36 Best Insurance Companies and Comparison Platforms in 2026

This directory covers the leading insurance carriers and digital comparison platforms in the United States, spanning auto, home, life, renters, and specialty coverage. We include both direct insurers (where you buy a policy) and marketplaces (where you compare quotes across multiple carriers). Pricing figures are verified as of March 2026 based on published rate data and insurer pricing pages.

GEICO

GEICO is the third-largest U.S. auto insurer by market share, owned by Berkshire Hathaway, and one of the few national carriers writing policies in all 50 states. Its average full-coverage premium runs approximately $1,867 per year — about 21% below the national average of $2,290. Beyond auto, GEICO distributes home, renters, life, pet, and specialty coverages, though most non-auto products are underwritten by third-party carriers. The company's DriveEasy telematics program rewards safe drivers with premium discounts, and its 2024 data shows an average new-policyholder savings of hundreds annually. GEICO's mobile app and 24/7 digital claims process earn it high convenience scores, and it carries an A++ (Superior) AM Best rating for financial strength.

- • DriveEasy telematics: opt-in safe driving program that tracks braking and phone use to lower premiums through the GEICO mobile app.

- • Multi-policy discounts: bundling auto with home, renters, motorcycle, or life insurance reduces premiums; GEICO reports an average 18% bundle discount for home and auto.

- • 16+ discount categories: good student (B+ GPA or above), government employees, military members, five-year accident-free, and more.

- • Claim Forgiveness: available as a purchased or earned feature; prevents rate increases after a first at-fault claim in most states.

- • Coverage breadth: auto, motorcycle, RV, boat, home, renters, condo, life, pet, travel, event, and umbrella policies available through GEICO's distribution network.

GEICO is the go-to for drivers who want low rates, a strong app, and the confidence of Berkshire Hathaway's backing — without needing to interact with an agent. It is weakest if you want true one-stop bundling under a single underwriter; home and life products are passed to third parties.

State Farm

State Farm is the largest U.S. personal lines insurer, writing roughly 24% of the private-passenger auto market with $66.5 billion in direct written premium in 2024. It operates through more than 19,000 licensed agents and holds over 94 million active policies. Average full-coverage auto premium runs $2,169 per year per a 2025 NerdWallet rate study — about 5% below the national average for clean-record drivers. In November 2025, AM Best downgraded the mutual parent from A++ to A+ (Superior) following five consecutive years of underwriting losses, though the rating still reflects strong claims-paying capacity. State Farm paused new homeowners policies in California, Massachusetts, and Rhode Island, and applied a California state-approved 17% homeowners rate hike in June 2025 following $7.6 billion in January 2025 wildfire losses.

- • Drive Safe & Save telematics: usage-based program offering up to 30% discount based on mileage and driving habits tracked via mobile app.

- • Steer Clear program: discount program for drivers under 25 that combines a driving course with monitored on-road performance.

- • Full product suite: auto, home, renters, life, health, disability, and small business insurance all available through a single agent.

- • 19,000+ local agents: nationwide agent network that J.D. Power consistently rates above average for customer satisfaction and responsiveness.

- • Claim cycle times: routine auto losses average 7–14 days; catastrophe-response teams are deployed after major weather events.

State Farm is the strongest choice for households that want a single agent managing auto, home, and life insurance with face-to-face service and a long track record. For pure price sensitivity, GEICO or Nationwide usually beat it; for California homeowners, State Farm is currently not an option for new policies.

Progressive

Progressive is the second-largest U.S. auto insurer by market share and has spent decades pioneering usage-based insurance. Its Snapshot telematics program — available as a plug-in OBD-II device or smartphone app — has paid out over $1.2 billion in discounts; safe drivers who complete the program save an average of $322 per year at renewal, with an initial sign-up discount averaging $169. Average annual full-coverage premium sits around $2,060, slightly above GEICO but below Allstate. Progressive received the number-one ranking for overall online customer experience in Keynova Group's Q4 2025 Online Insurance Scorecard, with its AI-powered photo claims system noted as more mature than most competitors. The company also offers home, renters, life, boat, and commercial auto through its network.

- • Snapshot telematics: tracks braking (hard braking defined as a speed decrease of 7 mph/sec or more), night driving, mileage, and phone use to deliver a personalized rate at renewal.

- • Accident Forgiveness: Small Accident Forgiveness applies from day one for claims under $500; Large Accident Forgiveness protects your rate after five years claim- and violation-free.

- • Name Your Price tool: allows drivers to set a budget and see what coverage Progressive can offer at that price point.

- • AI photo claims: Progressive's AI estimate system handles a wider range of claim types without adjuster involvement than most peers, enabling faster settlements.

- • Rate comparison tool: Progressive was the first major insurer to display competitor rates alongside its own quotes, a long-standing differentiator.

Progressive is the best choice for safe, low-mileage drivers who are comfortable with telematics and value a best-in-class digital experience. If you're a city driver with lots of stop-and-go traffic, Snapshot might hurt your rate — compare quotes from GEICO before committing.

Allstate

Allstate is one of the largest publicly traded insurers in the U.S., offering auto, home, life, renters, motorcycle, and business insurance through a network of over 10,000 exclusive agents. Its average full-coverage auto premium runs approximately $2,509 per year, which is above both GEICO and State Farm, according to Insurance.com's 2025 data. Allstate's Drivewise telematics program rewards safe driving with up to 40% in potential discounts. The company offers extensive homeowners coverage options including unique add-ons like identity theft protection and green improvements coverage. Allstate has an A+ (Superior) financial strength rating from AM Best and is licensed in all 50 states.

- • Drivewise telematics: tracks acceleration, braking, and time of day to offer up to 40% in discounts; safer than Snapshot for urban drivers as there is no penalty for hard braking.

- • Claim Satisfaction Guarantee: if you're dissatisfied with your claim experience, Allstate will credit six months of your premium to your account — unique among major carriers.

- • Homeowners add-ons: identity theft restoration, green improvement coverage (pays to upgrade to greener materials after a loss), and business property rider.

- • Digital Locker app: free app that lets policyholders catalog personal property for faster, more accurate claims.

- • 10,000+ exclusive agents: large agent network for those who want face-to-face policy management and claims support.

Allstate makes sense for homeowners who want broad coverage options and an agent relationship, and who can use Drivewise to manage the higher baseline auto premium. Pure price shoppers will consistently find better rates elsewhere.

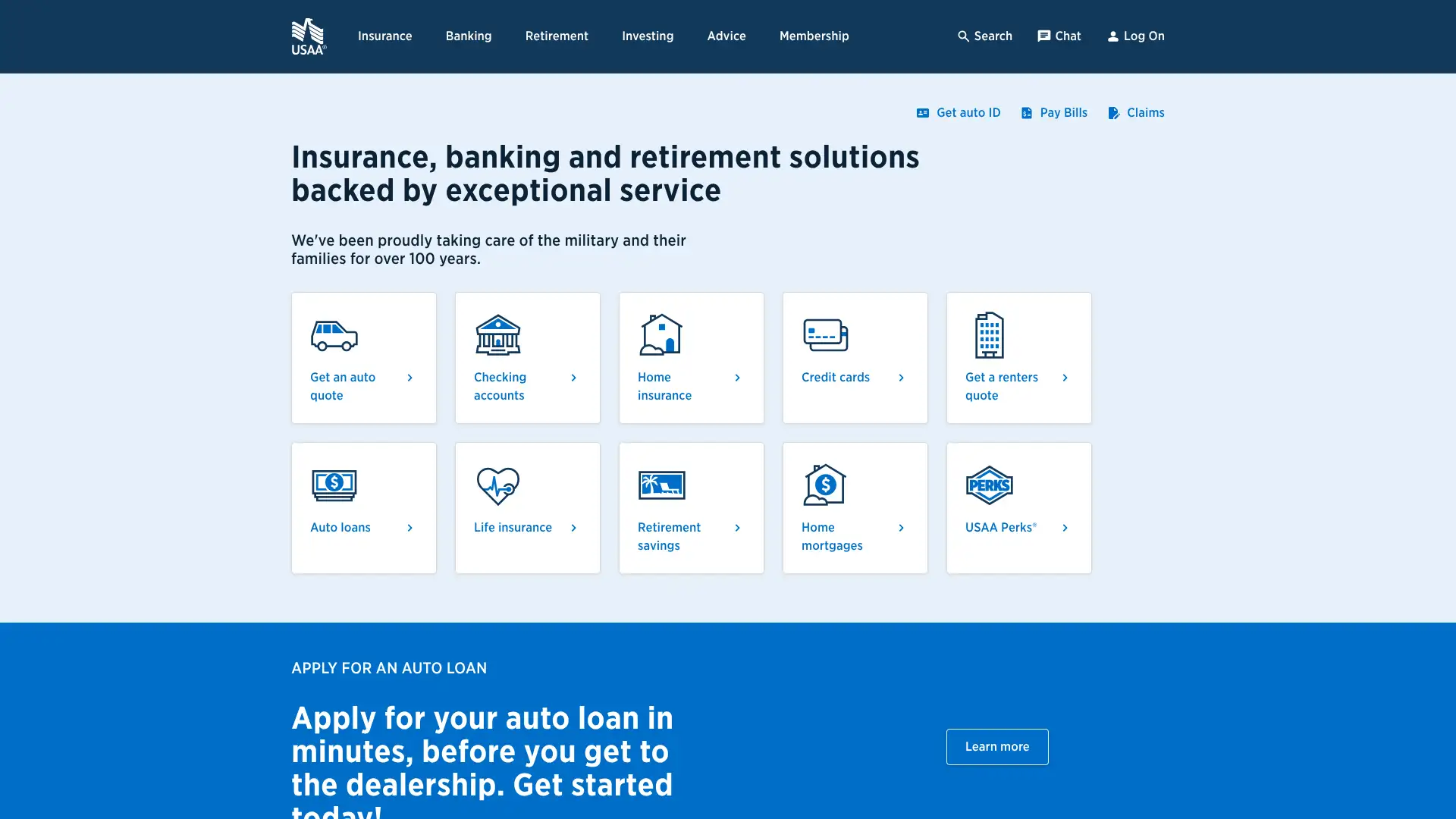

USAA

USAA is widely regarded as the gold standard for insurance quality in the United States, but is restricted to current and former U.S. military members and their immediate families. It consistently ranks first or near-first in J.D. Power customer satisfaction studies for auto, home, and banking, and its auto insurance rates are among the cheapest of any national carrier. Average full-coverage auto premiums run approximately $1,600 per year or less for clean-record drivers — below GEICO and well below Allstate. USAA carries an A++ (Superior) AM Best financial strength rating and has no shareholders, meaning profits are returned to members. It offers auto, home, renters, life, health, flood, and valuables insurance, plus banking and investment products.

