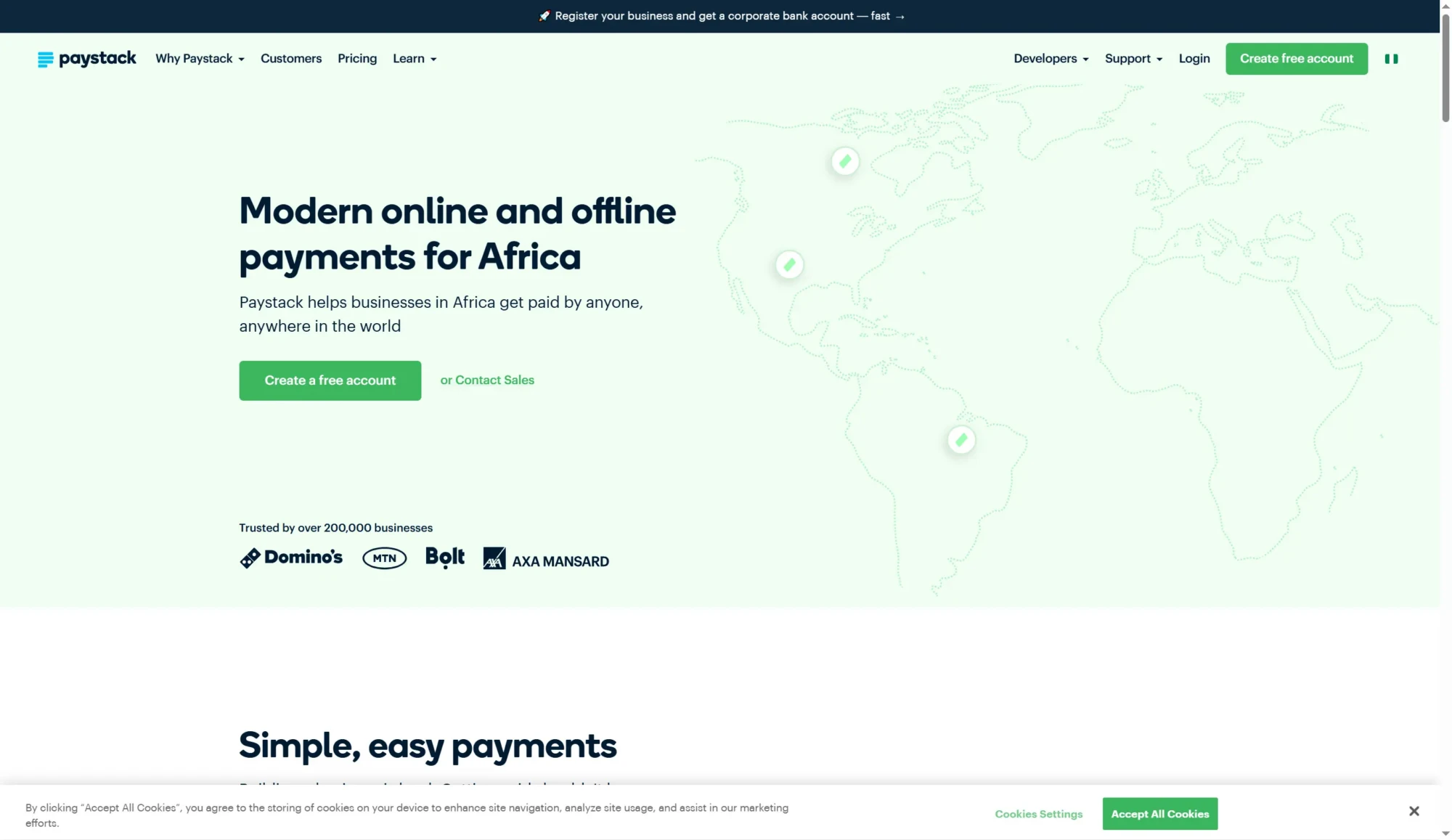

Paystack

Paystack was founded in 2015 by Shola Akinlade and Ezra Olubi and acquired by Stripe in 2020 for approximately $200 million. It operates in Nigeria, Ghana, Kenya, South Africa, Côte d'Ivoire, and other African markets. Nigerian local card transactions cost 1.5% + ₦100, capped at ₦2,000 per transaction (₦100 fee is waived for transactions under ₦2,500). International card transactions are 3.9% + ₦100. Paystack charges zero integration or maintenance fees. It processes cards, bank transfers, mobile money (M-Pesa, MTN Mobile Money), USSD, and QR codes. Paystack Terminal POS hardware is available for Nigerian merchants.

