28 Best Business Credit Cards for Entrepreneurs in 2026

Business credit cards range from traditional bank rewards cards with travel perks to modern fintech charge cards built for startups, and fleet-specific fuel cards for transport businesses. This guide covers 27 actively operating options across all categories, with pricing verified in March 2026. Whether you need points, cashback, spend controls, or per-gallon fuel discounts, there is a card here built for your business.

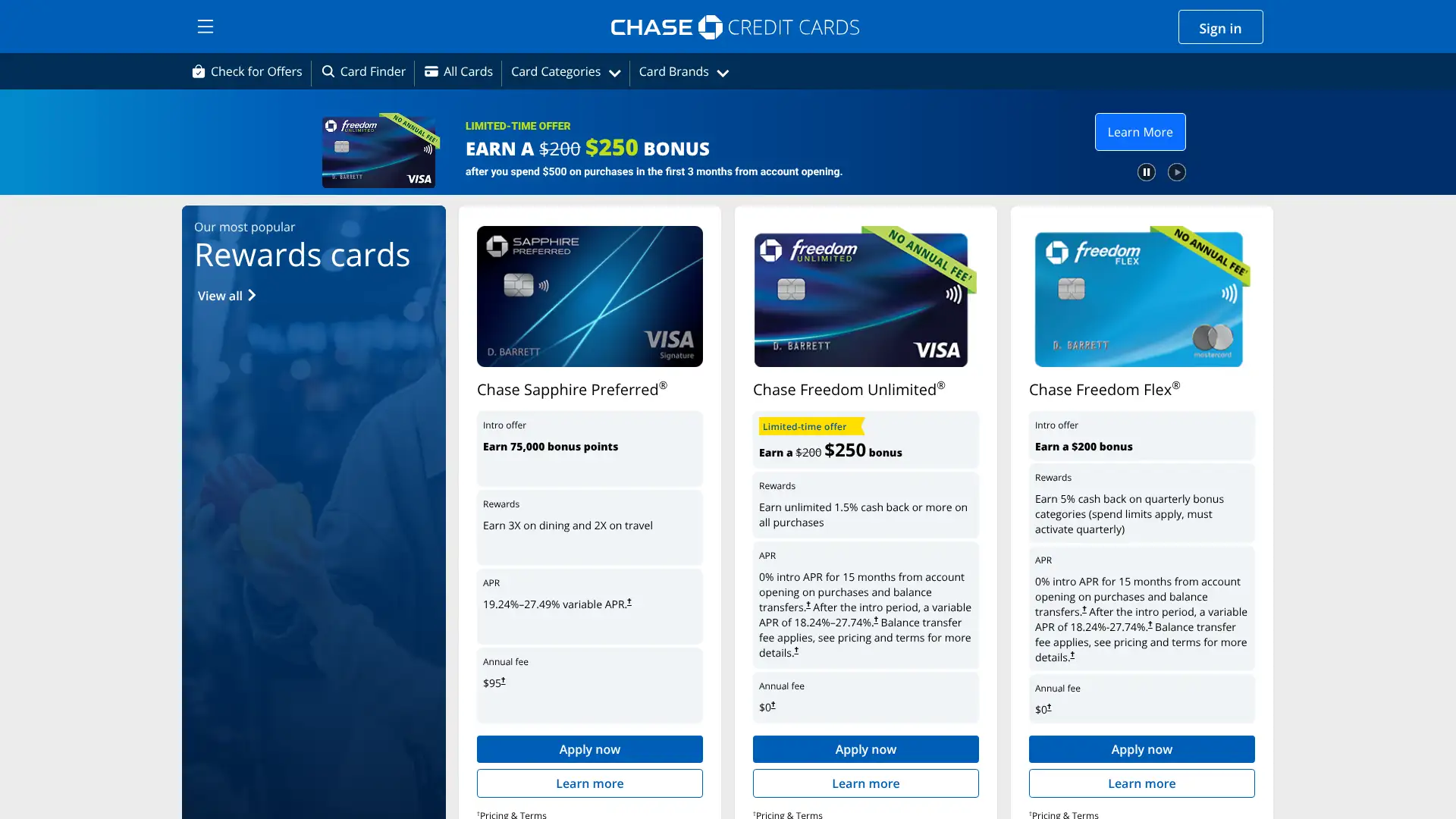

Chase Ink Business

Chase offers four Ink Business cards covering nearly every reward preference. The Ink Business Cash and Ink Business Unlimited both carry $0 annual fees, while the Ink Business Preferred charges $95/year and earns 3x points on travel, shipping, telecom, and social media advertising on the first $150,000 spent annually. The premium Ink Business Premier charges $195/year, earns 2.5% cash back on purchases of $5,000 or more, and 2% on all others. All cards issue employee cards at no extra cost and pool rewards into Chase Ultimate Rewards. As of March 2026, Chase announced that cash-back rewards can no longer be transferred to an outside bank account, only to eligible Chase accounts.

- • Ink Business Cash earns 5% cash back on office supplies and internet/cable/phone services on the first $25,000 spent per account anniversary year.

- • Ink Business Preferred earns 3x Chase Ultimate Rewards points in four key business categories, with points transferable to 14 airline and hotel partners.

- • Ink Business Premier is a pay-in-full charge card with no preset spending limit designed for high-spend businesses making frequent large purchases.

- • Employee cards are free on all four Ink cards with customizable individual spending limits and no additional annual fee.

- • All Ink cards include purchase protection up to $10,000 per claim and extended warranty protection, plus auto rental collision damage waiver.

Chase Ink Business cards are the best default choice for small businesses that want reliable rewards, strong travel redemption value, and the option to start free. The Ink Business Preferred is the standout pick for businesses that spend heavily on digital advertising, travel, and shipping. Businesses making frequent large purchases above $5,000 per transaction should evaluate the Ink Business Premier, though its lack of transfer partner access is a meaningful limitation compared to the Preferred.

American Express Business Gold

The American Express Business Gold Card automatically earns 4x Membership Rewards points in the two categories where a business spends the most each billing cycle from six eligible options: U.S. media advertising, U.S. purchases at gas stations, restaurants, shipping, transit, and wireless. The 4x rate applies to the first $150,000 in combined purchases from the top two categories per calendar year, then drops to 1x. The card carries a $375 annual fee and also earns 3x on flights and prepaid hotels booked through amextravel.com. Monthly credits of up to $20 at FedEx, Grubhub, and office supply stores (up to $240/year), plus a Walmart+ membership credit of up to $12.95/month, help offset the fee for qualifying businesses.

- • Automatic 4x Membership Rewards on the two categories where the business spends most each billing cycle, chosen from six eligible categories with no manual selection needed.

- • 3x Membership Rewards points on flights and prepaid hotels booked through amextravel.com, stackable with airline and hotel loyalty programs.

- • Up to $240/year in statement credits at FedEx, Grubhub, and eligible office supply stores ($20/month), automatically applied with no enrollment required.

- • No preset spending limit with Pay Over Time flexibility, allowing some balances to be carried while others must be paid in full each cycle.

- • Membership Rewards points transferable to 20+ airline and hotel partners including Delta, British Airways, Marriott Bonvoy, and Hilton Honors.

The Amex Business Gold is the right card for businesses spending $5,000 to $12,500 per month in concentrated categories like digital advertising, restaurant/catering, or shipping, where the 4x rate and strategic point redemptions easily justify the $375 fee. Businesses with more diversified or lower monthly spend will struggle to offset the annual fee and should look at no-fee alternatives or the Chase Ink cards.

American Express Business Platinum

The American Express Business Platinum Card is one of the most premium corporate cards available, carrying an $895 annual fee and offering more than $3,500 in annual credits and travel value when fully utilized. Cardholders earn 5x Membership Rewards points on flights and prepaid hotels booked through Amex Travel, 2x on eligible purchases of $5,000 or more, and 1.5x on purchases in select business categories up to $2 million per year. Notable credits include up to $200 in airline fee credits, $200 for Dell Technologies purchases, $360 in Indeed credits ($90/quarter), $150 Adobe credit (after $600 annual spend), $120 in wireless credits ($10/month), and access to 1,550+ airport lounges worldwide through the Global Lounge Collection including Centurion Lounges.