- • SafePilot telematics: usage-based program offering up to 30% discount for safe driving; simpler and less penalizing than most competitor programs.

- • Military-specific features: coverage for deployed vehicles, storage discounts, and comprehensive-only policies for vehicles stored overseas.

- • No-deductible glass coverage: USAA auto policies include windshield repair or replacement with no deductible in most states.

- • A++ AM Best rating: highest financial strength rating available, reflecting a capital-rich mutual structure with no shareholder dividends to pay.

- • Full-service financial institution: banking, credit cards, investment accounts, mortgages, and insurance all under one roof for members.

USAA is the undisputed best insurance option for those who qualify — best rates, best service, and best financial strength. If you are not eligible, the closest equivalents for overall value are GEICO for price and State Farm for service.

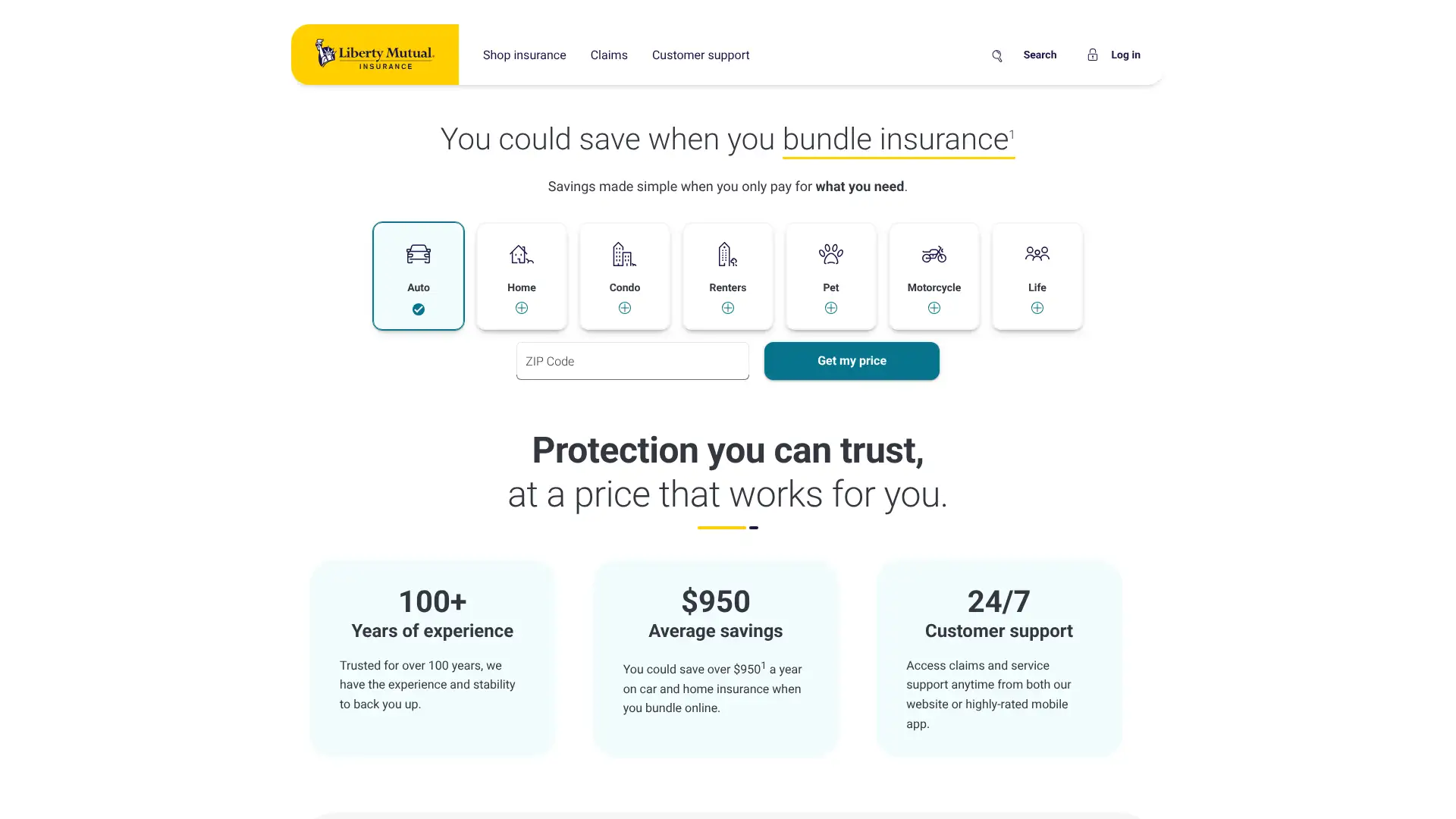

Liberty Mutual

Liberty Mutual is the sixth-largest U.S. property and casualty insurer, offering auto, home, renters, life, and commercial coverage nationwide. Its auto premiums run higher than most major competitors — average full-coverage rates sit around $225/mo nationally — but the company offers extensive customization through optional add-ons such as new car replacement, better car replacement, and lifetime repair guarantee. Liberty Mutual's RightTrack telematics program can save safe drivers up to 30% at renewal. The company holds an A (Excellent) AM Best rating and offers policies in all 50 states. It operates both through agents and directly online.

- • New Car Replacement: if your car is totaled in the first year or first 15,000 miles, Liberty Mutual pays for a brand-new replacement rather than the depreciated value.

- • Better Car Replacement: extends new car replacement beyond the first year, replacing your totaled car with a model one year newer with up to 15,000 fewer miles.

- • RightTrack telematics: tracks driving behavior for 90 days with up to 30% potential discount at first renewal; no penalty for monitored driving habits.

- • Lifetime Repair Guarantee: repairs made by a Liberty Mutual-approved shop are guaranteed for as long as you own the vehicle.

- • Blanket and scheduled personal property: flexible options for jewelry, electronics, and art with no deductible on scheduled items.

Liberty Mutual is worth considering if new car replacement or better car replacement matters to you and you can use RightTrack to offset the premium. For most drivers, the high baseline rates make it hard to justify over GEICO or Progressive on price alone.

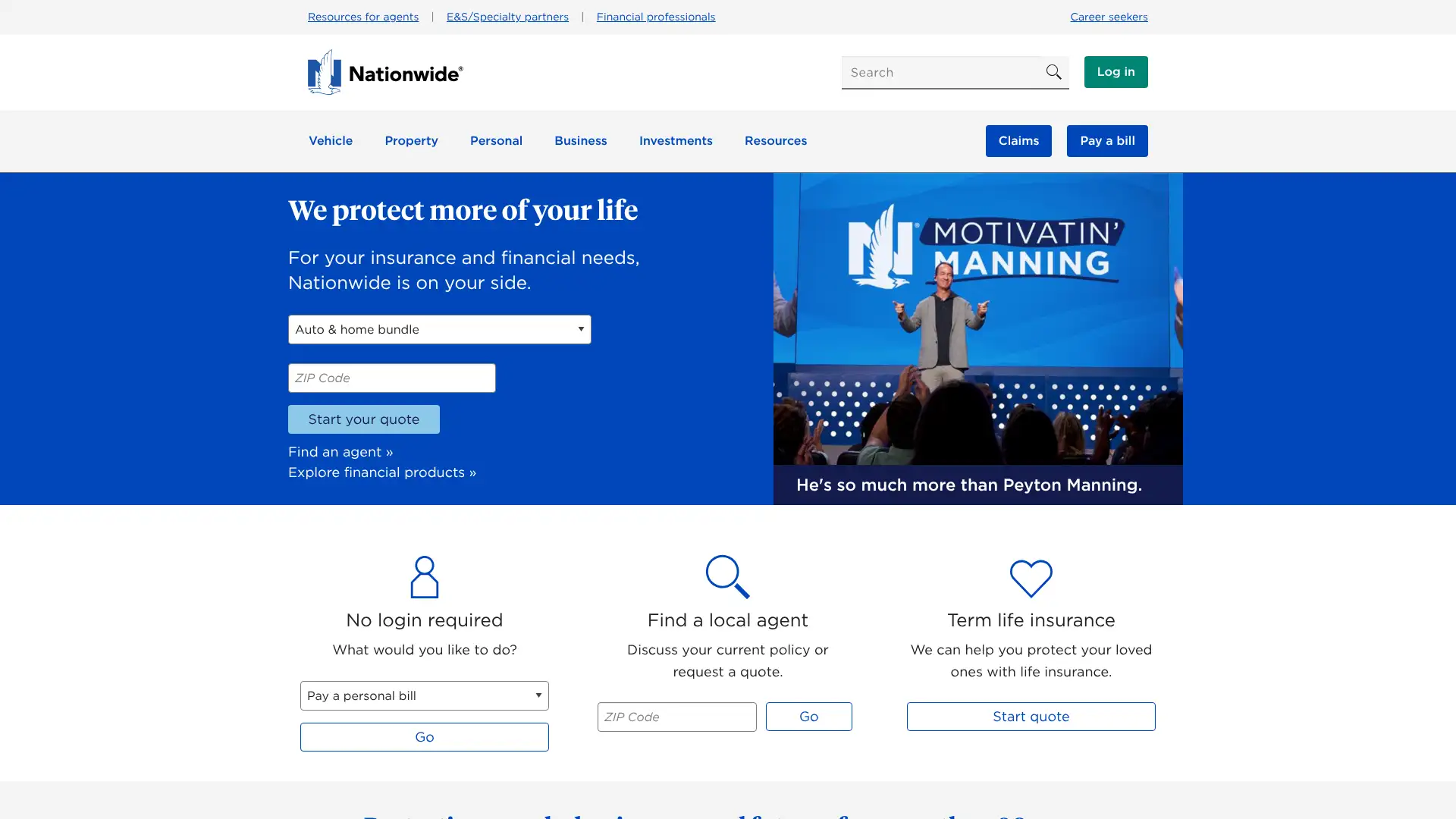

Nationwide

Nationwide is a Fortune 100 mutual insurer headquartered in Columbus, Ohio, offering auto, home, renters, life, farm, and commercial insurance across the country. Its average full-coverage auto rate comes in around $1,548 per year per Insurance.com's 2025 data — below both State Farm and Allstate and competitive with GEICO. Nationwide's SmartRide and SmartMiles telematics programs reward safe and low-mileage drivers respectively. The company has an A+ (Superior) AM Best rating and is particularly strong in farm and agricultural insurance through its Nationwide Agribusiness subsidiary. Nationwide does not sell auto insurance in Alaska, Hawaii, Louisiana, and Massachusetts.

- • SmartRide telematics: monitors driving behavior and can save qualifying drivers up to 40% on auto premiums at renewal.