- • Paystack Checkout: hosted payment page supporting cards, bank transfer, USSD, mobile money, and QR — no custom UI required

- • Recurring billing: subscription and installment payment support with direct debit mandates for recurring revenue businesses

- • Paystack Terminal: Android-based POS hardware for Nigerian brick-and-mortar merchants, enabling card and contactless payments in-store

- • Settlement in USD option: Nigerian merchants can elect to settle in US dollars rather than naira, providing FX protection

- • Fraud detection: automated transaction monitoring and risk scoring with configurable rules to reduce chargebacks

Paystack is the best payment gateway for Nigeria-first businesses and the strongest choice in its supported African markets due to its Stripe-backed developer experience and transparent pricing. Businesses serving multiple African countries should evaluate whether adding Flutterwave alongside Paystack covers the full geographic footprint needed.

Mercado Pago

Mercado Pago is the payments and financial services arm of Mercado Libre, Latin America's largest e-commerce platform. It operates in Argentina, Brazil, Chile, Colombia, Mexico, Peru, and Uruguay, with over 120 million active users (according to PPRO data). Transaction fees are approximately 3.5% per transaction for online payments; Mercado Libre sellers settle immediately while other channels can take up to 14 days. Mercado Pago supports cards, Pix (Brazil), QR code payments, installment financing, and cash payments via convenience stores. In Brazil, Pix transactions via Mercado Pago are particularly fast and low-cost.

- • Mercado Libre integration: sellers on Mercado Libre automatically receive Mercado Pago and get instant settlement — the most efficient payment flow in LATAM e-commerce

- • Pix in Brazil: real-time bank transfer payment accepted by Mercado Pago, offering zero-fee A2A payments to Brazilian merchants

- • QR code in-store: merchants accept in-person payments via QR codes in physical stores without hardware, widely deployed by Brazilian and Argentine street vendors

- • Installment financing: consumers can split purchases into interest-bearing or interest-free installments at Mercado Pago-powered checkouts

- • Mercado Crédito: working capital loans available to merchants based on Mercado Pago transaction history

Mercado Pago is essential for any merchant that sells on Mercado Libre and cannot be replaced in that context. For direct-to-consumer LATAM e-commerce outside the Mercado Libre marketplace, evaluate whether Stripe's growing LATAM acquiring or dLocal's enterprise LATAM coverage offers better rates and developer experience.

iyzico

iyzico was founded in 2013 in Istanbul and acquired by PayU GPO, making it the leading payment gateway in Turkey. It holds a Turkish Banking Regulation and Supervision Agency (BDDK) license and is PCI-DSS Level 1 compliant. Corporate merchant fees start from 2.49% + ₺0.25 per transaction; rates displayed on iyzico's help center start from 4.29% + ₺0.25 inclusive of Banking Insurance and Transaction Tax (BITT). The Wix connector shows fees from 3.99% + ₺0.25. iyzico supports installment payments from all major Turkish banks (Bonus, World, Maximum, Cardfinans, Paraf, Axess, Advantage) with merchants receiving full upfront payout. Supports TRY, EUR, USD, GBP, NOK, RUB, and CHF.

- • Installment payments: supports up to 12-month installments for all major Turkish credit cards — merchants receive full payout upfront while customers pay monthly

- • Dynamic 3DS: AI-based activation of 3D Secure only for high-risk transactions, reducing friction for legitimate customers without compromising security

- • Iyzi POS: accept in-store card payments via iyzico's card reader, unifying online and offline payment data

- • BKM Express integration: accepts Turkey's national digital wallet for one-click checkout with Turkish bank account holders

- • 24-hour onboarding: account setup and approval completed within one business day, enabling fast time-to-market for new Turkish merchants

iyzico is the required gateway for any serious Turkish e-commerce operation — no international processor matches its installment card coverage and BDDK compliance. Run iyzico in parallel with Stripe or Adyen for international payment coverage rather than relying on iyzico alone if you sell to non-Turkish buyers.