- • Global Lounge Collection access including Centurion Lounges, Priority Pass Select (enrollment required), Delta Sky Club (10 visits), and 1,550+ lounges across 140 countries.

- • 5x Membership Rewards points on flights and prepaid hotels booked through amextravel.com, making it best for heavy air travelers.

- • Up to $200 Dell Technologies statement credit per calendar year (up to $150 on first eligible purchases, plus up to $1,000 more after $5,000 in Dell spend).

- • $360/year in Indeed credits, $150 Adobe credit, and $120 annual wireless credit reduce the effective annual fee for qualifying businesses.

- • 35% points rebate when using Pay with Points for eligible first or business class flights or economy on the selected airline, effectively increasing point value.

The Amex Business Platinum is worth its premium price only for businesses with executives who travel frequently for work and can utilize the lounge access, airline credits, and technology/software credits. For the majority of small businesses or those without heavy travel, the effective cost is too high and the everyday rewards rate too low to justify the $895 outlay.

Capital One Spark

Capital One offers a full suite of Spark business cards from $0 annual fee options to premium charge cards. The flagship Spark Cash Plus is a charge card with a $150 annual fee (refunded each year you spend $150,000+), unlimited 2% cash back on all purchases, and 5% on hotels and rental cars through Capital One Business Travel. It has no preset spending limit and must be paid in full monthly. The Spark Cash Select has a $0 annual fee with 1.5% cash back. The Venture X Business charges $395/year and offers 150,000-mile sign-up bonus, a $300 annual travel credit, 10x miles on hotels and rental cars through Capital One Business Travel, and lounge access at 1,300+ airports. All Spark cards issue free employee cards and have no foreign transaction fees.

- • Spark Cash Plus delivers unlimited 2% back on all purchases with no categories to track, plus a $2,000 bonus for spending $30,000 in the first 3 months.

- • Venture X Business includes 10,000 bonus miles on each account anniversary and a $300 annual travel credit for bookings through Capital One Business Travel.

- • Free employee and virtual cards included on all Spark cards with customizable individual spending limits and real-time transaction alerts.

- • Capital One Business Travel portal included with Venture X Business for managing itineraries, earning elevated rewards, and accessing 1,300+ airport lounges.

- • No foreign transaction fees on all Spark cards, making them functional for international business travel and vendor payments.

Capital One Spark cards hit the sweet spot for businesses that want simple, predictable cash back without managing bonus categories. The Spark Cash Select is the best no-fee option; Spark Cash Plus suits high-spend businesses that can recoup the annual fee with $150,000 in spending. Businesses prioritizing travel rewards and lounge access should evaluate Venture X Business against the Amex Business Platinum and Chase Ink Preferred before committing.

Brex

Brex is a corporate charge card and spend management platform built for funded startups, tech companies, and scaling businesses. It does not require a personal credit check or personal guarantee; instead, approval is based on the company's cash balance, revenue, and funding status. Businesses must maintain at least $50,000 in cash reserves to qualify. The card has no annual fee and earns category-based rewards up to 7x on rideshare, 4x on travel booked through Brex Travel, 3x on restaurants, 2x on recurring software, and 1x on everything else. In January 2026, Capital One announced a $5.15 billion acquisition of Brex with the deal expected to close by mid-2026; Brex continues to operate independently through that period.

- • No personal guarantee underwriting: credit limits are based on the company's cash balance and revenue rather than the founder's personal credit score.

- • 7x points on rideshare and 4x on Brex Travel bookings, among the highest category reward rates available on any corporate card.

- • Built-in expense management with automated receipt matching, real-time categorization, and spend controls enforced at the card level for each employee.

- • Cards issued in 50+ countries with local currency support, making it practical for distributed teams and international operations.

- • Integrations with QuickBooks, Xero, NetSuite, Concur, Expensify, Gusto, and Rippling for automated expense reporting and accounting sync.

Brex remains the top choice for VC-backed startups and high-growth tech companies that want high credit limits, strong category rewards, and no personal liability. The Capital One acquisition announced in January 2026 introduces meaningful uncertainty about Brex's future product roadmap, and businesses evaluating Brex now should factor this into their decision and consider Ramp as a comparable independent alternative.

Ramp

Ramp is a corporate charge card and finance automation platform founded in 2019 that now serves over 25,000 businesses. It earns up to 1.5% cash back on all purchases with no annual fee, no foreign transaction fees, no personal guarantee, and no personal credit check. Eligibility requires at least $25,000 in a U.S. business bank account and the company must be a corporation, LLC, or LP. The core card and expense management platform is free; Ramp Plus at $15/user/month adds NetSuite and Sage Intacct integrations and advanced automation. As of June 2026, Ramp is introducing per-transaction fees for ACH and check payments through its Bill Pay feature ($0.59 per ACH, $1.99 per check), with a grace period for customers active before May 2026.

- • Flat 1-1.5% cash back on every purchase with no categories, no caps, and no complex point system, automatically credited to your Ramp account.

- • AI-powered expense policy enforcement that flags out-of-policy purchases in real time and routes them for approval before payment is made.

- • Automated receipt matching via SMS and Slack, reducing the time employees spend submitting expenses to under a minute per transaction.

- • Duplicate subscription detection that surfaces overlapping SaaS tools and vendor contracts to identify spending that can be cut or consolidated.

- • Native integrations with QuickBooks, Xero, Sage, NetSuite, and 100+ other platforms for automated GL coding and accounting sync.

Ramp is the best corporate card for incorporated businesses that prioritize automated expense management, cost reduction, and accounting efficiency over rewards maximization. It is particularly well-suited for companies using QuickBooks, Xero, or Sage, where the native integrations eliminate hours of monthly reconciliation. Teams seeking higher reward rates or access before accumulating $25,000 in the bank should look at Brex or Mercury IO.

BILL Divvy

The BILL Divvy Corporate Card (formerly Divvy, acquired by BILL.com in 2021 and rebranded in 2023) is a corporate charge card paired with BILL's free expense management software. Credit lines range from $1,000 to $5 million based on revenue, cash flow, and business history. The card has no annual fee and earns up to 7x points at restaurants and up to 5x at hotels, but rewards rates depend on how frequently the business pays its balance: weekly payments unlock the highest multipliers, while monthly payments earn just 1-2x. To earn any rewards, businesses must spend at least 30% of their credit limit in a given month. Points cannot be redeemed until after the first 12 months of card use.

- • Up to 7x points on restaurants and 5x on hotels when paying the balance weekly, among the highest category reward rates available on any no-fee corporate card.

- • Proactive spend controls that automatically decline purchases exceeding a cardholder's assigned budget, preventing overspend before it happens.

- • Real-time transaction visibility across all employee cards with instant budget adjustments and one-click card locking directly from the BILL Spend & Expense dashboard.

- • Credit lines up to $5 million with underwriting based on business revenue and cash flow rather than personal credit, accessible to businesses building their credit profile.

- • Physical and virtual cards for every employee at no extra cost, plus integration with QuickBooks Online for automated expense categorization and reporting.

BILL Divvy is a strong choice for businesses that can commit to weekly balance payments and consistently spend at least 30% of their credit line each month, particularly those with heavy restaurant and hotel spend. Businesses with variable monthly spending or that need immediate access to rewards should choose a simpler alternative like Ramp or Chase Ink Business Cash.

Airbase by Paylocity

Airbase was acquired by Paylocity in October 2024 for approximately $325 million and now operates as Airbase by Paylocity (also branded as Paylocity for Finance). The platform combines bill pay and accounts payable automation, expense management, corporate cards, and procurement in one spend management suite. Its corporate cards support physical and virtual cards with pre-built spend controls and approval workflows. The key differentiator is deep integration with Paylocity's HCM platform, allowing companies to manage both payroll and non-payroll spend from a single system. Airbase targets companies between 100 and 5,000 employees and integrates with Oracle NetSuite, Sage Intacct, and QuickBooks.