- • SmartMiles: pay-per-mile auto insurance program that charges a fixed monthly base rate plus a low per-mile charge — ideal for remote workers or low-mileage drivers.

- • On Your Side Review: free annual policy review with a Nationwide agent to check for coverage gaps and unearned premiums.

- • Vanishing deductible: earn $100 off your deductible for each claim-free year, up to a $500 reduction.

- • Gap coverage: loan/lease payoff coverage pays the difference between your car's value and what you owe to the lender if it's totaled.

Nationwide is a solid mid-tier choice for drivers who want below-average rates, vanishing deductible benefits, and a pay-per-mile option — particularly for low-mileage drivers in the 39 states it covers. Erie Insurance often beats it on claims satisfaction in overlapping states.

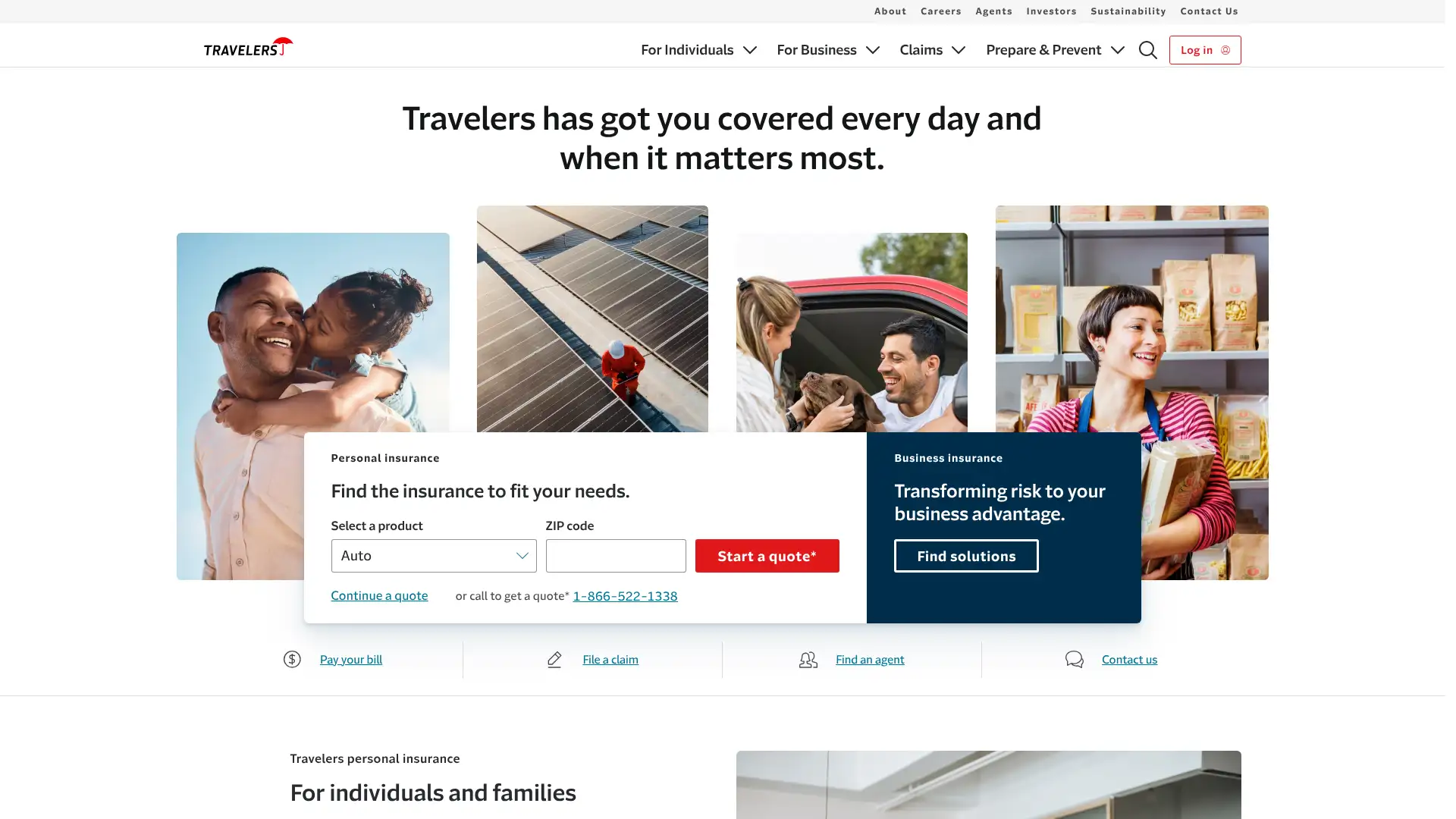

Travelers

Travelers is one of the oldest and largest U.S. property-casualty insurers, writing approximately $40 billion in annual premiums. It carries an A++ (Superior) AM Best rating — one of the strongest in the industry. NerdWallet's 2025 homeowners insurance analysis found Travelers to be among the cheapest large insurers for home coverage, with an average annual premium of around $2,055. On auto, Travelers rates average $1,980/yr for full coverage, competitive with Nationwide. Travelers does not write auto insurance in Alaska, Hawaii, or North Carolina, but maintains a broad national footprint elsewhere, selling through both independent agents and directly online.

- • IntelliDrive telematics: 90-day monitoring program for auto; safe drivers typically earn 10–20% savings at renewal with no upfront penalty.

- • Green Home coverage: pays additional cost to rebuild with green-certified materials after a covered loss — available on homeowners policies.

- • Valuable Items endorsement: scheduled coverage for jewelry, fine art, collectibles, and musical instruments with agreed value payout and worldwide protection.

- • Premier Renovation Coverage: covers homes under renovation for loss to materials and equipment that a standard policy might exclude.

- • Travelers Risk Control: free consultative service for business policyholders helping identify and reduce property and liability exposures.

Travelers is an excellent first call for homeowners wanting low rates combined with top-tier financial strength and claims service. Auto shoppers can do better on price and digital experience with GEICO or Progressive.

Farmers Insurance

Farmers Insurance Group is one of the largest U.S. personal lines insurers, offering auto, home, renters, life, business, and specialty insurance including rideshare, motorcycle, and RV coverage. Farmers is among the pricier national carriers — full-coverage auto averages approximately $220/mo nationally, well above GEICO's $156/mo. However, it offers strong specialty options and a robust discount menu, including Signal telematics (up to 15% off for safe driving), multi-policy discounts, and a HomeWatch smart home monitoring benefit. Farmers maintains an A (Excellent) AM Best rating and operates in all states except Hawaii. In 2024, Farmers raised rates sharply in many markets amid industry-wide catastrophe losses.

- • Signal telematics app: tracks driving behavior for up to 15% discount on auto premiums; enrollment discount applied immediately on sign-up.

- • HomeWatch: smart home monitoring service for Farmers home policyholders, providing water leak alerts and security monitoring with discounts for enrolled homes.

- • Rideshare coverage: Farmers offers dedicated rideshare insurance available in most states as a policy endorsement, covering drivers during all phases of app use.

- • Specialty vehicles: motorcycle, RV, boat, off-road vehicle, and classic car policies available under the Farmers umbrella.

- • Farmers University: online educational platform for agents, but customers benefit from highly trained agents who can explain complex multi-line policies.

Farmers is worth considering only if you have specialty vehicles, rideshare coverage needs, or complex multi-policy situations where an agent's expertise adds real value. For standard auto or home coverage, you will almost certainly pay less elsewhere.

Erie Insurance

Erie Insurance is a regional carrier operating in 12 states (IL, IN, KY, MD, NY, NC, OH, PA, TN, VA, WI, WV) plus Washington D.C., consistently earning top-tier J.D. Power satisfaction scores for both auto claims and overall customer experience. Erie's average full-coverage auto rate of approximately $84/mo is among the cheapest of any regional or national insurer, below both GEICO and Nationwide in its coverage territory. The company holds an A+ (Superior) AM Best rating and is notable for its Rate Lock feature — which freezes your premium until you add a vehicle or driver — and its guaranteed replacement cost on home insurance. Erie is distributed exclusively through independent agents.

- • Rate Lock: freeze your auto premium after the first year — your rate won't change unless you add a vehicle, driver, or move to a new address.

- • Guaranteed Replacement Cost for homes: pays to rebuild your home to its original quality even if the cost exceeds your policy limit, with no cap on overage.

- • Pet coverage included: up to $500 for pet injury or death in a covered auto accident, included at no extra cost on standard auto policies.

- • Erie Road Assistance: enhanced roadside service included with most auto policies; covers towing, lockout, fuel delivery, and flat tire service.

- • Auto Glass with no deductible: windshield and glass repair or replacement at no out-of-pocket cost with Erie's Platinum Plus coverage.

For drivers and homeowners in Erie's 12-state territory, Erie Insurance is the best all-around option — cheapest rates, top satisfaction scores, and unique features like Rate Lock and guaranteed replacement cost. The dealbreaker is geography: those outside its footprint cannot access it.

American Family Insurance

American Family Insurance (AmFam) is a Madison, Wisconsin-based mutual insurer operating in 19 states, primarily in the Midwest and Pacific Northwest. It offers auto, home, renters, life, business, and farm insurance, and is known for its KnowYourDrive telematics program and multi-policy discounts. AmFam's average full-coverage auto rates are competitive in its territory, and it holds an A (Excellent) AM Best rating. In 2023, AmFam completed its acquisition of CONNECT (formerly Costco Auto Insurance), expanding its digital reach. The company is distributed through approximately 3,400 exclusive agents and increasingly through direct digital channels.

- • KnowYourDrive telematics: mobile app-based program that monitors driving behavior with up to 40% potential savings for safe drivers.

- • Generational discount: if your parents were AmFam customers, you may qualify for a loyalty discount when starting your own policy.

- • Dream Protect bundles: packaged home and auto coverage with streamlined claims and single-deductible options for covered losses.

- • Diminishing deductible: $100 reduction each claim-free year on auto, up to $500 total.

- • Business insurance breadth: commercial auto, general liability, and workers' comp available for small businesses in most AmFam states.

American Family is a reasonable choice for Midwest and Pacific Northwest residents who value a strong agent relationship and want telematics savings. GEICO or Erie will generally beat it on base price in most overlapping states.

The Hartford

The Hartford is a Hartford, Connecticut-based insurer with over 200 years of history, offering auto, home, business, and employee benefits insurance. It is the exclusive auto and home insurance partner of AARP, and drivers who qualify through AARP membership typically access competitive rates and mature-driver benefits unavailable elsewhere. The Hartford holds an A+ (Superior) AM Best rating. Its TrueLane telematics program and RecoverCare home assistance benefit (which covers costs like cooking, cleaning, and transportation if you're injured in a covered auto accident) are differentiators. On the commercial side, The Hartford is one of the top small business insurers in the U.S.