PAYONE

PAYONE is a joint venture of Worldline and Germany's DSV Group (Sparkassen-Finanzgruppe), making it the leading payment service provider in Germany and Austria with deep integration into the German banking infrastructure. It offers online, mobile, and POS payment acceptance with full girocard support — a critical differentiator as girocard is Germany's most-used card. Online e-commerce plans start at 1.99% per transaction for a bundled shop solution with no setup fee; for existing shops, a €129 setup fee applies with 2.29% per transaction. In January 2026, PAYONE became one of the first German processors to offer Wero e-commerce acceptance, connecting merchants to 45 million Wero-capable consumers across Germany.

- • Girocard acceptance: native support for Germany's dominant card type, which is processed at significantly lower interchange than Visa/Mastercard

- • Wero e-commerce integration (2026): one of the first acquirers to offer Wero online merchant acceptance, connecting to 45+ million German Wero users

- • Germany Pays Digital: partnership with the national digitalization initiative gives eligible merchants 12 months of free card acceptance with a 24-month contract

- • TSE and GoBD-compliant POS terminals: fully compliant with German fiscal requirements for electronic receipts and transaction logging

- • SEPA direct debit and payment link support across all plans for flexible online invoice collection

PAYONE is the recommended primary acquirer for German and Austrian businesses that need girocard processing, German fiscal compliance, and early access to Wero e-commerce. Pair PAYONE with Stripe or Mollie for international payment methods beyond the DACH region.

Payoneer

Payoneer is a global payments platform operating in 190+ countries and supporting 70+ currencies, publicly traded on NASDAQ (PAYO) with approximately 2 million active users. It is primarily used for receiving international marketplace payouts (Upwork, Fiverr, Amazon, Airbnb) at 1% or free, and for sending payments between Payoneer accounts at no charge domestically or 1% internationally. In March 2025 Payoneer updated its fee structure: transfers under $400/€400/£400 carry a $4/€4/£4 flat fee; transfers above that cost 1%. Credit card payment requests carry 3.2% + $0.49. Accounts inactive for 12 months without receiving $2,000+ in payments are charged a $29.95 annual inactivity fee.

- • Multi-currency receiving accounts: US, UK, EU, CAD, AUD, JPY, SGD, and HKD local account details for receiving payments like a local business in each currency

- • Payoneer Commercial Mastercard: physical and virtual card for spending business funds globally without currency conversion at point of sale

- • Mass payouts: send up to 200 bank account payments simultaneously for contractor, supplier, and affiliate payout workflows

- • Payoneer Checkout: accept card payments in 120+ currencies for e-commerce merchants; rates vary by currency pair

- • Capital Advance: short-term working capital loans based on Payoneer transaction history, available to qualifying e-commerce sellers

Payoneer is the best tool for freelancers and remote contractors whose income comes primarily from global marketplaces like Upwork, Fiverr, or Amazon, where the zero-fee or 1% payout model substantially outperforms PayPal. For businesses that primarily receive direct client payments by credit card, Stripe or PayPal offer better checkout experiences at comparable or lower rates.

Wise (Business)

Wise (formerly TransferWise) processes over $13 billion monthly for 11.4 million active users and operates in 160+ countries. Wise Business provides multi-currency accounts with local account details in USD, GBP, EUR, CAD, AUD, SGD, JPY, HKD, and more — ideal for receiving international payments without opening foreign bank accounts. There are no monthly fees (a one-time $31 fee to unlock US local account details applies). Currency conversion fees start from 0.33%–0.41% depending on the currency pair — significantly below bank conversion spreads. Receiving via local bank transfer is free; receiving SWIFT payments may carry small fees. Wise is not a bank but holds EMI licenses in multiple jurisdictions.

- • Mid-market FX rate with transparent fee: Wise shows the exact conversion fee and mid-market rate before confirming any transfer — no hidden markup in the exchange rate

- • 40+ currency balances: hold, convert, and spend in 40+ currencies from a single account with no currency maintenance fees

- • Wise Business card: physical and virtual Mastercard debit card spending directly from multi-currency balances at the mid-market rate

- • Batch payments: send up to 1,000 payments simultaneously to suppliers, contractors, or affiliates globally in a single operation

- • Xero and QuickBooks integration: automated bank feed reconciliation for accounting without manual transaction exports

Wise Business is the benchmark for low-cost international payments and multi-currency account management. Any business making regular international transfers or holding multiple currency balances should evaluate Wise first. Its limitations — no credit, no cash deposit — mean it works best as a complement to a traditional business bank account rather than a replacement.

