33 Best Mortgage Lenders and Comparison Platforms in 2026

This directory covers the top mortgage lenders and comparison platforms operating in the United States in 2026, ranging from digital-first nonbank lenders like Rocket Mortgage and Better to major banks such as Chase, Wells Fargo, and Bank of America, plus rate marketplaces like LendingTree and Credible. Pricing and origination fee data are sourced from 2024 HMDA federal disclosure data and lender websites, verified April 2026. Note: Ameriquest (shut down 2007), Homepoint (closed 2023), and Caliber Home Loans (merged into Newrez 2021) have been removed as they are no longer operating independently.

Rocket Mortgage

Rocket Mortgage is America's largest retail mortgage lender by volume, founded in 1985 as Quicken Loans and rebranded in 2021. It completed two major acquisitions in late 2025: Mr. Cooper (the largest servicer, for $14.2 billion) and Redfin (the real estate brokerage), creating a combined servicing portfolio covering roughly one in six U.S. mortgages. The One+ program lets eligible borrowers put just 1% down while Rocket contributes an additional 2%. Origination fees typically run $1,500 to $3,000, and mortgage rates have historically been slightly above the national average per HMDA data. J.D. Power ranked it the most awarded mortgage servicer from 2002 to 2025.

- • One+ loan: eligible borrowers contribute 1% down and Rocket funds an additional 2% grant, up to $5,000, with income restrictions

- • RateShield: 90-day rate lock that can float down if market rates fall, priced at roughly 0.75% of the loan amount

- • RentRewards: credits 10% of annual rent (up to $5,000) toward closing costs for renters transitioning to ownership

- • Redfin integration: buyers using a Redfin agent receive either a 1% rate reduction for year one or a lender credit up to $6,000

- • AI Assist (Rocket Assist): natural-language chatbot for mortgage questions, widely praised as the most useful AI assistant in the industry

Rocket Mortgage is the default choice for borrowers who want a polished digital experience, a large and stable servicer, and access to unique programs like One+ and RateShield. The Mr. Cooper and Redfin acquisitions make Rocket the most vertically integrated homeownership platform in the U.S. as of 2026. Borrowers with strong credit who want the lowest possible rate should still compare at least two or three additional lenders, since Rocket's rates and fees are not always the most competitive.

Better

Better (better.com) is a New York-based direct mortgage lender founded in 2014 by Vishal Garg. It charges no origination, application, or underwriting fees, which can save borrowers $1,000–$2,000 compared to traditional lenders. Its One Day Mortgage program issues a full commitment letter within 24 hours for qualifying applicants who link bank accounts digitally. Better operates in all 50 states and Washington D.C., and average origination fees per HMDA data were $2,910 versus a national average of $2,792 — slightly above average despite the no-fee marketing. Interest rates consistently trend below the national average per 2024 federal data. The Better Forever loyalty program waives origination fees on all future purchases or refinances.

- • One Day Mortgage: issues a full loan commitment letter in as little as 24 hours when bank accounts are linked digitally via Plaid

- • Better Forever loyalty program: waives origination fees on any future purchase or refinance for prior Better borrowers

- • Bank Statement HELOC: unique product that uses only bank statements to verify income, benefiting self-employed borrowers

- • Price match guarantee: Better will match a competing lender's rate and give a $100 credit if the borrower ultimately closes with the other lender

- • Betsy AI voice assistant: available for in-app mortgage inquiries and status updates without waiting for a human agent

Better is the strongest choice for straightforward purchase loans where the borrower wants to minimize upfront fees and close quickly. The One Day Mortgage and $0 origination fee combination is genuinely useful in competitive real estate markets. Borrowers with non-standard income or complex credit profiles should consider loanDepot or a lender with more human underwriting flexibility.

loanDepot

loanDepot is a California-based nonbank lender founded in 2010 and one of the largest retail mortgage companies in the U.S., with over $100 billion in loans originated. The mello smartloan platform digitally verifies income, employment, and assets, often eliminating paper documents entirely. The Lifetime Guarantee waives all lender fees on any future loanDepot refinance, and the Close On Time Guarantee pays borrowers and sellers $1,000 if a delay is loanDepot's fault. Average origination fees per 2023 HMDA data were $4,909, above the national average. A 2025 class-action lawsuit alleged that loanDepot pressured loan officers to steer borrowers toward more expensive loans; the company revamped leadership after the filing.