- • RecoverCare: if injured in a covered auto accident, The Hartford pays for household services like cooking, cleaning, lawn care, and transportation during recovery — up to $2,500.

- • Lifetime renewability: as long as you meet certain criteria (including being an AARP member), The Hartford guarantees policy renewal regardless of claims history.

- • TrueLane telematics: safe driving discount program offering up to 25% savings for AARP policyholders who drive safely.

- • New Car Replacement (AARP policies): if your new car (under 15,000 miles) is totaled, The Hartford replaces it with a new vehicle of the same make and model.

- • Small business expertise: business owner's policy, workers' comp, and data breach coverage available; The Hartford ranked highly in J.D. Power's 2025 small commercial lines study.

The Hartford is the top pick for AARP members age 50+ who want guaranteed renewability, RecoverCare, and competitive rates through the AARP program. For younger drivers or those outside the AARP ecosystem, other carriers deliver better value.

Amica

Amica is the oldest mutual automobile insurer in the United States, founded in 1907 in Providence, Rhode Island. It sells auto, home, life, marine, umbrella, and renters insurance directly to consumers — no independent agents — and consistently earns J.D. Power's highest customer satisfaction ratings for both auto and home claims. Amica carries an A+ (Superior) AM Best rating. Its Platinum Choice auto program layers additional coverages including full glass, lock replacement, and trip interruption, and its dividend program returns a portion of premiums to policyholders. Amica is available in all states except Hawaii.

- • Dividend policy option: auto and home policyholders can choose a dividend-paying policy that returns 5–20% of premiums annually when the company performs well — effectively reducing the net annual cost.

- • Amica Platinum Choice Auto: comprehensive coverage tier adding full glass (no deductible), lock replacement, trip interruption up to $1,000, and airbag replacement.

- • No independent agent model: Amica sells directly, meaning no agent commissions are built into premiums — part of why it consistently earns high satisfaction ratings.

- • J.D. Power No. 1 rankings: Amica ranks first or near-first in J.D. Power's homeowners and auto claims satisfaction studies annually — the most decorated carrier for service quality.

- • Free credit monitoring: Amica includes identity fraud expense coverage and optional credit monitoring with many of its policies.

Amica is the best choice for policyholders who have had bad experiences with claim disputes at other insurers and are willing to pay a slight upfront premium for best-in-class service. The dividend policy is genuinely compelling over a 3–5 year horizon.

Chubb

Chubb is the world's largest publicly traded property and casualty insurer, headquartered in Zurich with significant U.S. operations. Its Masterpiece and Platinum lines of personal insurance are designed explicitly for high-value homes, luxury vehicles, fine art, jewelry, and watercraft — with features like agreed value settlement (no depreciation) and cash settlement without requiring a rebuild. Chubb holds an A++ (Superior) AM Best rating and is sold exclusively through independent agents. Standard homeowners policies include replacement cost coverage as a default, extended dwelling replacement cost up to 150% of the insured amount, and complimentary wildfire home assessments in fire-prone areas. Chubb is not price-competitive for standard policies.

- • Agreed value settlement: Chubb pays the full agreed value of your property at the time of loss — no depreciation deductions — for both auto and home.

- • Extended replacement cost: home policies automatically include up to 150% of the insured amount to cover construction cost inflation after a total loss.

- • Wildfire Defense Services: Chubb deploys private firefighting contractors to protect enrolled high-risk homes during active wildfire events — no extra charge.

- • Masterpiece Fine Art: worldwide scheduled coverage for paintings, sculptures, and collectibles with agreed value, mysterious disappearance coverage, and no deductible.

- • Worldwide protection: auto, jewelry, and personal property covered globally under standard Masterpiece terms — critical for frequent international travelers.

Chubb is the definitive choice for high-net-worth households with luxury homes, art collections, jewelry, or classic cars who need agreed value coverage and premium claims service. For anything below that asset threshold, standard carriers deliver better value at a fraction of the price.

MetLife

MetLife is one of the world's largest insurers, best known for group benefits including life, dental, vision, disability, and auto/home through employer-sponsored plans. Its MyDirect personal auto and home products are available through employers, associations, and directly, with group discount rates that can be 10–20% below retail market rates. MetLife's auto insurance is underwritten by subsidiaries and distributed through a combination of employer channels and direct sales. The company holds an A+ (Superior) AM Best rating and insures millions of U.S. employees through workplace benefit programs. MetLife divested its U.S. retail life insurance arm (now Brighthouse Financial) but remains active in group and specialty lines.

- • MyDirect group pricing: employer and affinity group members access negotiated rates that are typically 10–20% below standard retail market pricing.

- • Payroll deduction: group auto and home premiums can be deducted directly from paycheck — simplifies budgeting and eliminates missed payments.

- • Multi-line group discounts: combining auto and home through a group employer program layers an additional discount on top of the base group rate.

- • MetLife Legal Plans: employer-sponsored legal plan available as a voluntary benefit alongside auto and home — covers estate planning, traffic, real estate, and identity theft.

- • A+ AM Best financial strength rating across its insurance subsidiaries.

MetLife is worth checking if your employer offers group auto or home insurance — the 10–20% group discount can make it the cheapest option available to you. Without employer access, shop GEICO, Progressive, or Travelers instead.

Prudential

Prudential Financial is one of the largest life insurers in the United States, with over $1 trillion in assets under management and a history dating to 1875. It offers term life, whole life, universal life, and variable universal life insurance, along with annuities, retirement accounts, and workplace benefits. Prudential does not offer personal auto or home insurance; its core strength is in life insurance complexity and group benefit administration. The company holds an A+ (Superior) AM Best rating. Term life premiums from Prudential are published and run approximately $29–$45/mo for a healthy 35-year-old with $500,000 in coverage for 20 years, depending on gender and health classification.

- • PruTerm WorkLife 65: unique hybrid term product that pays the full death benefit plus a monthly disability benefit if you become disabled before 65 — not a common combination.

- • Accelerated underwriting: Prudential's Express Underwriting offers decisions in days without a medical exam for qualifying applicants under 60 seeking up to $3 million.

- • Variable Universal Life: cash value component tied to investment sub-accounts, allowing policyholders to participate in market growth with downside floor protection.

- • Employer group life: among the top group life and disability carriers for large employers, with broad network reach and administration tools.

- • Living needs benefit: accelerated death benefit rider allows terminally ill policyholders to access up to 60% of the face amount while still living.

Prudential is a strong choice for complex life insurance needs — especially permanent, variable, or disability-combo coverage — where an agent's expertise adds real value. For basic term life, shopping Policygenius or Ethos will typically find comparable or cheaper premiums with less friction.

New York Life

New York Life is the largest mutual life insurance company in the United States, with over $700 billion in assets under management and a history dating to 1845. Unlike stock insurers, New York Life has no shareholders — profits are returned to policyholders as dividends. The company offers term, whole, universal, and variable universal life insurance, along with annuities, long-term care, and disability income coverage. New York Life holds an A++ (Superior) AM Best rating — the highest available — and has paid policyholder dividends every year since 1854. Average whole life premiums for a healthy 35-year-old non-smoker typically start around $300–$500/mo for a $500,000 policy, though term products are more accessible.

- • Participating whole life dividends: New York Life has paid annual dividends to whole life policyholders every year since 1854, effectively reducing net premium cost over the policy's life.

- • A++ AM Best rating: highest financial strength rating available; $38 billion in surplus capital provides an exceptional margin for claims-paying.

- • Long-term care integration: hybrid products that combine whole life or universal life with long-term care benefits, addressing a major gap in most retirees' financial plans.

- • 10,000+ licensed agents: one of the largest proprietary agent networks in the country for in-person guidance on complex coverage needs.

- • Cash value growth: whole life policies accrue guaranteed cash value that can be borrowed against tax-free during the policyholder's lifetime.

New York Life is the best choice for individuals who want permanent life insurance from the most financially secure mutual carrier in the U.S., particularly for estate planning and long-term care integration. For straightforward term life, digital platforms like Ethos or Policygenius will find comparable coverage faster and often cheaper.

Mutual of Omaha

Mutual of Omaha is a Fortune 500 mutual insurer based in Omaha, Nebraska, with a particularly strong reputation in Medicare supplement (Medigap) insurance, long-term care, and final expense life insurance. It offers Medicare Supplement Plans A, B, C, D, F, G, K, L, M, and N — covering gaps in original Medicare — and is consistently rated among the top Medigap carriers for claims payment and premium stability. Mutual of Omaha also offers term life, whole life, disability income, and critical illness coverage. The company holds an A+ (Superior) AM Best rating. It ranks in the top tier of the Policygenius October 2025 Life Insurance Price Index as one of 13 carriers featured on the marketplace.

- • Medicare Supplement breadth: 10 standardized Medigap plan types available in most states with a strong track record of claims payment and rate stability.

- • Guaranteed acceptance final expense: whole life policies available to ages 45–85 with no medical exam and no health questions for coverage up to $25,000.

- • Living Promise policy: final expense whole life that builds cash value and pays an accelerated death benefit for terminal illness at no extra cost.

- • Disability income insurance: own-occupation and any-occupation disability products with benefit periods to age 65 — competitive with Unum and Principal.

- • Critical illness coverage: lump-sum benefit for heart attack, stroke, cancer, and other specified conditions — supplements major medical and disability income.

Mutual of Omaha is the best starting point for seniors evaluating Medicare supplement plans and final expense insurance — strong rates, reliable claims, and broad plan availability. For working-age term life shoppers, compare via Policygenius to ensure you're getting competitive pricing.

MassMutual

Massachusetts Mutual Life Insurance Company (MassMutual) is one of the largest and oldest U.S. mutual life insurers, founded in 1851 and based in Springfield, Massachusetts. It holds an A++ (Superior) AM Best rating — the highest level — and has paid dividends to participating whole life policyholders every year since 1869. MassMutual offers term life, whole life, disability income, long-term care, and annuity products. It was the parent company of Haven Life until Haven stopped selling new policies in January 2024, and MassMutual now services those existing policies directly. Term life premiums are competitive; a healthy 35-year-old can access $500,000 in 20-year coverage for approximately $25–35/mo depending on gender and health class.

- • Participating whole life dividends: MassMutual has paid annual dividends to whole life policyholders every year since 1869 — effectively reducing net premium cost over time.

- • A++ AM Best rating: maximum financial strength, sharing the top tier with USAA, GEICO parent Berkshire Hathaway, and New York Life.

- • LifeBridge program: MassMutual provides free 10-year, $50,000 term life policies to qualifying low-income applicants — a corporate social responsibility initiative.