Skrill

Skrill is a digital wallet and payment platform operated by Paysafe Group, available in 100+ countries and regulated by the FCA in the UK. It is widely accepted in online gaming, sports betting, forex, and digital entertainment verticals where PayPal's usage policies are restrictive. For merchants receiving payments, fees are approximately 2.9% + €0.29 per transaction (varies by business category and volume). Sending money between Skrill users costs 1.45% capped at €10. Currency conversion carries up to a 4.99% FX markup over the interbank rate. Skrill charges a $5/month inactivity fee after 12 months without a login or transaction.

- • Digital wallet: customers pay with Skrill balance without sharing bank or card details with merchants, popular in privacy-conscious verticals

- • Rapid Transfer: instant bank-funded Skrill account top-up at 1% fee, enabling fast fund loading for time-sensitive transactions

- • Skrill Visa Prepaid Card: physical card allowing Skrill balance spending globally at any Visa-accepting merchant or ATM

- • VIP tiers: Silver, Gold, and Diamond VIP levels with reduced conversion fees (as low as 1.30% for Diamond crypto trades) based on annual transaction volume

- • Crypto buy/sell: buy and sell 10 cryptocurrencies within the Skrill account in 40 fiat currencies

Skrill is a niche solution best suited for merchants in iGaming, sports betting, and forex trading who need a digital wallet that consumers in those verticals actively use. For mainstream e-commerce, PayPal or Stripe offer better consumer reach and more competitive merchant fees. The 4.99% FX markup is a dealbreaker for any business with significant cross-currency payment volume.

GoCardless

GoCardless is a bank payment specialist founded in 2011, processing over $130 billion annually for 100,000+ businesses including DocuSign, The Guardian, and NHS. It specializes in direct debit and bank-to-bank payments, not card processing. Three plans are available in the US: Standard at 0.5% + $0.05/transaction (domestic, capped at $5), Advanced at 0.70% + $0.05, and Pro at 0.90% + $0.05. International payments range from 1.5% + $0.05 to 1.90% + $0.05 depending on plan. No monthly fees on Standard or Advanced; Pro includes additional white-labeling features. GoCardless is targeting full-year profitability by 2026 and reported revenue of £126.8 million for the year ending June 2024.

- • Direct debit across 30+ countries: UK Bacs, SEPA, ACH, BECS (Australia/NZ), Autogiro (Sweden), and more via single API integration

- • Success+ (failed payment retry): AI-powered intelligent payment retry for Advanced and Pro plans, reducing involuntary churn for subscription businesses

- • Instant Bank Pay: real-time one-off payment collection in UK and Germany using open banking, completing in under 10 seconds

- • 350+ integrations: pre-built connectors for Xero, QuickBooks, Zuora, Recurly, Chargebee, TeamUp, and other subscription platforms

- • No chargeback fees for most merchants (applies above 15 chargebacks/month, affecting only 0.25% of active merchants)

GoCardless is the best tool for subscription businesses that can offer bank debit as a payment option, as the cost savings vs. card processing are substantial — especially for B2B SaaS where average contract values are high. It must be run alongside a card processor for customers who prefer card payments.

Trustly

Trustly is a Swedish open banking payments company founded in 2008, processing $85–$100 billion in payments in 2024 — a 54% year-over-year increase. It connects to 12,000 banks across 30+ markets in Europe, North America, and beyond, and is owned by Nordic Capital at an estimated $10 billion valuation. Trustly charges approximately 1.5% per transaction with a €0.80 minimum fee; exact pricing is not publicly listed and is negotiated per merchant. No setup or monthly fees for direct integrations, but direct Trustly access typically requires merchants with minimum annual revenue of €5 million. Smaller businesses access Trustly via third-party PSPs. The platform processes 95%+ of European transactions in under 5 minutes.