- • mello smartloan: proprietary platform that digitally verifies income and assets, often enabling fully paperless processing

- • Lifetime Guarantee: lender fees and appraisal costs are waived on any future refinance with loanDepot — industry estimate is borrowers refinance every seven years

- • AccessONE+ program: down payment and closing cost assistance of up to $8,000 for first-time buyers in eligible census tracts

- • 200+ physical branch locations nationwide, plus fully remote and hybrid closing options

- • FHA 203(k) renovation loans and jumbo loans up to $5 million round out a wide loan menu that includes FHA, VA, USDA, and conventional

loanDepot works best for borrowers who plan to refinance at least once and want to eliminate fees on that future transaction, or for those buying fixer-uppers who need a 203(k) loan. The hybrid digital-and-branch model appeals to borrowers who like technology but want in-person options. Given the ongoing lawsuit and above-average fees, it is worth collecting competing quotes before committing.

United Wholesale Mortgage (UWM)

United Wholesale Mortgage (UWM), headquartered in Pontiac, Michigan, is the largest wholesale mortgage lender in the U.S. and ranked as the top overall mortgage lender by volume in 2024. Founded in 1986, UWM lends exclusively through independent mortgage brokers — borrowers cannot apply directly. The company went public in 2021 and has partnered with Google AI to modernize its tech platform. Average origination charges per 2024 HMDA data were $5,466. TRAC+ title alternative program cuts title insurance costs to as low as $1,295 for refinances. An April 2025 Ohio attorney general lawsuit alleged UWM and certain brokers charged inflated fees; the case was pending as of April 2026.

- • Wholesale-only model: all loans originate through UWM's network of approved independent mortgage brokers, not direct-to-consumer

- • TRAC+ title alternative: handles title review and closing in-house for refinances starting at $1,295, significantly below typical title insurance premiums

- • 17-day average loan processing time, one of the fastest turn times among large lenders

- • UClose digital closing platform allows virtual notary closings available 24 hours a day, six days a week

- • Conventional, FHA, VA, USDA, jumbo, and non-QM products are available through broker partners nationwide

UWM is genuinely the top choice for borrowers who work with an experienced independent mortgage broker, since UWM's wholesale pricing can beat retail lenders — particularly for VA and FHA loans. It is not suitable for borrowers who want to apply directly, manage their loan independently, or work with a lender that has public rate transparency. Always vet the broker first, since the borrower's experience depends heavily on who they are paired with.

Pennymac

Pennymac is a California-based nonbank mortgage lender and servicer founded in 2008. It originated $134 billion in loans between June 2024 and June 2025 and services a portfolio worth $700 billion. Pennymac is the top FHA lender by volume nationally and one of the top three VA lenders, having financed over $5 billion in VA loans in Q1 2025 alone. Rates consistently trend below national averages per HMDA data, though average origination fees of $4,216 per 2024 HMDA data are above average. The lender does not offer HELOCs or renovation loans. A $1,000 closing credit is available for preapproved customers on eligible loans.

- • Online rate tool: one of the most transparent and detailed rate quote tools in the industry — no contact information required to view initial rates

- • VA leadership: Pennymac is ranked #1 VA lender by Scotsman Guide and financed over $5 billion in VA loans in Q1 2025, with 500,000+ VA loans serviced

- • $1,000 closing credit for preapproved customers on eligible purchase loans, redeemable at closing

- • $2,000 cash bonus for Pennymac purchase customers who refinance with Pennymac within three years

- • Non-QM expansion: Pennymac entered the non-QM market in 2025, adding bank statement loans and investor DSCR mortgages

Pennymac is the strongest choice for VA and FHA borrowers who prioritize below-average rates and want to compare pricing without submitting personal information upfront. The $1,000 preapproval credit and 1% temporary rate buydown add real value. The poor J.D. Power origination score is a meaningful concern; borrowers should read recent reviews before committing.