- • C.M. Life Insurance Company: subsidiary used for issuing certain term products including Haven Life's existing policies, providing structural separation for specialized product lines.

- • Compass program: digital estate planning and beneficiary organization tools included for active policyholders.

MassMutual is an excellent choice for permanent life insurance and disability income coverage, particularly for high-earners who want long-term cash value accumulation from a carrier with the maximum financial strength rating. Term-only shoppers should still comparison shop via Policygenius.

Transamerica

Transamerica is one of the largest U.S. life insurance and financial services companies, a subsidiary of Aegon, with over 12 million customers. It offers term life, whole life, indexed universal life, final expense, and retirement annuity products. Transamerica is one of the 13 carriers featured in the Policygenius Life Insurance Price Index and consistently ranks as a competitive option for term life pricing. A 35-year-old non-smoker in preferred health can access $500,000 of 20-year term coverage for approximately $22–30/mo. Transamerica partnered with Bestow's B2B platform in September 2024 to launch a no-exam final expense product. It holds an A+ (Superior) AM Best rating.

- • Trendsetter Super convertible term: term policies convertible to permanent coverage at any point during the term without medical re-underwriting — a safety net for policyholders whose health changes.

- • No-exam term to $10M: accelerated underwriting for qualifying applicants offers up to $10 million in term coverage without requiring a paramedical exam.

- • Final Expense Express (with Bestow): instant-issue final expense product launched in 2024 through Bestow's platform; application approval in under 10 minutes.

- • Financial Foundation IUL II Express: Transamerica's IUL product launched on Bestow's platform in November 2025, offering faster IUL access through digital distribution.

- • Retirement income annuities: fixed, variable, and indexed annuities for retirement income planning alongside the life insurance product suite.

Transamerica is a solid term life option for applicants in good health who want competitive pricing and conversion flexibility. Use Policygenius to confirm it's the best rate for your profile before purchasing — pricing for some health classes is not always the lowest available.

Lemonade

Lemonade is a New York-based B-Corp and publicly traded insurtech founded in 2015 that uses AI to underwrite and pay claims across renters, home, condo, auto, pet, and term life insurance. Its renters policies start at $5/mo and average $12/mo ($140/yr) — 36–40% below the national average per LendingTree and ValuePenguin 2025 data. The company's AI claims system pays simple claims in as little as 3 seconds and runs 18 anti-fraud algorithms simultaneously. Lemonade auto insurance is only available in 9 states (AZ, CO, IL, IN, OH, OR, TN, TX, WA) and uses pay-per-mile pricing acquired from Metromile in 2022. Term life starts at $9/mo and is issued through Banner Life (Legal & General America). Lemonade takes a flat fee from premiums and donates surplus to charity through its Giveback program.

- • AI instant claims: files and pays simple claims in under 3 seconds using 18 anti-fraud algorithms — the fastest claims experience of any insurer of scale.

- • Giveback program: Lemonade takes a flat fee and donates leftover premiums to a charity chosen by the policyholder at signup — a structural social good component.

- • Tesla FSD discount: Lemonade offers a 50% discount on miles driven using Tesla Full Self-Driving (Supervised) mode in AZ and OR — unique in the auto insurance market.

- • Extra Coverage add-on: scheduled personal property coverage for jewelry, cameras, bikes, and art with no deductible and accidental loss protection — beyond standard renters scope.

- • Bundle discount: combining any two or more Lemonade products (e.g., renters + pet + auto) unlocks an automatic bundle discount across all policies.

Lemonade is the best renters insurance for urban renters who want the cheapest policy and fastest claims. For homeowners or anyone outside Lemonade's auto states, supplement with a traditional carrier for the coverage gaps. The complaint rate is worth watching.

Policygenius

Policygenius is an independent insurance marketplace founded in 2014, now operated under the Zinnia backend for faster quoting. It partners with 13 major life insurance carriers — including Corebridge Financial, Legal & General America, Mutual of Omaha, Pacific Life, Protective, Prudential, and Transamerica — and allows side-by-side comparison of real-time quotes across all of them. Policygenius is free to use; it earns a commission from carriers when users purchase. For auto and home, it connects users with carrier websites for quotes rather than generating fully real-time figures. Over 30 million people have used Policygenius to shop insurance. Its October 2025 Life Insurance Price Index shows life insurance rates have remained stable with only 0.08% monthly fluctuation.

- • 13 life insurance carrier partners: real-time quotes from Corebridge, Legal & General, Lincoln, Mutual of Omaha, Pacific Life, Protective, Prudential, SBLI, Symetra, Transamerica, and others in one dashboard.

- • Licensed expert access: Policygenius employs licensed insurance advisors who can answer policy questions and guide purchase decisions via phone and chat — not just a form-fill tool.

- • Life Insurance Price Index: proprietary monthly benchmark tracking average term life rates across 13 carriers — the most granular public pricing data in the industry.

- • Coverage recommendations: after completing the application, Policygenius flags underinsurance risks based on income, dependents, debt, and state requirements.

- • Estate planning integration: the platform offers wills, trusts, and beneficiary management tools alongside life insurance — broader financial planning scope than most competitors.

Policygenius is the best single destination for life insurance comparison — the combination of 13 real-time carrier quotes and licensed advisors is unmatched. Use a dedicated auto comparison platform like Insurify for property and casualty needs.

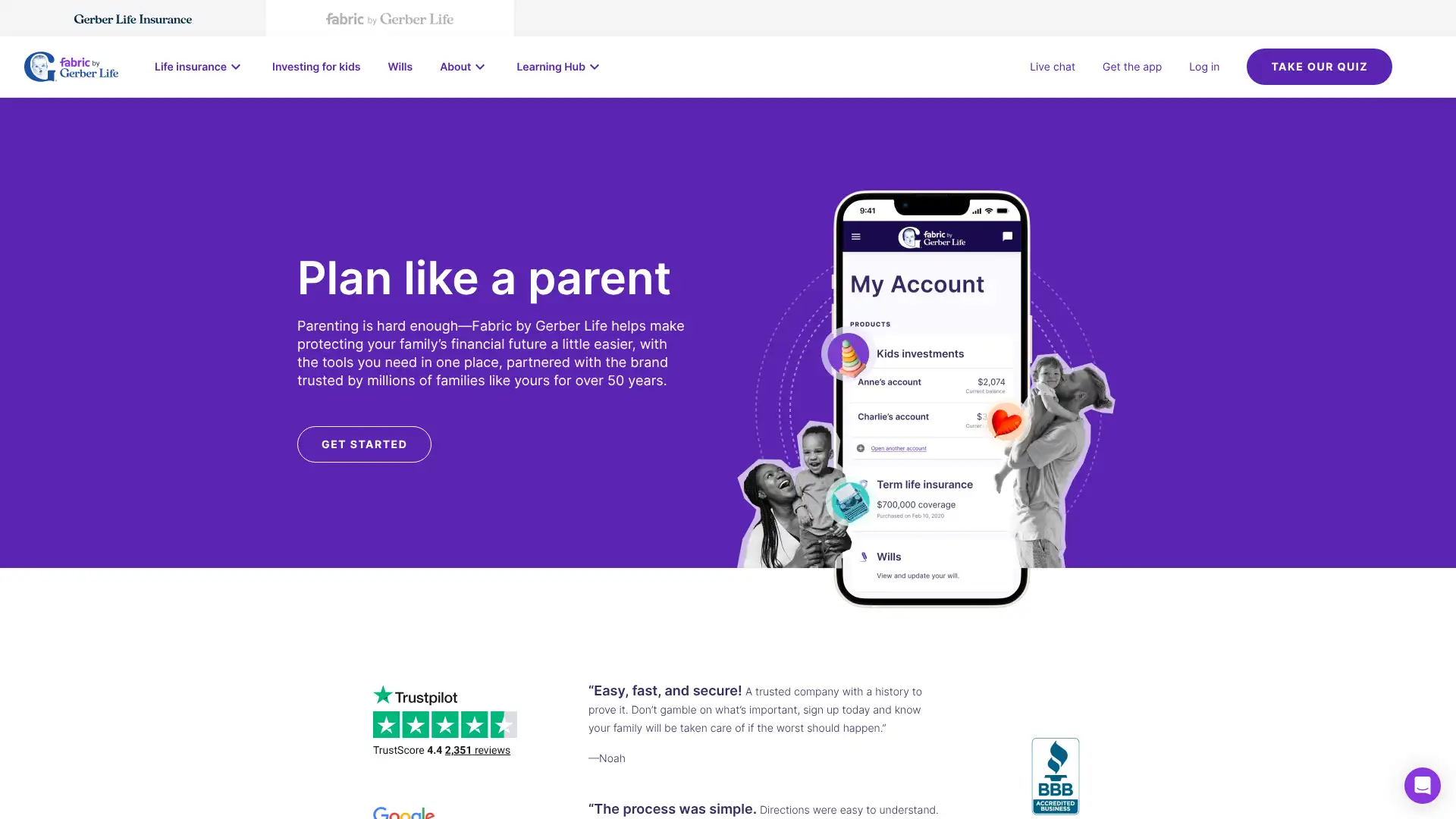

Fabric by Gerber Life

Fabric is a digital life insurance platform founded in 2015, acquired by Western & Southern Financial Group in 2021, and rebranded as Fabric by Gerber Life under Western & Southern's Gerber Life Insurance Company subsidiary. Policies are issued by Gerber Life Insurance Company (A+, AM Best) and Western-Southern Life Assurance Company. Fabric offers term life insurance for ages 21–70 in all states except New York, with terms from 10–30 years and coverage from $100,000 to $5 million. A 25-year-old female can access $100,000 in coverage for as little as $7.85/mo. The application takes approximately 10 minutes online with no medical exam required for most applicants. Fabric also includes free will creation and UGMA investment account tools within its app.

- • 10-minute application: fully online term life application with no medical exam for qualifying applicants under $1.5 million in coverage — instant decision in most cases.

- • Free will creation: Fabric provides a legally valid digital will for policyholders and spouses within the app — valued at over $898 if done through a traditional attorney.

- • UGMA investment account: parents can open a custodial investment account for their child directly in the Fabric app alongside their life insurance policy.

- • 30-day money-back guarantee: cancel within 30 days for a full refund — no questions asked, unique among major life insurance carriers.

- • A+ (Superior) AM Best rating (Gerber Life Insurance Company): strong financial backing from Western & Southern Financial Group, one of the strongest mutual insurance groups in the U.S.

Fabric is the top pick for parents of young children who want term life insurance, a free will, and a kids' investment account from a single app in under 15 minutes. New York residents and those needing permanent coverage need to shop elsewhere.