- • Unified AP automation covering purchase orders, invoice processing, and payment routing via ACH, virtual card, check, or wire from a single platform.

- • Smart corporate cards with pre-built approval workflows that enforce spending policies before purchases are made, not after the statement arrives.

- • Real-time employee reimbursements initiated directly through the platform, eliminating the typical 1-2 week delay common with traditional expense reimbursement processes.

- • Paylocity HCM integration allows payroll and non-payroll spend to be managed side-by-side, giving finance and HR teams a unified view of all company spend.

- • Deep ERP integrations with Oracle NetSuite, Sage Intacct, QuickBooks, and others for automated GL coding and financial reporting.

Airbase by Paylocity is the best option for mid-market companies already using Paylocity for HR and payroll who want to consolidate their entire spend stack into a single vendor. Businesses not using Paylocity or those outside the 100-5,000 employee range will get better value and less complexity from Ramp, Payhawk, or BILL Divvy.

Stripe Corporate Card

The Stripe Corporate Card is a Visa charge card available exclusively to businesses with an existing Stripe account. There is no annual fee, no foreign transaction fees, no late fees, and no card replacement fees. Credit limits are determined by the business's Stripe payment processing history and banking relationships rather than traditional credit checks. The card earns cash back with enhanced rates in the categories where a business spends most, automatically applied as a monthly statement credit without manual redemption. Physical and virtual cards can be provisioned instantly from the Stripe Dashboard, with built-in spending controls by employee, day, or category.

- • Instant virtual card provisioning directly from the Stripe Dashboard, with no paperwork or application process beyond existing Stripe account verification.

- • Automatic cash back in the highest spending categories with no manual redemption required, credited directly to the monthly statement.

- • Real-time expense reporting visible in the Stripe Dashboard alongside payment processing data, giving a unified financial view for internet businesses.

- • Spending controls configurable by amount per person, per day, or per category, with immediate card locking and transaction blocking from the Dashboard.

- • Integrates natively with QuickBooks and Expensify for automated expense categorization and reconciliation.

The Stripe Corporate Card is a sensible default for Stripe-native businesses, particularly e-commerce companies and SaaS platforms already deeply embedded in the Stripe ecosystem. For businesses that want transparent, published rewards and no personal guarantee, Ramp and Mercury IO are stronger alternatives with no platform lock-in.

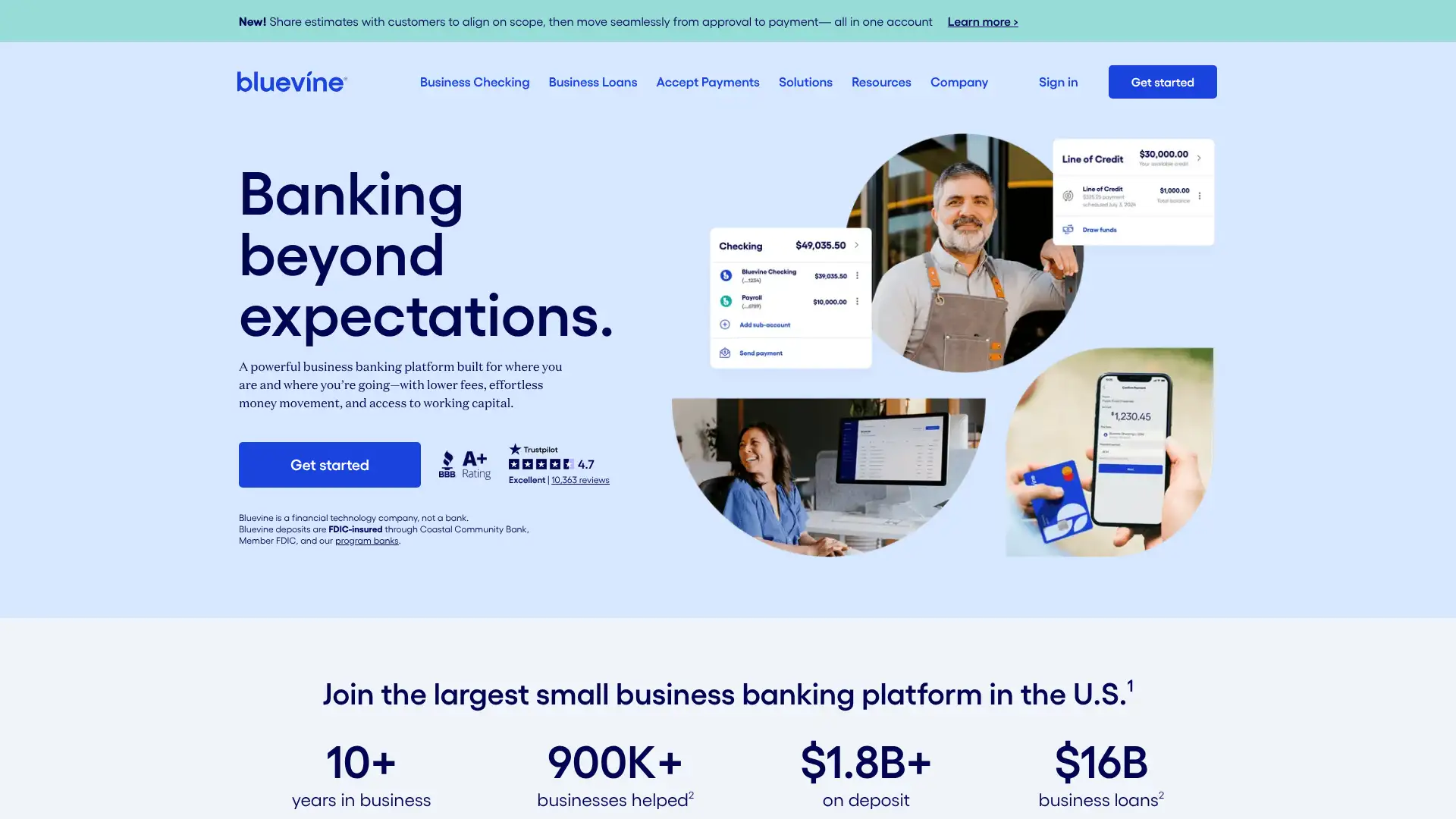

Bluevine Business Cashback Mastercard

Bluevine launched the Business Cashback Mastercard in general availability in June 2024, exclusively for eligible Bluevine Business Checking customers. It earns unlimited 1.5% cash back on all business purchases with no annual fee, and is issued by Coastal Community Bank. The card integrates directly with the Bluevine Business Checking dashboard so owners can view credit card and checking transactions in one place. Cash back earned can contribute toward meeting the monthly spending requirements to earn APY on Bluevine checking balances (2.0% on Standard, higher on Plus and Premier plans). The card is currently available by invitation only to customers who meet eligibility criteria including time in business and account standing.

- • Unlimited 1.5% cash back on all business purchases with no categories, caps, or rotating periods, credited automatically.

- • Integrated dashboard showing both Bluevine Business Checking and credit card transactions in one view, reducing the need to toggle between platforms.

- • Employee cards with customizable spending limits, real-time transaction visibility, and instant card locking available for all team members.

- • Card spend counts toward the monthly activity requirement to earn APY on Bluevine Business Checking balances, adding value for businesses using both products.

- • Mastercard perks including ID theft protection, car rental insurance, and discounts on QuickBooks, Intuit, and McAfee products.

The Bluevine Business Cashback Mastercard is a solid choice for small businesses already banking with Bluevine who want a simple no-fee cashback card that integrates with their checking account. It is not a fit for businesses that need expense controls, multi-team card management, or ERP integrations, and the invitation-only access limits its availability to a subset of Bluevine customers.