- • Pay N Play (iGaming): instant deposit combined with real-time KYC using bank-verified identity data — eliminates registration form for iGaming merchants

- • Instant settlement: 95%+ of European transactions complete in under 5 minutes with funds transferred in real time, improving cash flow vs. card settlement cycles

- • Zero chargebacks: bank-authenticated push payments are essentially irreversible, eliminating chargeback risk entirely for merchants

- • Data products: Trustly's open banking data products enable income verification, credit scoring, and affordability checks beyond pure payment initiation

- • FedNow and RTP integration (US): connects to US real-time payment rails, enabling instant Pay by Bank payments for US merchants

Trustly is the leading open banking payment method for iGaming, travel, and high-ticket European e-commerce where bank transfer conversion is strong and eliminating chargebacks justifies the integration investment. Merchants processing under €5M annually should access it via an existing PSP rather than pursuing direct integration.

iDEAL

iDEAL is the Netherlands' dominant online payment method, used for 72%+ of Dutch e-commerce transactions and processing 1.5+ billion transactions annually across 350,000 participating merchants. Since 2023 it has been owned by the European Payments Initiative (EPI). As of January 2026, iDEAL is undergoing a phased migration to Wero, the new pan-European payment standard. The co-branded 'iDEAL | Wero' logo began appearing at Dutch checkouts from January 31, 2026; payments through the Wero infrastructure began March 31, 2026. Full migration to Wero is expected by end of 2027. For merchants, there is no disruption during the migration — existing iDEAL integrations via PSPs continue to function. Consumer-facing the payment experience is unchanged. Merchant fees are set by PSPs and typically €0.25–€0.40 per transaction.

- • 72%+ Dutch e-commerce market share: accepted by virtually all Dutch consumers through their banking app with no friction or additional registration

- • Instant payment confirmation: transaction results are returned in real time, enabling immediate order fulfillment confirmation

- • Zero chargeback risk: bank-authenticated push payments cannot be reversed by customers after approval

- • iDEAL | Wero transition: from March 31, 2026, iDEAL payments begin routing through Wero infrastructure while maintaining identical user experience through end of 2027

- • 350,000+ Dutch merchant acceptance points: the most widely integrated local payment method in the Netherlands

iDEAL is essential for any merchant selling to Dutch consumers — it is the expected, default payment option and its omission will cost conversions. Accept it via your existing PSP (Mollie, Stripe, or Adyen all support it) rather than any direct integration. Merchants should monitor the Wero migration timeline and follow their PSP's guidance on logo updates by January 31, 2026.

Bancontact

Bancontact is Belgium's most-used payment method, with over 17 million cards in circulation and acceptance at virtually all Belgian payment terminals and online stores. It is operated by Bancontact Payconiq Company and is beginning integration with Wero as part of the European Payments Initiative (EPI), with a joint Bancontact/Wero platform launched in Belgium in 2026. For merchants, Bancontact is accessed via PSPs (Mollie, Stripe, Adyen, etc.) at typically €0.10–€0.30 per transaction depending on the PSP. Transactions are bank-authenticated push payments with immediate confirmation and no chargeback risk.

- • 17+ million Bancontact cards in circulation covering virtually the entire Belgian adult population

- • QR-based mobile payment: Bancontact Payconiq app enables QR code payments in-store and online, used for P2P and merchant payments

- • Wero co-platform: from 2026 Bancontact begins joint branding with Wero for Belgian merchants, preparing for a phased European payment standard

- • Zero chargebacks: bank-authenticated transactions are irreversible, eliminating dispute risk for merchants

- • Instant confirmation: payment status returned in real time, enabling immediate inventory release and order confirmation

Bancontact is non-negotiable for Belgian merchant checkouts. Accept it via your PSP at minimal additional cost and update to the Bancontact/Wero co-branding as instructed by your PSP during the 2026 transition. There is no reason to delay accepting Bancontact for any store serving Belgian consumers.

Apple Pay

Apple Pay is a digital wallet and contactless payment service that uses tokenized card credentials stored in the Secure Element of Apple devices. It is accepted at 85%+ of US retail locations and by tens of millions of online merchants globally. Apple Pay does not charge merchants any additional fees beyond standard card processing rates — merchants pay only their card processor's rates (e.g., Stripe's 2.9% + $0.30). For merchants, Apple Pay is enabled through existing payment processors like Stripe, Adyen, Braintree, and Square with minimal integration overhead. iOS devices hold over 1 billion active users globally. Apple Pay is not available on Android devices.