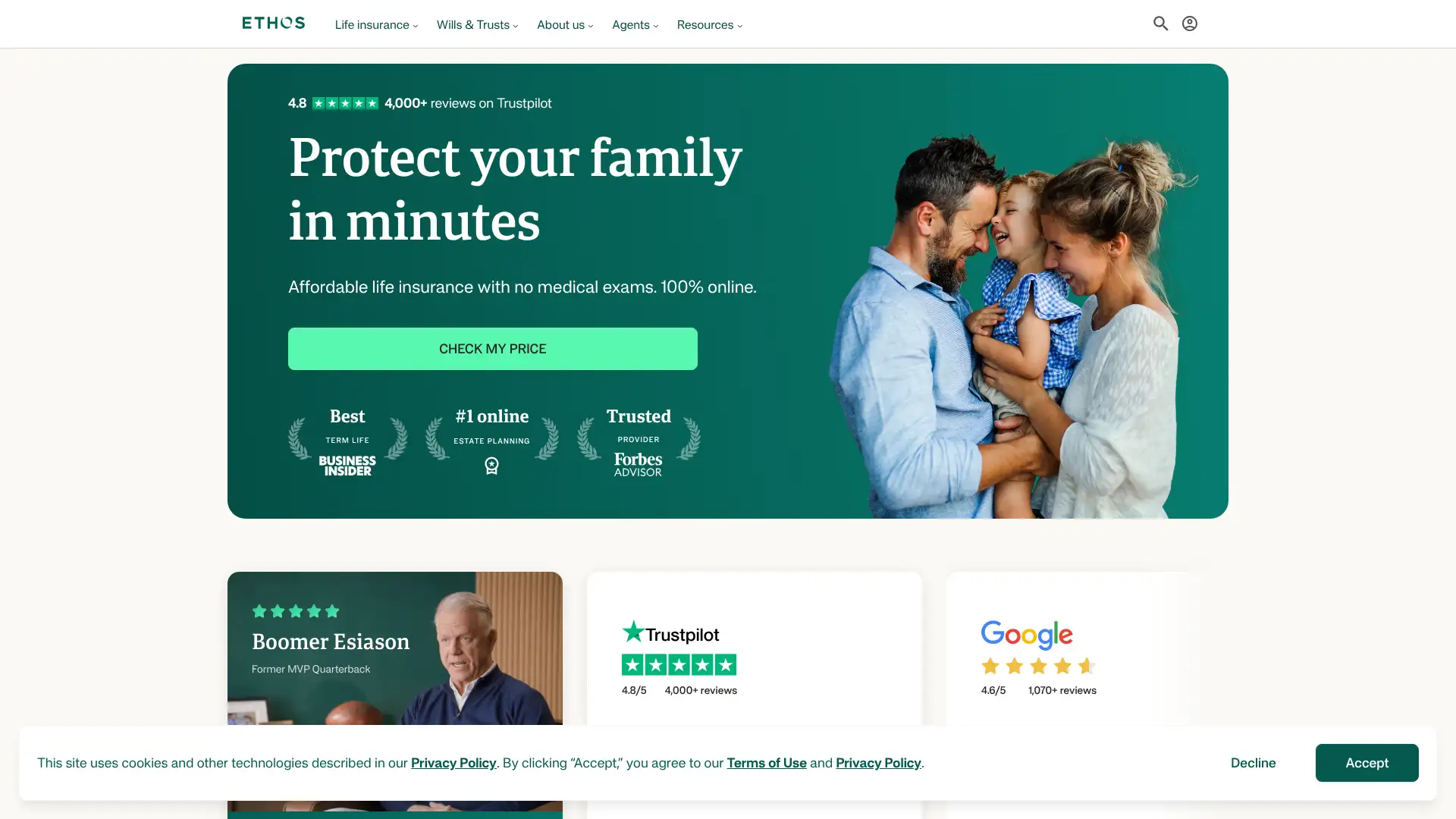

Ethos

Ethos is a San Francisco-based digital life insurance agency founded in 2016 that acts as a licensed broker selling policies issued by carriers including Legal & General America (Banner Life), Ameritas, Protective, and TruStage. It offers term life (10–40 year terms) for ages 20–75 with up to $3 million in coverage, whole life for seniors (ages 66–85, up to $30,000), and indexed universal life insurance. Ethos uses automated data underwriting — no medical exam — for most applicants, with same-day approval in most cases. A healthy 35-year-old can expect to pay approximately $20–30/mo for $500,000 of 20-year term coverage. Policies include a 30-day money-back guarantee, and policyholders receive free will and estate planning tools. Ethos is available in 49 states (not New York).

- • Laddering system: if your health profile disqualifies you from a preferred term policy, Ethos automatically offers the next-available product rather than a flat rejection.

- • Same-day coverage: most applicants receive an instant decision and active coverage within minutes of completing the online application.

- • Free estate planning tools: policyholders receive complimentary will creation, trust formation guidance, and beneficiary management tools valued at $898+.

- • 40-year term option: Ethos offers 40-year term life, longer than most competitors (most max at 30 years) — valuable for younger applicants securing lifelong income replacement.

- • Whole life for seniors with guaranteed acceptance: no health questions for ages 66–85 up to $30,000, covering final expenses for applicants declined elsewhere.

Ethos is the best choice for applicants who want fast, no-exam coverage up to $3 million and appreciate the laddering system's inclusivity. Be aware that post-purchase policy management goes through the issuing carrier, not Ethos — read your policy's carrier carefully before purchasing.

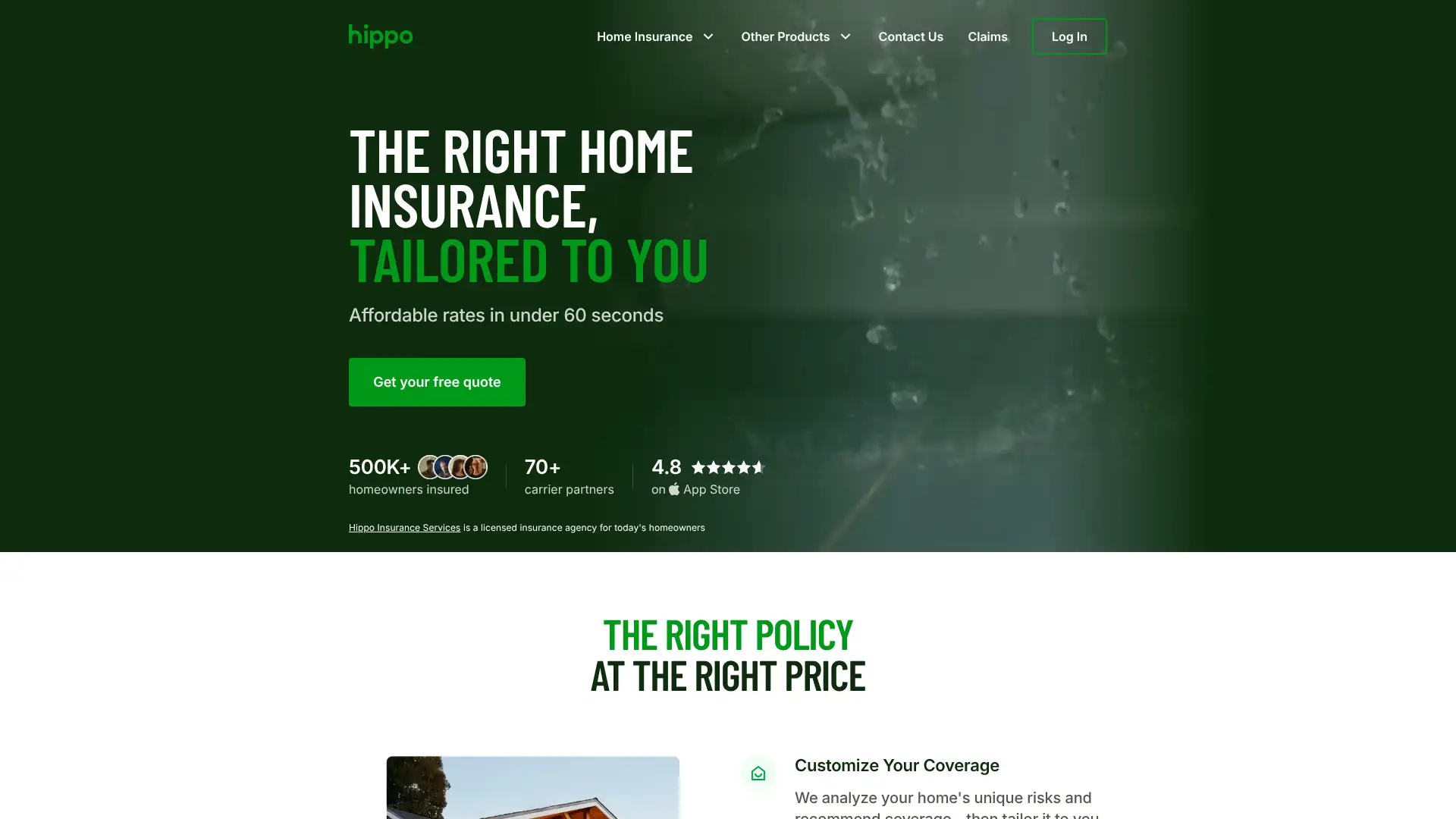

Hippo

Hippo is a Silicon Valley-born home insurance provider founded in 2015 that emphasizes smart home technology and preventative loss mitigation. It pairs policies with complimentary smart home devices (water leak sensors, smoke alarms, security cameras) from partners including Notion, Kangaroo, and SimpliSafe, and discounts premiums by up to 13% for monitored systems. Hippo does not currently sell its own homeowner policies broadly through its website — following substantial weather-related losses in 2023 it paused direct HHIP writing. Instead, it matches users with third-party carrier partners. Its own Spinnaker Insurance Company subsidiary underwrites some policies in select markets. Hippo achieved a financial turnaround in 2025 with $58 million in net income. Average Hippo-distributed policies historically ran approximately $1,761/yr — 17% below competitor averages.

- • Free smart home kit: qualifying new policyholders receive a complimentary smart home monitoring system from Kangaroo, Notion, or SimpliSafe at no additional cost.

- • Smart home discount: up to 10% for self-monitored systems and 13% for professionally monitored systems — one of the higher home technology discounts in the industry.

- • Home office coverage: standard policies include higher limits for computers, electronics, and office equipment — differentiating coverage for remote workers.

- • Hippo Home app: maintenance reminders, alerts for water leaks and freeze events, and claims management in one mobile interface.

- • Coverage for appliances: standard Hippo policies historically included up to $100,000 for appliance breakdown — broader than most standard homeowners policies.