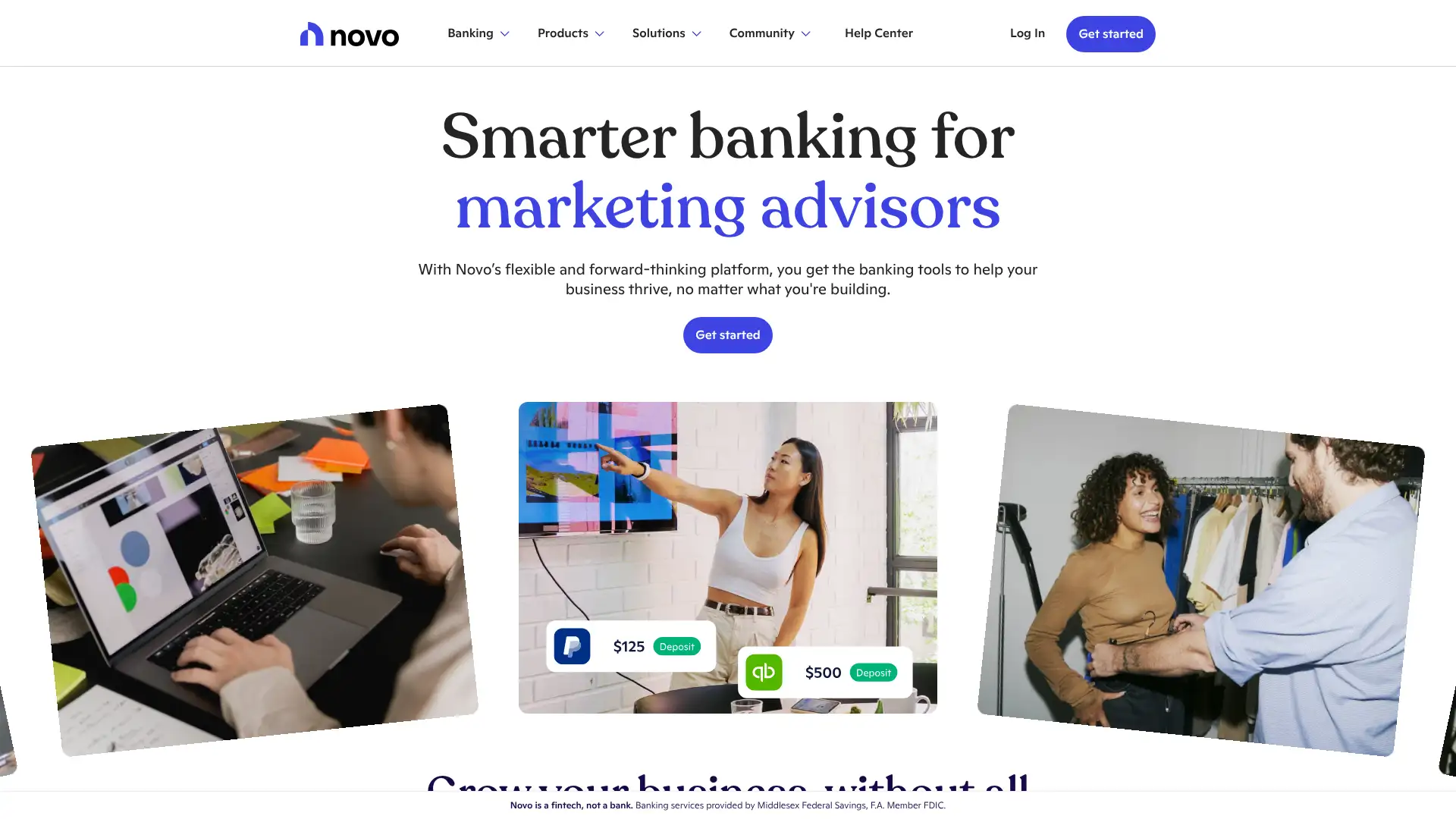

Novo Business Credit Card

Novo launched the Novo Business Credit Card for its over 250,000+ banking customers, issued by Continental Bank via Mastercard. The card earns 2% cash back on eligible purchases when the Novo checking account balance is $5,000 or more, and 1% when the balance is under $5,000. There is no annual fee. Novo positions the card as a way for small businesses to build business credit while integrating their spending with Novo's checking account, expense categorization, and bookkeeping tools. Perks include Mastercard Easy Savings, QuickBooks discounts, Microsoft Advertising credits, and Instacart Business offers for new subscribers.

- • Tiered 2%/1% cash back structure tied to the Novo checking account balance, incentivizing businesses to maintain healthy cash reserves alongside their credit card spending.

- • AI-powered expense categorization built into the Novo dashboard, automatically sorting transactions for tax readiness and financial reporting.

- • Business credit reporting to major bureaus, helping small businesses establish a formal credit profile through consistent on-time payments.

- • Integration with Novo's invoicing and bookkeeping tools, allowing owners to view credit and debit transactions alongside sent invoices in one interface.

- • Mastercard network perks including Instacart Business offers, QuickBooks Online discounts, Zoho and Microsoft Advertising credits for new customers.

The Novo Business Credit Card suits sole proprietors and very small businesses that already use Novo for banking and want simple, auto-categorized cashback without the complexity of a full expense management platform. Businesses with employees, team spending needs, or balances consistently below $5,000 will find stronger options in Ramp or BILL Divvy.