- • Tokenized payment: Apple Pay replaces card numbers with device-specific tokens, eliminating the possibility of card data theft at the merchant level

- • Face ID / Touch ID authentication: biometric verification makes Apple Pay checkout faster and more secure than entering card details manually

- • Express Checkout: one-tap payment directly from product pages or carts without requiring customers to complete a full checkout form

- • Apple Pay for Safari: works in mobile and desktop Safari for in-app and web purchases across iOS, iPadOS, and macOS

- • Apple Pay Business Register: merchant information registered with Apple ensures payment sheet displays business name rather than a technical identifier

Apple Pay should be enabled on every e-commerce website and mobile app immediately — it costs nothing additional, improves checkout conversion among Apple users, and adds biometric security. Enable it through your existing processor (Stripe, Adyen, etc.) rather than treating it as a separate integration project.

Google Pay

Google Pay (GPay) is Google's digital wallet and payment platform available on Android devices, Chrome browser, and in apps. It tokenizes stored card credentials from users' Google accounts and enables one-tap payment at checkout. Google Pay does not charge merchants any additional fees — merchants pay only their payment processor's standard rates. Google Pay has over 150 million users in 40+ countries and is supported by virtually all major payment processors including Stripe, Adyen, Braintree, Square, and Checkout.com. In the US, Google Pay also supports bank account funding for online purchases, providing an alternative to card-based payments.

- • Works on Android, Chrome, and web: Google Pay is available across the Android ecosystem (72% of global smartphones) and in Chrome browser on any device

- • Tokenized credentials: replaces actual card numbers with encrypted tokens, protecting merchant and customer from card data exposure

- • Google Pay API: simple JavaScript integration enables Google Pay button display on any web checkout or Android app

- • Bank account payment in the US: Google Pay supports ACH-based payments direct from bank accounts in addition to card-backed payments

- • Google Maps and Search integration: Google Pay enables purchases directly from Google search results, maps directions, and assistant interactions

Google Pay should be enabled alongside Apple Pay as a zero-cost checkout conversion tool. The combination covers iOS users (Apple Pay) and Android/Chrome users (Google Pay) and represents the most impactful two-step checkout optimization any e-commerce merchant can make without changing processors.

Amazon Pay

Amazon Pay allows customers to use their Amazon account's stored payment methods and shipping addresses on third-party websites. It is accepted by 6,000+ external merchants and leverages Amazon's 300 million active customer accounts globally. Amazon Pay charges merchants 2.9% + $0.30 per domestic transaction in the US (the same rate as Stripe), plus a $0.30 authorization decline fee per declined transaction. No monthly fee or setup fee. International transactions carry an additional 1.5% cross-border fee and 1.5% currency conversion fee. Amazon Pay also offers Login with Amazon as a combined one-click authentication and payment solution.

- • 300 million Amazon account profiles: enables one-click checkout with stored payment and address details for the world's largest stored-card base

- • Login with Amazon: combined authentication and payment initiation that reduces checkout friction and account creation barriers for new buyers

- • Alexa voice commerce: Amazon Pay powers purchases initiated through Amazon Echo devices and Alexa integrations

- • A-to-z Guarantee: Amazon Pay extends its buyer protection to third-party merchant transactions, increasing consumer trust

- • Multi-currency support: processes payments in 12 currencies with Amazon handling currency conversion for international customers

Amazon Pay is worth testing for merchants whose analytics show significant traffic from Amazon Prime members or whose products are closely related to categories Amazon sells. The conversion lift from pre-filled Amazon credentials can offset the standard 2.9% + $0.30 rate. International merchants should be cautious given the 3% cumulative cross-border/FX surcharge.

Shopify Payments

Shopify Payments is Shopify's native payment processing solution, included in all Shopify plans with no additional monthly fee. Using Shopify Payments eliminates Shopify's 0.6%–2% third-party transaction fee that applies when using external processors like Stripe or PayPal. Online processing rates range from 2.9% + $0.30 (Basic, $39/month annual) to 2.5% + $0.30 (Grow, $105/month) to 2.4% + $0.30 (Advanced, $399/month). In-person rates are 2.6% + $0.10 on Basic. Currency conversion carries a 1.5% fee for US-based stores. Over 4.8 million Shopify stores use Shopify Payments across 17 supported countries. Shopify Payments is powered by Stripe's infrastructure.