Hippo is worth a quote for homeowners who actively want smart home technology integrated into their coverage and don't mind the current third-party carrier model. The claims experience inconsistency is a real concern — confirm the specific carrier backing your policy before signing.

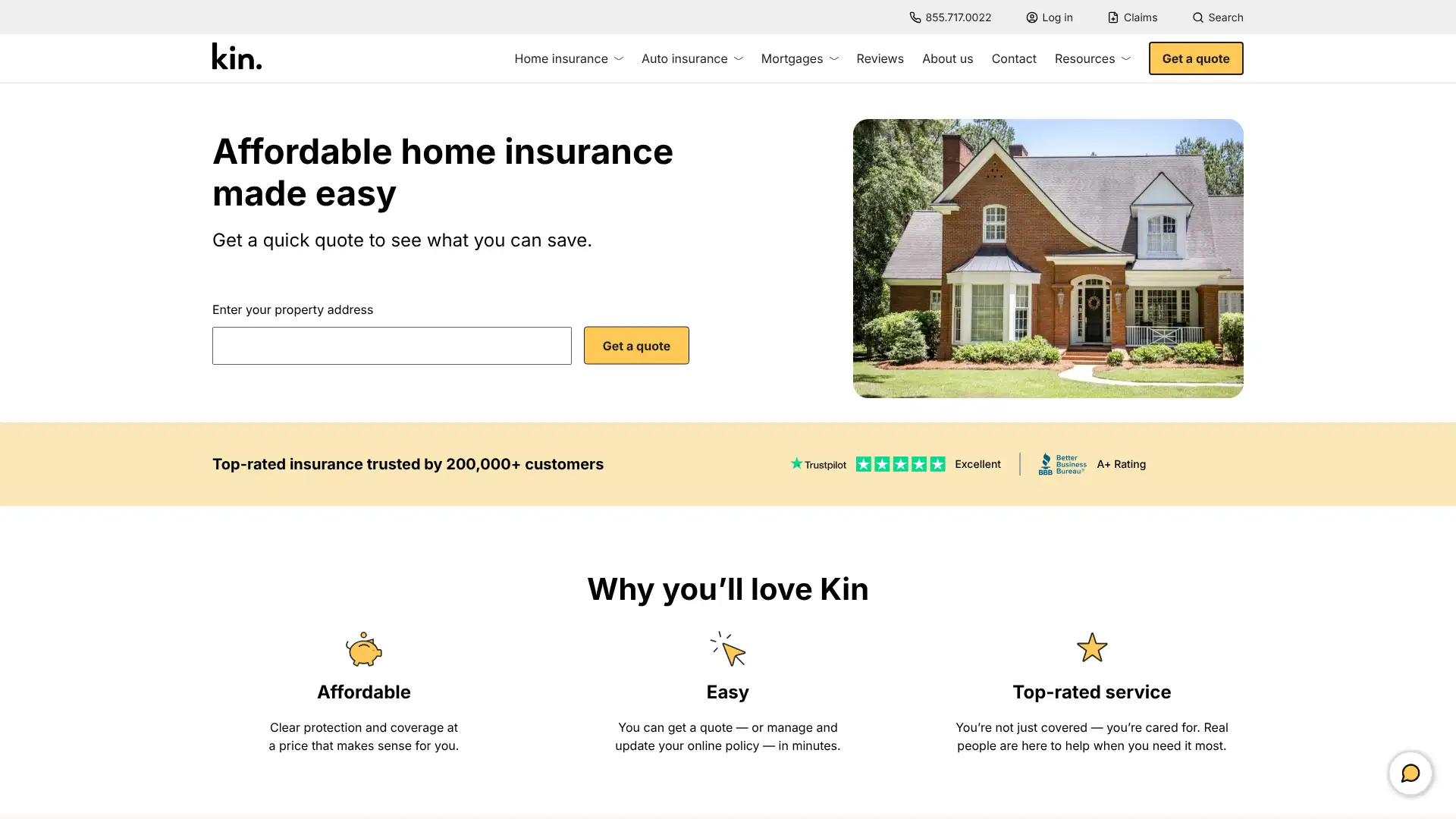

Kin

Kin is a Chicago-based insurtech founded in 2016 that specializes in home insurance for properties in catastrophe-prone states where traditional carriers have withdrawn or priced out homeowners. It operates in 13 states (AL, AZ, CA, CO, FL, GA, LA, MS, MO, SC, TN, TX, VA) as of early 2026, having expanded to California in March 2025 and Colorado in June 2025. Kin reported $634.8 million in gross written premium in 2025 — up 28% year-over-year — with 240,000+ policies written. Customers who switched to Kin saved an average of $989/year per a 2023–2024 survey. Kin's NAIC complaint index is only 61% of the expected average for its size. It introduced bundled home and auto in Florida and Texas in January 2026. Policies are underwritten by Kin Interinsurance Network and Kin Interinsurance Nexus Exchange (policyholders are owners), rated A (Exceptional) by Demotech.

- • Disaster-state specialization: actively insures high-risk properties in FL, LA, TX, CA, and other states where most major carriers have withdrawn or raised rates dramatically.

- • Fast online quoting: Kin's website uses public property records, aerial imagery, and permit data to generate quotes in approximately 3 minutes with minimal input.

- • Private flood insurance: available in select states as a policy add-on, with shorter waiting periods and higher limits than the federal NFIP.

- • Replacement cost on personal property: Kin includes replacement cost coverage (not actual cash value) as the default for personal belongings — more generous than many competitors at the same price point.

- • Reciprocal exchange model: policyholders are members of the exchange and share in underwriting profits — aligning incentives between Kin's management and its insured population.

Kin is the best available option for homeowners in high-risk states who have been dropped by traditional carriers or face unaffordable renewal quotes — it's filling a gap the market has created. The regulatory fines and lack of major AM Best rating are legitimate concerns to weigh before purchasing.

Branch

Branch is a Columbus, Ohio-based B-Corp insurtech founded in 2018 by Steve Lekas and Joe Emison that pioneered instant home-and-auto bundling — its platform claims to generate a bundled quote and bind coverage in as little as 37 seconds using just a name and address. Branch raised $51 million in a Series D in October 2024 led by American Family Ventures, reaching total equity funding of $280 million. It operates as a reciprocal exchange in many states (owned by its policyholders) and distributes through its website and app. Branch is available in approximately 36 states plus Washington D.C. and offers home, auto, renters, umbrella, motorcycle, boat, and ATV coverage. Customers save an average of $548/year per Branch's own data. The company invested in AI-powered claims operations with Kyber in 2024, reducing claims correspondence turnaround from hours to minutes.

- • 37-second bundle binding: Branch's instant-bind process binds both a home and auto policy in under 37 seconds using just your name and address — no lengthy questionnaire.

- • Community Drive telematics: safe driving program offering up to 20% auto premium savings; automatic 2% discount for enrollment; Nextbase dash cam integration adds 8% additional savings.

- • Homeshare and rideshare coverage: explicitly includes coverage for Airbnb hosting and rideshare driving as policy options — cleaner than traditional carriers that require separate endorsements.

- • Reciprocal exchange structure: policyholders are exchange members and may share in underwriting profits — similar to Erie and Kin's policyholder-owned models.

- • AI claims platform: partnership with Kyber AI in 2024 to automate claims correspondence; significant customer experience improvement over prior claims workflows.

Branch is the best option for homeowners who want the fastest possible bundled quote and are comfortable with a newer carrier. The renewal rate increase complaints are worth investigating before committing long-term — get a multi-year price projection before signing.

Root Insurance

Root Insurance is a Columbus, Ohio-based public insurtech (NYSE: ROOT) founded in 2015 that built its entire pricing model on telematics — you drive with the Root app for a test period, and your quote is set based primarily on how safely you drive, not your demographic profile. Root achieved profitability in 2025 with net income of $40.3 million on $1.52 billion in revenue (up 29%). It operates in 36 states and has collected over 20 billion miles of telematics data. Root pledged to eliminate credit scores from its pricing model by 2025 — though ValuePenguin notes the company deleted this announcement from its website and credit scores remain a factor in some states. Average full-coverage rates average approximately $1,120 per year, significantly below the national average for clean-record drivers. Root offers standard auto coverage plus roadside assistance (included in all policies) and renters insurance in select states.

- • Telematics-first rating: driving behavior accounts for over 52% of premium determination — the highest weighting of any major insurer, translating directly to savings for proven safe drivers.

- • Test drive period: Root monitors your driving for 2–4 weeks before issuing a final quote, using real driving data rather than proxies like credit score.

- • Roadside assistance included: every Root policy includes roadside assistance for 3 incidents per 6-month term at no additional cost — unusual for a low-cost carrier.

- • 3-minute app claim filing: Root advertises claim filing in approximately 3 minutes via its mobile app — competitive with the fastest digital insurers.

- • Embedded insurance partnerships: Root has embedded its quoting engine within Carvana's checkout flow, Kikoff's financial app (January 2026), and Hyundai dealerships (2025).

Root delivers real savings for safe, low-mileage drivers willing to complete a telematics test drive — rates around $1,120/yr for good drivers are genuinely compelling. The data breach fine, complaint index, and credit score pledge controversy are serious issues to weigh against the pricing advantage.

Clearcover

Clearcover is a Chicago-based auto insurance insurtech founded in 2016 that uses an API-first, low-overhead model to deliver lower premiums than legacy carriers. It is available in 19 states and targets standard and, since January 2025, non-standard drivers in Texas through its Clearcover General Agency subsidiary. Average full-coverage auto costs approximately $1,994/yr — about 23% below the national average per Coverage Cat 2025 data. Clearcover reached unicorn status at a $1 billion valuation in 2021 and has raised $432 million total. It offers standard auto coverage plus rideshare, roadside assistance, and alternate transportation (up to $30/day for rideshare or public transit if your car is in the shop). Claims are processed via app; Clearcover advertises average claims decisions in 6.8 minutes.

- • 6.8-minute average claims decision: Clearcover's AI-powered claims system delivers among the fastest automated claim assessments in the industry.

- • Alternate Transportation coverage: unique add-on paying up to $30/day for rideshare, public transit, or rental while your car is being repaired.

- • Rideshare coverage endorsement: available add-on covering you during all phases of rideshare driving, including app-on waiting time — does not cover delivery services.

- • Discounts built into quotes: Clearcover automatically applies eligible discounts (safe driving record, continuous insurance, vehicle safety features) rather than requiring you to ask.

- • Car Care maintenance savings: in-app access to discounts at 23,000 maintenance shops nationally for up to 25% off services — available in select states.

Clearcover is worth a quote if you're in one of its 19 states — 23% below-average rates without telematics is compelling. The market contraction signals and high complaint index are warning signs; confirm Clearcover still actively writes in your state before purchasing.