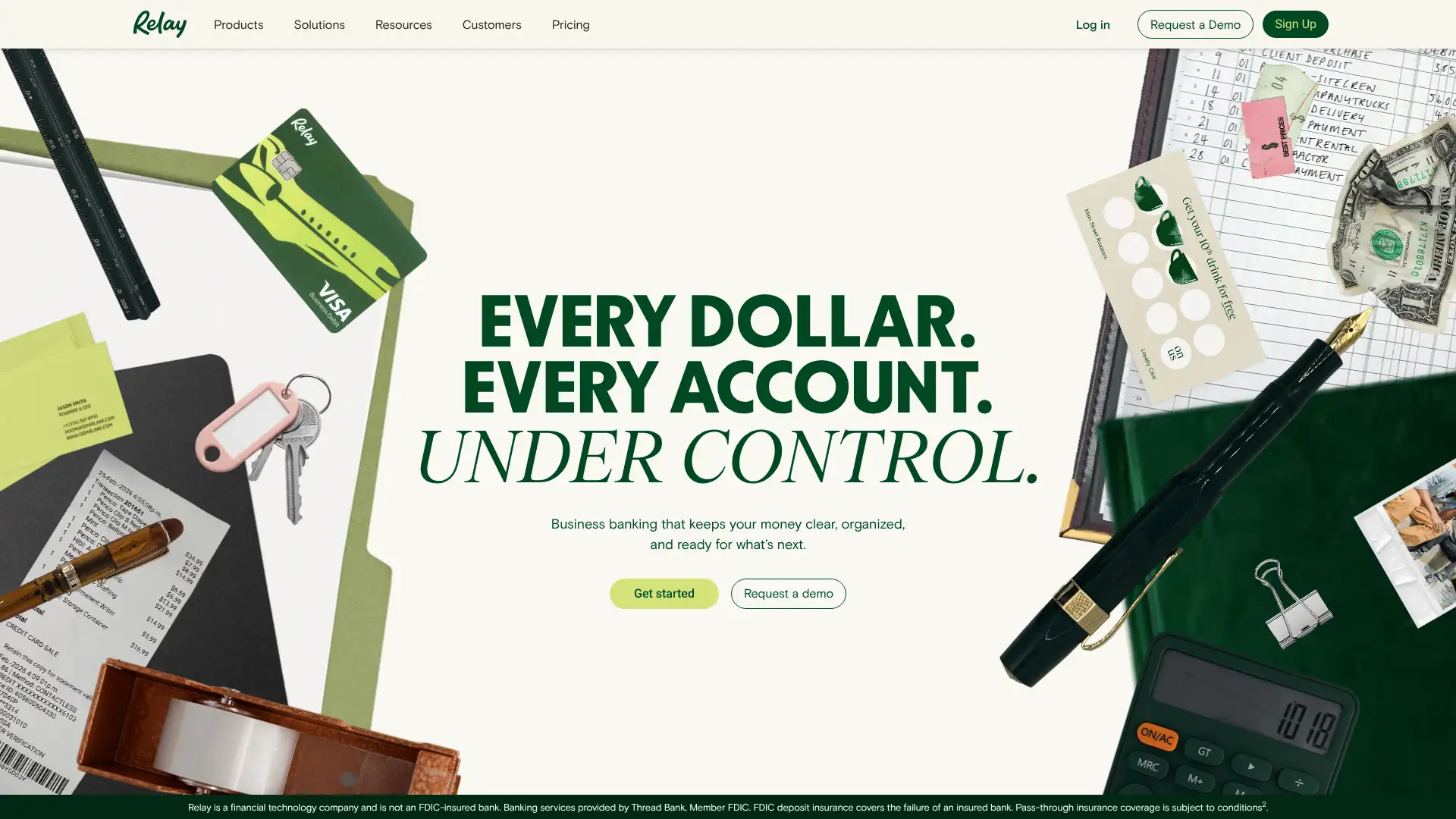

Relay

Relay is an online banking platform for small businesses that added the Relay Visa Credit Card as an invitation-only product, issued by Thread Bank. The card earns up to 1.5% cash back on all eligible purchases, with the exact rate tied to the Relay subscription plan (Starter, Grow at $30/month, or Scale at $120/month). It is a charge card with a 30-day billing cycle, paid automatically from a linked Relay account. Credit limits are set based on either a cash-based model (requiring $25,000 in Relay accounts) or an underwriting model based on revenue and financial health. As of March 2026, Relay expanded access to include businesses with $50,000+ in average monthly revenue over 3 months, removing the balance-only requirement for qualifying businesses.

- • Up to 50 unique virtual and physical credit cards per business with 30+ customizable color and spend-category designs to visually organize expenses by purpose.

- • Per-card spending limits and category restrictions enforced at the point of transaction, preventing employees from spending in unauthorized categories without manager approval.

- • Business credit building through payment reporting to all three major business credit bureaus, announced in March 2026.

- • Full banking integration with up to 20 Relay checking accounts and up to $3 million in FDIC-insured sweep coverage through Thread Bank.

- • QuickBooks and Xero sync with automated expense categorization, receipt upload, and role-based permissions for bookkeepers and accountants.

Relay is the best banking-integrated credit card option for small businesses using a multi-account cash management approach like Profit First, or accountants managing multiple client accounts. The invitation-only model and $25,000 balance requirement limit accessibility, and Thread Bank's FDIC consent order is worth monitoring. Businesses that prioritize straightforward cashback over multi-account banking should evaluate Mercury IO or Bluevine.

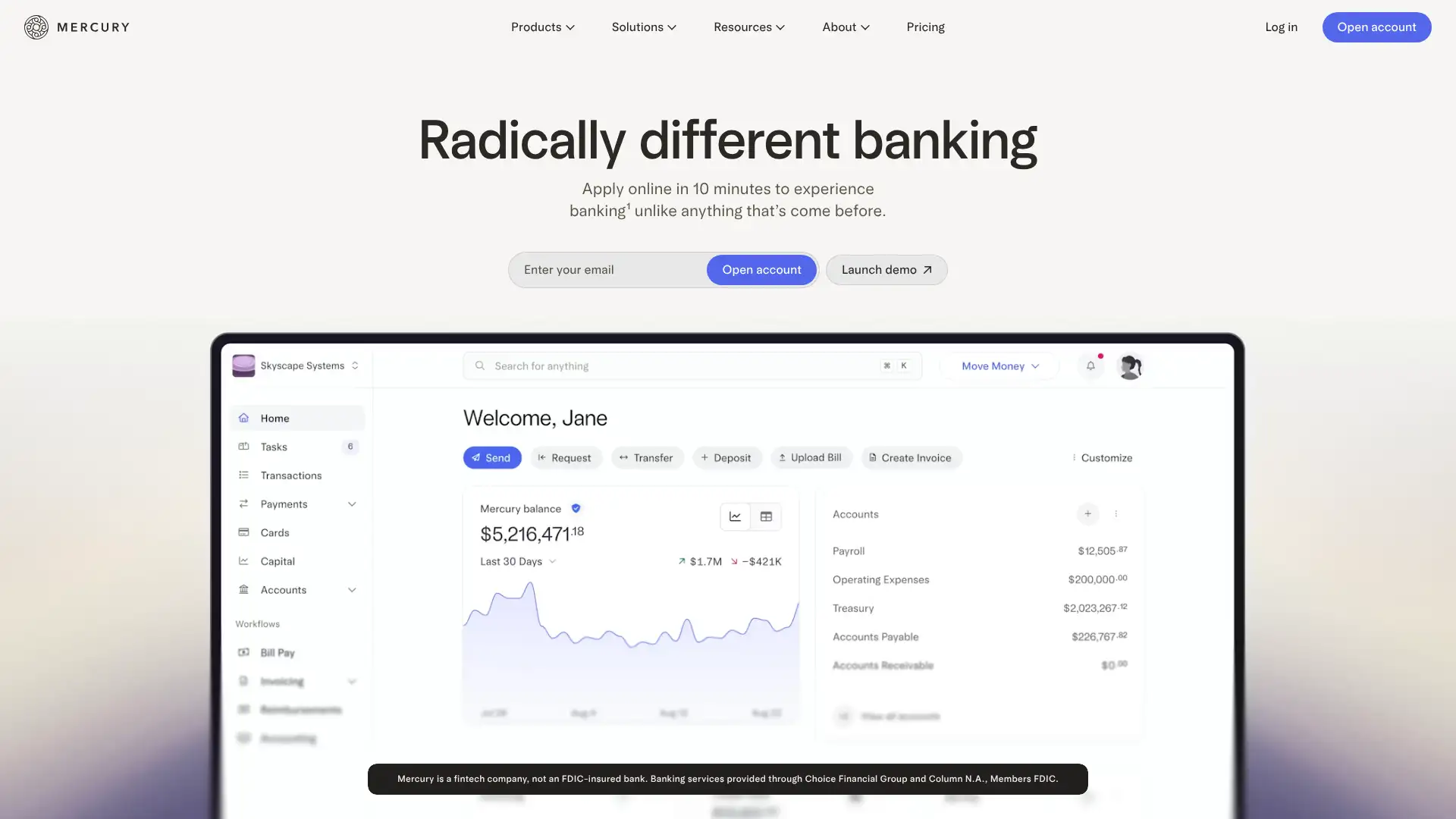

Mercury IO

Mercury launched the IO Corporate Card in 2022, issued by Patriot Bank via Mastercard, as part of its banking platform used by more than 80,000 startups. The IO card earns a flat 1.5% cash back on all settled purchases, including international transactions, with no annual fee, no personal guarantee, and no personal credit check. The card is underwritten based on the company's Mercury account balance. Most businesses qualify for an introductory IO account on day one of opening a Mercury account. Monthly payment schedules become available once the business holds $15,000 in Mercury accounts; before that, daily repayment applies. A foreign transaction fee applies for non-USD purchases.

- • Flat 1.5% cash back on every purchase automatically deposited into the linked Mercury account when the balance is paid, with no manual redemption.

- • Cash-underwritten credit limits that scale as the company's Mercury account balances grow, enabling higher limits for companies that hold more capital.

- • Unlimited virtual cards with individual monthly limits for team members, plus one physical card per employee for in-person purchases.

- • External bank account linking to supplement credit limits beyond the Mercury balance, added in October 2025 to increase spending power for early-stage companies.

- • Automatic payment from the linked Mercury account monthly or daily, with cashback deposited in proportion to the amount paid.

Mercury IO is the best card for early-stage startups that want a banking-integrated charge card with flat cashback from day one without the $50,000 reserve barrier that Brex requires. Founders who prefer simplicity over complex rewards and want their banking and spending on one dashboard will find Mercury IO a natural fit. Companies that need advanced expense management, multi-entity controls, or zero foreign transaction fees should consider Brex or Ramp.

Wallester Business

Wallester is an Estonian-licensed financial institution and Visa Principal Member founded in 2018, ranked the fastest-growing fintech in Europe in the Financial Times FT1000 2026 list. Wallester Business offers a free-forever plan with up to 300 virtual Visa cards and unlimited physical cards, linked to a personal IBAN account in EUR, without requiring a monthly subscription. The free plan includes spend management, budget controls, receipt capture, and mobile app access. Paid plans starting at EUR 199/month expand the card count and unlock accounting integrations and advanced reporting. Wallester is primarily used by advertising agencies, media buyers, e-commerce companies, and SaaS teams that need large volumes of virtual cards to separate spending by campaign or vendor.