- • Integrated checkout: payment data, order management, and analytics are unified in Shopify Admin — no reconciliation between a separate processor dashboard and Shopify

- • Shop Pay: Shopify's accelerated checkout, allowing shoppers who have used Shop Pay anywhere to check out with stored details in one tap — documented 50%+ higher conversion than guest checkout

- • Multi-currency: automatically display prices and process transactions in 130+ local currencies without separate FX configuration

- • Fraud analysis: built-in fraud scoring powered by Stripe's Radar included at no additional cost on all Shopify plans

- • Shopify Balance: business bank account and Mastercard debit card with 2.29% cashback rewards (3.32% for Plus) on eligible purchases

Any Shopify merchant should use Shopify Payments as their primary processor to eliminate the 2% Shopify transaction fee — it is almost always the most cost-effective option and unifies order/payment management. Add PayPal as a secondary checkout option for shoppers who prefer not to enter card details, but keep Shopify Payments as the default.

SOFORT

SOFORT was a German bank transfer payment method operating across Austria, Belgium, Germany, Netherlands, and Spain. Acquired by Klarna in 2014, it was progressively merged into Klarna's own product suite. As of March 31, 2025, SOFORT has been fully discontinued as a standalone payment method. Stripe removed SOFORT support on that date. All SOFORT integrations are non-functional. The recommended replacement is Klarna's 'Pay Now' option, which replicates the instant bank transfer flow within Klarna's platform. Merchants who still reference SOFORT in checkout pages or documentation should remove all SOFORT branding and replace with Klarna Pay Now or an alternative pay-by-bank method.

- • DISCONTINUED: SOFORT ceased operations March 31, 2025 and is no longer available as a payment method on any platform

- • Replacement: Klarna Pay Now (formerly Klarna Pay Now) replicates the instant bank transfer checkout experience in Germany, Austria, and Belgium

- • Alternative: Wero is rolling out across Germany, France, Belgium, and Netherlands (2026) as the European A2A payment standard backed by major banks

- • Alternative: GoCardless instant bank pay offers UK and Germany open banking payment initiation for one-off transactions

- • Stripe note: Stripe automatically hides SOFORT from payment UIs; merchants using custom API integrations must explicitly remove SOFORT from payment method lists

SOFORT no longer exists as a standalone payment method. Remove all SOFORT references from checkout pages, documentation, and marketing materials immediately. Replace with Klarna Pay Now for the closest functional equivalent in the DACH market, or integrate Wero through your PSP as it becomes available in your target markets during 2026.

Giropay

Giropay was a German online payment method enabling direct bank transfers from 1,500+ German bank accounts, launched in 2006 and used by approximately 45 million customers (54% of Germany's population) at its peak. It merged with Paydirekt in 2021 and was owned by a consortium of German banks including Deutsche Bank, Postbank, Commerzbank, and the Sparkassen-Finanzgruppe. On July 1, 2024, Paydirekt announced Giropay would be permanently shut down. All Giropay payments ceased on December 31, 2024. Refund functionality remained available until January 31, 2025. German banks are backing Wero (EPI) as Giropay's successor, launched in Germany in 2024 with merchant e-commerce acceptance rolling out in 2025–2026.

- • DISCONTINUED: Giropay ceased all payment operations on December 31, 2024; any remaining Giropay integrations will return errors

- • Wero successor: German banks (Deutsche Bank, Sparkassen, Volksbanken) are backing Wero as Giropay's intended European successor for bank-to-bank payments

- • Wero Germany status: Wero e-commerce acceptance launched in Germany from November 2025 via PAYONE and select PSPs; rolling out to more PSPs through 2026

- • Alternative: PayPal has 31 million German accounts and is the most-used digital payment method in Germany by market share (27.7%)

- • Alternative: SEPA instant credit transfer via open banking (Trustly, GoCardless) provides account-to-account payments in Germany without Giropay infrastructure

Giropay no longer exists. Remove all Giropay buttons, logos, and references from German checkout pages and documentation. For German bank transfer capability, integrate Wero through your PSP when it becomes available on your platform, and ensure PayPal and Klarna are offered in the interim to retain German consumer checkout options.