Jerry

Jerry (Jerry Services, Inc.) is a Palo Alto-based licensed insurance broker and comparison app founded in 2019 that uses AI and machine learning to compare auto, home, and renters insurance from over 50 carriers in minutes. The app-first platform has generated over 25 million quotes for more than 2 million users. Jerry claims average savings of $800 per year based on Y Combinator data, and the process takes approximately 45 seconds from sign-up to initial quotes. Jerry's differentiation is its GarageGuard feature (maintenance reminders, recall notifications, repair cost estimates), DriveShield telematics scoring, and PriceProtect automatic re-shopping every 6 months with price-drop alerts. Jerry does not mark up quotes — it earns commissions from carriers on policy purchases.

- • 45-second sign-up to initial quotes: Jerry uses public records and your phone number to autopopulate vehicle and address information, minimizing manual data entry.

- • GarageGuard: maintenance reminders, service cost benchmarks at local shops, and vehicle recall notifications — extending Jerry beyond pure insurance comparison into car ownership.

- • PriceProtect automatic re-shopping: Jerry monitors carrier pricing every 6 months and sends price-drop alerts when a cheaper equivalent policy is available.

- • DriveShield driving score: optional telematics scoring that tracks trips, provides per-trip feedback, and generates a driving safety report for insurance purposes.

- • Comparison from 50+ carriers: includes major national carriers and specialty providers including pay-per-mile options like Mile Auto — more niche coverage than most competitors show.

Jerry is the best app for drivers who want fast AI-powered comparison and automatic renewal re-shopping in one place. Supplement with Insurify or The Zebra to catch regional carriers Jerry misses before making a final decision.

Gabi

Gabi (now operating as Experian Insurance Services following a $320 million acquisition by Experian in October 2021) is a digital insurance comparison platform founded in 2016. Its core differentiator is allowing users to upload their existing declarations page — rather than re-entering all their information — and then comparing their current policy limits and pricing against 40+ regional and national carriers including Nationwide, Travelers, Progressive, Safeco, and Kemper. According to Gabi, users save up to $960 per year on average. The platform covers auto, home, renters, condo, landlord, umbrella, RV, and motorcycle insurance. Gabi is available in all 50 states, licensed as Gabi Personal Insurance Agency (California DI License 0L31621). Recent reviews indicate service quality declined post-Experian acquisition, with a current BBB customer rating of 1.72/5.

- • Declarations page upload: users can upload their current insurance declarations page and Gabi's team manually reviews it to compare the exact same limits against other carriers — true apples-to-apples comparison.

- • 40+ carrier network: includes Nationwide, Travelers, Progressive, Safeco, Encompass, and Kemper plus regional carriers; broader than Jerry's 50+ but with different carrier mix.

- • Multi-product comparison: simultaneously compares auto, home, renters, condo, umbrella, RV, and motorcycle — one of the broadest comparison scopes of any U.S. platform.

- • Assisted shopping: Gabi offers phone and chat support from licensed agents to finalize quotes and facilitate switching — more hands-on than purely automated tools.

- • Privacy commitment: Gabi does not sell user data to lead generation sites; comparison is anonymous until you choose to proceed with a specific carrier.

Gabi's declarations page upload is genuinely differentiated for existing policyholders who want a true coverage-equivalent comparison. The 48-hour wait and post-acquisition service decline make it less competitive for users who want instant results — use Insurify for speed, Gabi when accuracy of limit comparison matters most.

The Zebra

The Zebra is an Austin, Texas-based insurance comparison platform founded in 2012 and named PropertyCasualty360's 2025 Agency of the Year. It compares quotes from 100+ insurance companies for auto, home, renters, and condo insurance across all 50 states. The Zebra does not sell your data to lead generators and does not require your phone number to get quotes. Its in-house team of 100+ licensed agents can finalize purchases and provide coverage guidance by phone or chat. According to The Zebra, users save an average of $922 on combined home and car insurance. Unlike Insurify, The Zebra has been criticized for not always providing instant real-time quotes — some users receive redirects to partner websites rather than finalized prices.

- • 100+ carrier comparisons: one of the broadest comparison networks for auto and home in the U.S., covering regional and national carriers side by side.

- • 100+ licensed in-house agents: unlike most comparison sites that redirect users to carrier websites, The Zebra's agents can finalize and bind policies within the platform.

- • No phone number required: Zebra explicitly does not ask for your phone number to generate quotes, preventing spam calls — a differentiator from many lead-gen competitors.

- • Price drop alerts and renewal tips: post-purchase tools that notify users when rates drop and remind them to re-shop before auto-renewal.

- • PropertyCasualty360 2025 Agency of the Year: recognized as the top digital insurance agency in the U.S. for 2025.

The Zebra is the best comparison platform for shoppers who want agent support alongside quotes and are willing to trade some instant-quote functionality for in-house bindable coverage. For purely digital, fastest-possible instant quotes, Insurify delivers more real-time results.

QuoteWizard

QuoteWizard is an LendingTree-owned insurance marketplace founded in 2006 and headquartered in Seattle. It compares quotes for auto, home, renters, health, life, and Medicare insurance across a large network of carriers. QuoteWizard generates quotes by connecting users with licensed insurance agents and carriers — some quotes are instant, others require an agent callback. Unlike Insurify, QuoteWizard operates primarily as a lead-generation marketplace, which means entering your information may result in agent calls from multiple carriers. The platform is free to use and earns revenue from carriers and agents for qualified leads. It covers all 50 states and has served tens of millions of users.

- • Multi-product comparison: one of the few platforms that covers auto, home, health, life, and Medicare in a single portal — broader product scope than Insurify or The Zebra.

- • Agent connection model: for complex coverage needs (health, Medicare, life), QuoteWizard connects users with licensed agents rather than trying to automate underwriting, which can provide better guidance.

- • National availability: operates across all 50 states with coverage for most major insurance product lines.

- • LendingTree ownership: part of a major fintech ecosystem; QuoteWizard benefits from LendingTree's financial services infrastructure and data scale.

- • Educational content: extensive library of insurance guides, state-by-state coverage requirements, and cost comparison articles that are among the most SEO-ranked insurance education resources online.

QuoteWizard's broad product coverage makes it useful for shoppers who want one portal for health, Medicare, and property coverage. Be prepared for follow-up calls — the lead-gen model is a significant trade-off versus spam-free platforms like Insurify or The Zebra.

Insurify

Insurify is a Cambridge, Massachusetts-based licensed digital insurance agency founded in 2016 that has served over 10.4 million users and generated 196 million+ quotes across 500+ carrier integrations. It is consistently rated the highest of any insurance comparison platform on both Trustpilot (4.7/5 from 14,000+ reviews) and the Better Business Bureau (A+, accredited). In February 2026, Insurify launched the first insurance ChatGPT app, allowing users to compare rates through OpenAI's platform. In 2026, the company also introduced Insurify Car — a liability-only auto insurance product with weekly payment options. Insurify does not sell user data and earns commissions only from carrier partnerships. Average reported user savings reach up to $1,100/year.

- • 500+ carrier integrations: the most carrier connections of any U.S. comparison platform, delivering real-time instant quotes for both regional and national insurers in most states.

- • SmartRate background monitoring: continuously reshops your policy and sends price-drop notifications automatically — no manual re-shopping required.

- • ChatGPT app: the first insurance ChatGPT integration (launched February 2026), allowing natural-language insurance comparison directly in OpenAI's platform.

- • 85,000+ user reviews on insurance companies: Insurify maintains a verified customer review database for 120+ carriers, enabling post-quote insurer research in one place.

- • Licensed in all 50 states: Insurify can finalize and bind policies in-house with no redirect to carrier websites — end-to-end purchase within the Insurify platform.

Insurify is the best all-around auto and home insurance comparison platform in the U.S. — most carrier integrations, top-rated service, no spam, and licensed binding in all 50 states. Use Policygenius alongside it for life insurance needs.

CoverHound

CoverHound is a San Francisco-based digital insurance marketplace acquired by CNA Insurance in 2017 for a reported $40 million. It operates as an independent comparative platform offering personal lines (auto, home, renters) and commercial lines (business owners policy, general liability, professional liability, commercial auto) across a network of carrier partners. CoverHound's commercial insurance comparison is its key differentiator — it allows small businesses to compare BOPs, general liability, and professional liability policies side by side, which most consumer comparison platforms don't offer. It covers all 50 states and earns revenue through carrier commissions. CNA's backing provides financial stability.

- • Small business insurance comparison: allows side-by-side comparison of business owners policies, general liability, and professional liability — a product segment most consumer platforms ignore.

- • CNA-backed credibility: CNA Insurance (one of the largest U.S. commercial insurers) provides operational stability and credibility for the platform.

- • Personal + commercial in one portal: individuals and business owners can compare both personal and commercial coverage in the same platform.

- • 50-state availability: nationally licensed for both personal and commercial insurance comparison.

- • Quick quote interface: designed to deliver comparative quotes in minutes for standard commercial coverage like BOP and GL.

CoverHound is the most relevant option specifically for small business owners who need to compare commercial coverage alongside personal lines in one place. For personal insurance only, Insurify delivers a significantly better experience.

Ladder

Ladder is a Palo Alto-based digital life insurance company founded in 2015 that offers one unique feature most term life carriers cannot match: the ability to reduce (ladder down) your coverage amount at any time without cancellation fees or new underwriting — as your mortgage balance drops or your kids grow up, you pay less. Ladder offers term life for ages 20–60, with coverage from $100,000 to $8 million for qualified applicants, in 10–30 year terms. Instant approval is available for many applicants without a medical exam for policies up to $3 million. A healthy 30-year-old can access $500,000 in 20-year coverage for approximately $16–22/mo. Policies are issued by Fidelity Security Life Insurance Company of New York (NY) and Allianz Life Insurance Company of New York for NY residents.

- • Coverage laddering: reduce your coverage amount at any point during the term without fees or new underwriting — as your financial obligations decrease, your premium drops immediately.

- • Up to $8 million in coverage: one of the highest coverage limits available online; most digital carriers cap at $3 million for no-exam and $5 million total.

- • Instant decisions up to $3 million: for qualifying applicants, instant approval without a medical exam — no waiting for a scheduled exam.

- • 30-day refund: cancel within 30 days for a full refund, consistent with most digital life insurance competitors.

- • Simple product design: Ladder offers only term life — no whole life, UL, or final expense options, keeping the product focused and the pricing transparent.

Ladder is the best term life insurance option for professionals with high and declining financial obligations — the ability to reduce coverage as your mortgage or income-replacement needs decrease is a real, money-saving feature. For those who might eventually need permanent coverage, check Ethos or Policygenius.