- • Up to 300 free virtual Visa cards on the free plan, more than any other platform in its category, ideal for teams managing multiple ad campaigns or vendors.

- • Personal IBAN account in EUR for each Wallester Business account, enabling direct bank transfers and payroll functionality within the European Economic Area.

- • Multi-currency support with 11 currencies available; non-EUR top-ups incur a EUR 15 fee per deposit, relevant for businesses operating in mixed currencies.

- • Real-time transaction monitoring and receipt capture via the Wallester mobile app for iOS and Android, with automated matching to expense categories.

- • REST API for custom integrations and white-label card programs, used by software platforms and fintechs looking to embed card issuance in their products.

Wallester Business is the best option for European companies — particularly media buying agencies and e-commerce teams — that need a large number of virtual Visa cards without a monthly subscription fee. Businesses outside the EEA or those needing credit facilities rather than prepaid accounts should look at Pliant, Pleo, or Payhawk for more comprehensive solutions.

Jeeves

Jeeves is a global spend management platform founded in 2019 and backed by $543 million in funding from Andreessen Horowitz, GIC, and Tencent, with a $2.1 billion valuation from its March 2022 round. It serves more than 3,000 businesses across 30+ countries including Mexico, Colombia, Brazil, the U.S., Canada, the UK, and the EU. Jeeves offers corporate cards (physical and virtual) issued in local currencies, cross-border payments to 150+ countries in 40 currencies, and expense management software at no additional cost. Cards earn up to 1% cash back and provide access to 1,300+ airport lounges worldwide. There are no monthly fees, no annual fees, and no personal guarantees required.

- • Cards issued in local currencies across 30+ markets, allowing teams in Mexico, Colombia, Brazil, the EU, UK, and the U.S. to spend in their local currency without conversion overhead.

- • Cross-border payment processing to 150+ countries in 40 currencies, with same-day settlement available between North America, South America, and Europe.

- • Up to 1% cash back on all card purchases plus access to 1,300+ airport lounges globally, a premium perk typically reserved for higher-fee cards.

- • Expense management software included at no extra cost with receipt capture via mobile app, approval workflows, and integrations with QuickBooks and Xero.

- • 37-day payment terms on invoice-based credit in select regions, extending cash flow flexibility beyond the standard 30-day charge card cycle.

Jeeves is the best corporate card option for startups and SMBs operating across Latin America and Europe that need local currency cards, cross-border payments, and expense management in one platform without monthly fees. Businesses operating exclusively in the U.S. with no international team have better-supported alternatives in Brex, Ramp, or Mercury IO.

Pliant

Pliant is a Berlin-based fintech founded in 2020 that operates as a licensed EU e-money institution and Visa Principal Member. It issues Visa Platinum Business (physical black cards) and Visa Infinite Business (metal cards) credit cards for corporations, SMEs, and scale-ups across 30+ countries in 11 currencies. Unlike most European spend management tools that offer prepaid or debit cards, Pliant provides actual credit cards with high credit limits and flexible repayment terms, making it bank account-independent. The platform offers cashback on all transactions (rate varies by repayment frequency), is integrated with major ERP and accounting platforms, and supports transactions in 11 currencies. Pricing is custom and requires a sales contact.

- • True Visa credit cards (not prepaid or debit) with high credit limits and flexible repayment terms that do not require linking to a business bank account.

- • Visa Infinite Business metal card option with unlimited worldwide airport lounge access and a comprehensive travel insurance package for executives.

- • Multi-entity support allowing different branches or subsidiaries of the same company to have separate billing settings and card pools from one Pliant account.

- • Pro API for custom integrations with ERP systems, procurement platforms, and financial software for high-volume enterprise card programs.

- • 11-currency billing to reduce FX conversion costs for European businesses with cross-border operations or international vendor payments.

Pliant is the best Visa credit card option for European companies that have outgrown prepaid card platforms and need actual credit lines, multi-currency billing, and Visa Infinite Business features for executive travel. Businesses that need published pricing or U.S. operations should look at Payhawk or Jeeves for more transparent and geographically broader alternatives.

Payhawk

Payhawk is a Bulgarian-founded spend management platform serving finance teams in 32+ countries. It combines Visa corporate cards (debit and credit, virtual and physical including metal), expense management, invoice management, and accounts payable automation in a single platform. Payhawk is an EEA and UK EMI-licensed company and Visa Principal Member. Pricing starts at $599/month for cards and expenses or bill payments separately, and $899/month for the full Procure to Pay suite. An introductory plan is available for businesses with fewer than 20 employees at £149/month for 24 months. All plans include cashback on Visa card spend capped at the subscription cost, unlimited users, transactions, and receipt processing.

- • AI Office of the CFO suite including Financial Controller Agent, Travel Agent, Procurement Agent, and Payments Agent for automated workflow handling at the enterprise level.

- • Visa corporate cards issued across 32+ countries in 7 currencies with debit and credit options, providing flexibility for different business structures and cash flow preferences.

- • OCR receipt scanning in 60+ languages that auto-populates expense fields and routes for approval, reducing manual data entry to near zero for most transactions.

- • Native ERP integrations with NetSuite, Xero, QuickBooks, Sage Intacct, Microsoft Dynamics 365, and DATEV for real-time accounting sync without manual uploads.

- • Multi-entity management allowing finance teams to oversee spending across multiple legal entities with separate billing and consolidated reporting from one dashboard.

Payhawk is the most capable all-in-one spend platform for mid-market European companies with 50-500 employees that need corporate cards, AP automation, and procurement in one integrated stack. For smaller teams or businesses that only need card management and basic expense tracking, the $599/month starting price is hard to justify relative to Pleo or Spendesk.

Spendesk

Spendesk is a Paris-based spend management and procurement platform that was the first European platform to fully integrate procurement and spend management. It processes EUR 20 billion annually across 200,000+ business users. The platform combines corporate cards, accounts payable, expense management, budgets, and procurement in one suite. Its AI automation handles receipt validation, invoice processing, and spend allocation with approval workflows. Spendesk offers physical and virtual Mastercard corporate cards, single-use virtual cards for online purchases, and Apple/Google Pay support. Pricing has three tiers: Foundations, Scale, and a bespoke Enterprise plan, all with custom pricing requiring a sales demo.

- • AI-powered receipt validation that automatically reads, categorizes, and routes receipts for approval, with reviewers noting it eliminates up to 80% of manual data entry.

- • Single-use virtual cards for one-time online purchases, reducing the risk of subscription creep and vendor fraud by making each virtual card number unique per transaction.

- • Integrated procurement module with purchase orders, supplier management, contract renewal tracking, and approval workflows in one platform.

- • Pre-accounting automation that extracts VAT, allocates expense accounts, and prepares data for export, significantly reducing month-end closing time.

- • ISO 27001: 2022 certified and PCI-DSS, GDPR, and PSD2/SCA compliant, meeting the strictest European security and regulatory standards.

Spendesk is the strongest choice for European companies with 50 to 1,000 employees that want a fully integrated procurement and spend management platform backed by AI automation. Its lack of published pricing is a genuine friction point, and businesses that want to evaluate costs before engaging sales should contact Pleo or Payhawk first as benchmark comparisons.

Pleo

Pleo is Europe's leading prepaid spend management solution, serving over 40,000 customers across 14 European countries including the UK, Denmark, Germany, Sweden, France, Spain, and others. It issues Mastercard prepaid cards (physical and virtual) linked to a prefunded company wallet, with automatic receipt nudging, OCR scanning, and accounting integrations with Xero, Sage, QuickBooks, and 50+ others. Pleo's free Starter plan is available for small teams; paid plans start at approximately £9.50 per user per month for Essentials and scale to £179 for Beyond plans with cashback. As of 2026, Pleo introduced vendor cards for recurring supplier payments and expanded its invoice management module for larger teams.

- • Automatic receipt nudging that sends push notifications to employees immediately after every purchase, achieving near-100% receipt submission rates reported by many users.

- • Vendor cards for recurring subscriptions issued with unique card numbers per supplier, making it easier to track, control, and cancel specific vendor payments.

- • Prepaid Mastercard model that requires no credit check and removes the financial risk of employee overspend by limiting each card to its assigned wallet balance.

- • In-app expense submission via iOS and Android with OCR auto-population of amount, vendor, and category, reducing submission time to under 30 seconds.

- • 50+ accounting integrations including one-click export to Xero, QuickBooks, and Sage, with real-time or end-of-period sync options.

Pleo is the best entry-level spend management card for small and mid-sized European teams that prioritize ease of use, strong receipt automation, and a trusted brand. The free plan works for very small teams; scaling to paid tiers is straightforward. Businesses that need credit facilities rather than prepaid, or those with complex procurement workflows, should evaluate Pliant or Payhawk.

Soldo

Soldo is a UK-headquartered spend management company founded in 2016 and serving over 30,000 companies across Europe. It issues prepaid Mastercard debit cards and provides a spend management platform that works alongside existing business bank accounts rather than replacing them. Soldo's model relies on businesses depositing funds into wallets that are then distributed to individual or team cards with custom spending rules. Plans include Standard, Plus, and Unlimited, with no free plan but a 30-day trial on Standard and Plus. The Standard plan covers core receipt capture, user wallets, reporting, and integrations; Plus adds multi-currency wallets and advanced reporting; Unlimited is designed for enterprises.

- • Multi-wallet architecture allowing finance teams to ring-fence funds for specific teams, departments, or projects with custom spending limits and rules per wallet.

- • Physical and virtual prepaid Mastercards including fuel cards for fleets, with 1% FX fee for transactions in currencies other than the card's issued currency.

- • Receipt capture and automatic matching via the Soldo mobile app, with direct sync to QuickBooks Online, Xero, NetSuite, and Sage for accounting reconciliation.

- • Real-time reporting dashboards showing company-wide spend by wallet, card, group, and fuel category, exportable to Excel, PDF, and CSV formats.

- • Segregated client funds model where deposited money is held in a regulated, ring-fenced account separate from Soldo's operating capital, providing additional financial security.

Soldo is a solid choice for European businesses, charities, and nonprofits that need wallet-based spending control without a credit facility and want to keep their existing business bank account. For businesses that have already evaluated Pleo and want a more enterprise-grade multi-wallet structure, Soldo offers meaningful differentiation. Teams that need credit-based spending or lower FX fees should consider Payhawk or Pliant.

Emburse Cards

Emburse is a Los Angeles-based fintech company offering two main products: Emburse Cards (prepaid corporate cards with built-in spend controls) and Emburse Spend (an expense management platform starting at $8/user/month that works with any existing corporate card including Amex virtual cards). Emburse Cards are prepaid Mastercards issued with granular self-enforcing spending rules by budget, date, time, location, or transaction category. The platform integrates with Sage Intacct, QuickBooks Online, NetSuite, Okta, and Xero. Emburse Cards have no annual fee with custom pricing; Emburse Spend starts at $8/user/month with a 30-day free trial.

- • Granular prepaid spending rules that self-enforce at the point of purchase, automatically declining transactions that exceed budget, date, time, location, or category limits.

- • Emburse Spend platform allows businesses to keep their existing credit card program (including Amex, Visa, and Mastercard) while adding real-time expense submission and approval workflows.

- • Automatic Google inbox scanning to locate and match receipts to card transactions, reducing the need for employees to manually upload receipts.

- • 1% cash rebate available on Emburse Cards when qualifying spend volumes are met, confirmed on the pricing page.

- • Direct integrations with Sage Intacct, QuickBooks Online Advanced, NetSuite, Xero, Okta, and Slack for approval workflows and accounting automation.

Emburse is the best choice for U.S. businesses that want granular prepaid spending controls but do not want to abandon their existing corporate card program. Emburse Spend is particularly well-suited for companies that have an established Amex or Chase card relationship but need real-time expense submission and approval workflows layered on top. For businesses without an existing card program, Ramp offers comparable controls for free.

Center

Center is a Seattle-based spend management company that puts the CenterCard Mastercard at the center of its expense and travel management platform. Unlike software-first platforms, Center is designed around the card itself, capturing spend data at the point of purchase and automatically matching it to projects, jobs, and cost categories in real time. The platform is built for mid-market companies with 50-500 employees, with particular traction in professional services and construction where job-cost coding is critical. Center's revenue model is interchange-based, meaning the platform is funded by Mastercard transaction fees rather than subscriptions, allowing Center to offer the card at a usage-based cost rather than flat subscription pricing.

- • Real-time spend capture at the point of purchase with automatic job-code, project, and department coding visible to finance teams before month-end, not after.

- • Smart Receipts that auto-generate IRS-compliant line-item receipts for up to 40% of transactions, reducing the manual receipt collection burden significantly.

- • Integrated corporate travel booking for flights, hotels, and rental cars directly within the CenterCard mobile app, keeping all travel spend within the same tracking system.

- • AI-powered expense audit that flags only exceptions requiring review, rather than requiring finance teams to manually review all transactions.

- • Filterability by project, job, and employee category for professional services and construction use cases, enabling real-time billable expense tracking.

Center is the strongest choice for professional services firms, consultancies, and construction companies that need real-time job-cost tracking tied directly to corporate card transactions. The interchange-based model and card-centric design make it genuinely different from software-first competitors. Businesses without job-cost tracking needs will find the platform's specialization a limitation rather than a benefit.

Navan

Navan (formerly TripActions) is an all-in-one corporate travel and expense platform serving 10,000+ customers including DoorDash, WeWork, and Zillow. It combines a corporate card, travel booking (flights, hotels, cars, trains), expense management, and AP automation. The Navan corporate card earns up to 1.5% cash back on all transactions with no annual card fee and is issued in USD, GBP, and EUR. Navan Travel is free for companies with up to 300 employees with no per-booking fee; Navan Expense costs $15/user/month for the first 5 active users, then $15/user/month beyond. Navan Rewards incentivizes employees to book cost-effective options by giving them points redeemable for personal travel or gift cards.

- • Fully integrated travel booking, corporate card, and expense management in a single platform, eliminating the need for separate TMC, card, and expense software vendors.

- • Navan Rewards program that pays employees personal travel credits or gift cards when they book below the policy budget, aligning individual and company incentives.

- • Virtual cards automatically generated for each travel booking made through Navan, so travelers never need to front personal expenses for business trips.

- • Real-time policy enforcement that blocks out-of-policy bookings and flags non-compliant expenses before approval, reducing the CFO's month-end surprises.

- • Global reimbursements in 25+ currencies across 49 countries, supporting distributed teams and contractors outside the primary business entity.

Navan is the best choice for companies with 20-300 employees that have meaningful corporate travel spend and want to eliminate the chaos of separate booking, card, and expense platforms. The free travel tier and $15/user expense add-on make it cost-competitive for mid-sized companies. Businesses with limited travel but heavy expense reporting volume should evaluate Ramp or BILL Divvy instead.

Corpay

Corpay (NYSE: CPAY, formerly FLEETCOR) is America's largest commercial card issuer and a S&P 500 company that serves 800,000 businesses in 200+ countries. Corpay offers corporate travel cards, purchasing cards (P-cards), virtual cards for AP automation, and fleet fuel cards under brands including Corpay One and Corpay Complete. Its Mastercard products are issued by Regions Bank and Fifth Third Bank. Corpay Complete is the flagship all-in-one platform combining AP automation, corporate card management, and expense control. Pricing is custom and requires a demo. The company also offers cross-border payment services and has acquired multiple fleet card brands including Fuelman and others.

- • Virtual single-use and recurring card numbers for AP automation that bind to a specific vendor, invoice amount, and expiry date, sharply reducing AP fraud exposure.

- • Corpay Complete's fully managed AP automation handles purchase orders, invoicing, vendor payments, corporate cards, and expense controls from one platform.

- • Rebate programs tied to card spend volume, with higher spend unlocking better cash-back rebate rates for enterprise clients.

- • Corporate travel card specifically designed for executive travel with enhanced rebate opportunities, travel protections, and dedicated account support.

- • 100+ ERP integrations including NetSuite, Sage, QuickBooks, and Microsoft Dynamics, with automated GL coding and real-time accounting sync.

Corpay is the right fit for large enterprises and corporate AP teams that need the scale, global reach, and managed supplier enrollment that only an S&P 500 commercial card issuer can reliably deliver. For companies under 500 employees, the combination of custom pricing, legacy UX, and high late fees makes Ramp, Navan, or BILL a more practical and modern alternative.

WEX

WEX Inc. (NYSE: WEX) is a Portland, Maine-based global commerce platform founded in 1983 as Wright Express Corporation that serves 600,000+ businesses with fleet fuel cards, EV charging management, and B2B payment solutions. The WEX Fleet Card is accepted at 95% of U.S. fueling stations, saving businesses up to 15 cents per gallon through the WEX EDGE savings network. In January 2026, WEX introduced the first fleet card unifying traditional fuel and public EV charging via embedded RFID technology, allowing mixed-energy fleets to manage all vehicle energy on one card, account, and invoice. WEX also offers the FlexCard variant that allows balances to be carried (with a 6.77% periodic interest rate, equating to approximately 83% APR).

- • Accepted at 95% of U.S. fuel stations plus 45,000+ vehicle service locations, providing more coverage than any proprietary trucking fuel card network.

- • WEX Fleet Card now with EV payment capabilities, the first card to unify traditional fuel and public EV charging (175,000+ accepting charge ports) on one card and invoice, launched January 2026.

- • WEX EDGE savings network offering up to 15 cents per gallon savings on fuel, plus discounts on tires, hotels, and wireless at the point of sale.

- • ClearView analytics platform providing fleet spending insights, MPG tracking, fuel consumption trends, and real-time exception alerting for fraud or unusual activity.

- • Fleet SmartHub mobile app (4.7 stars App Store as of Feb 2026) for real-time card management, fuel price finder, and transaction alerts from any device.

WEX is the strongest all-purpose fleet fuel card for businesses with mixed vehicle types, nationwide routes, and now mixed fuel/EV fleets following the January 2026 EV charging card launch. Trucking companies that route primarily through major truck stops will get stronger per-gallon discounts from Comdata or AtoB. Local service businesses with smaller fleets should evaluate Coast for its simpler $4/user pricing.

Comdata

Comdata has served the trucking industry for over 50 years and offers multiple card products for over-the-road fleets: the Fleet Card (credit line), Connect Card (prepaid), OnRoad Card (driver payroll plus fuel), and Mastercard (dual-network access). The Comdata network is accepted at 8,000+ truck stops including TA/Petro, Pilot/Flying J, and Love's, with discounts up to 40 cents per gallon off the cash price at network locations. The standout feature is the OnRoad Card, which combines fleet fuel discounts with instant driver payroll deposits when loads settle, eliminating the need for separate payroll and fuel card programs. Pricing is tiered with per-card monthly fees depending on the plan selected.

- • Up to 40 cents per gallon off the cash price at TA/Petro truck stops, up to 10 cents at Pilot/Flying J, and up to 8 cents at Love's, representing the strongest truck stop discount program in the industry.

- • OnRoad Card instant driver pay: when a load settles, funds hit the driver's card immediately via direct deposit, eliminating the 3-5 day ACH wait common with traditional payroll processing.

- • OneClick fraud prevention that requires drivers to unlock the fuel card via the Comdata app before fueling, with the card automatically relocking after the transaction.

- • DRIVEN app for drivers to find fuel discounts by location, manage peer-to-peer transfers between OnRoad cardholders, and track spending in real time.

- • IFTA fuel tax reporting built into the Comdata platform, simplifying quarterly state fuel tax filings for owner-operators and carriers.

Comdata is the best fleet card for established OTR trucking companies that route heavily through TA/Petro, Pilot, and Love's and want the strongest per-gallon discounts bundled with driver payroll capabilities. Fleets outside the OTR trucking sector, or those needing fuel access beyond truck stops, will find WEX or Coast more practical for their operations.

Coast

Coast is a modern fintech fleet card founded for local service businesses (HVAC, plumbing, landscaping, construction, delivery) that need fleet fuel management without the complexity of OTR-focused cards. The Coast Card runs on the Visa fleet network, accepted everywhere Visa is accepted. It earns 3-9 cents per gallon at 30,000+ partner stations including Exxon, Mobil, Shell, Circle K, 7-Eleven, and Casey's, plus 1% cash back on all non-fuel purchases. The fee structure is transparent at $4 per active user per month with no setup, annual, or transaction fees. Coast's fraud guarantee covers up to $25,000 per year for both external and employee fuel card fraud. In 2025, Coast expanded to cover non-fuel fleet expenses including parts, tools, and job supplies, effectively becoming a full fleet expense card.

- • Accepted everywhere Visa is accepted, giving drivers the flexibility to fuel at any gas station without rerouting to specific brand networks.

- • 3-9 cents per gallon at 30,000+ partner stations (Exxon, Shell, Mobil, Circle K, BP, 7-Eleven, Casey's, RaceTrac, Maverik) plus 1% cash back on all non-fuel purchases including maintenance and supplies.

- • SMS card unlock security requiring drivers to text the card ID before fueling, combined with GPS auto-decline if the vehicle is not near the pump, providing two-factor transaction verification.

- • Included expense management platform at no extra cost covering fuel, maintenance, job supplies, and field purchases, with receipt capture via driver SMS for non-fuel transactions.

- • Telematics integrations with Samsara, Geotab, Verizon Connect, Azuga, and Fleetio for GPS-powered fraud prevention and cost-per-vehicle reporting.

Coast is the best fleet card for local service businesses (HVAC, plumbing, landscaping, delivery) with 2-50 vehicles that want simple, transparent pricing, wide Visa acceptance, and modern app-based fraud controls without committing to a trucking-focused card program. For long-haul trucking fleets that need deep diesel discounts at major truck stops, Comdata or WEX are more appropriate.

Mudflap

Mudflap launched in 2020 as a mobile app for independent truckers to find discounted diesel, and introduced the Mudflap Fuel Card (issued by Celtic Bank via Visa) in 2023. The card is used by over 515,000 drivers and offers discounts averaging 57 cents per gallon at 2,800+ in-network truck stops including regional chains like Kwik Trip and Road Ranger, with up to $1 per gallon savings at select locations. There are no monthly fees, no annual fees, no setup fees, and no transaction fees. The only fee is a late payment penalty of 3-6% depending on how overdue the balance is. Discount pricing is structured as cost-plus (wholesale rack price plus a small markup) rather than the retail-minus model used by WEX and Coast, often resulting in stronger absolute per-gallon savings.

- • Cost-plus pricing at 2,800+ in-network truck stops delivering average savings of 57 cents per gallon, significantly higher than the retail-minus discount model used by WEX and Comdata.

- • No monthly fees or annual fees of any kind, with charges only applying if a payment is late, making it the lowest-commitment fuel card available for trucking fleets.

- • Mudflap app with real-time price comparison across in-network locations, route optimization to the cheapest nearby stop, and claim-ahead functionality to lock in prices up to 24 hours before fueling.

- • IFTA-compliant receipts emailed automatically after every transaction with state-by-state fuel purchase data for quarterly tax filing.

- • Fleet management tools including per-driver and per-vehicle spending limits, SMS or app-based card unlock before fueling, and telematics-powered fraud prevention confirming vehicle proximity to the pump.

Mudflap is the best fuel card for owner-operators and small trucking fleets that primarily route through independent and regional truck stops where its cost-plus discounts are deepest. The no-fee model removes all financial risk from carrying the card. For fleets that regularly stop at Pilot, Flying J, Love's, or TA/Petro, Comdata's network discounts at those chains will typically outperform Mudflap's independent-stop pricing.