Newrez

Newrez is a national mortgage lender and servicer based in Fort Washington, Pennsylvania, founded in 2008 and now a subsidiary of Rithm Capital. It absorbed Caliber Home Loans in 2021, quadrupling its market share over five years. Newrez offers a 'Smart Series' of non-QM products including SmartSelf (bank statement loans for self-employed borrowers), SmartEdge (for borrowers with credit blemishes), and SmartVest (for real estate investors). The RezSource program enables 1%-down conventional loans with up to $5,000 in down payment assistance. Average origination fees were approximately $4,096 per 2024 data, above the national average. Newrez can close some loans in as few as 10 days with its $5,000 Close-on-Time Guarantee.

- • Smart Series non-QM loans: four distinct programs for self-employed (SmartSelf), credit-challenged (SmartEdge), investors (SmartVest), and high LTV (SmartStart)

- • RezSource: conventional purchase loan with 1% minimum down and up to $5,000 in lender-provided down payment assistance

- • HELOC available up to $350,000 (U.S. News) / $400,000 (Newrez website) at fixed or variable rates; requires 660+ credit score

- • $5,000 Close-on-Time Guarantee paid from Newrez if lender delays cause a missed closing date

- • Loans up to $3.5 million including jumbo and non-QM products for high-value properties

Newrez is the best option on this list for borrowers who don't fit standard lending guidelines — particularly the self-employed, real estate investors, or those rebuilding credit. For everyone else, rates and fees are high enough that shopping alternatives first makes sense. The Caliber Home Loans customer base is now fully on the Newrez platform.

Freedom Mortgage

Freedom Mortgage, founded in 1990 and headquartered in Boca Raton, Florida, is one of the largest FHA and VA lenders in the U.S. Over half of its 2024 loan originations were VA loans, placing it third nationally for VA purchase volume. The company services most of the mortgages it originates, reducing the chance of mid-loan transfers. Average origination fees per HMDA data are $5,282 — nearly double the national average of $2,792 — though rates are often below average, which can offset upfront costs over time. Freedom was fined $3.95 million in 2024 by the CFPB for submitting inaccurate loan data; the bureau labeled it a repeat offender in this area.

- • VA loan expertise: one of the top three VA lenders nationally by volume, with deep experience in VA IRRRLs, cash-out refis, and purchase loans

- • Eagle Eye program: proactively monitors current Freedom borrowers' loan terms and alerts them when a refinance opportunity appears

- • Loan servicing: Freedom retains servicing on most loans it originates, so borrowers are unlikely to face a servicer transfer

- • Available nationwide in all 50 states and D.C., including Puerto Rico and U.S. Virgin Islands for VA loans

- • FHA streamline refinance and VA IRRRL programs available without an appraisal for eligible existing mortgage holders

Freedom Mortgage is best for veterans who want a specialist with deep VA experience and are comfortable trading higher upfront fees for competitive long-term rates. The CFPB fine history and lack of online pricing transparency are material negatives. Borrowers should obtain at least one competing VA quote from Pennymac or Veterans United before deciding.

Guild Mortgage

Guild Mortgage, founded in 1960 and headquartered in San Diego, is one of the largest independent mortgage companies in the U.S. with over 350 branches in 49 states (excluding New York). In late 2025, Guild was acquired by Bayview Asset Management. The Complete Rate program accepts alternative credit like rent history, utility payments, and car insurance as substitutes for traditional FICO scores on FHA, VA, and USDA loans. Guild's 1%-down program provides 2% in lender grant assistance up to $5,000. Average origination fee per 2024 HMDA data was $3,928 with average total loan costs of $8,061, both above national averages. J.D. Power ranked Guild second nationally for mortgage servicer satisfaction in 2025.

- • Complete Rate program: accepts rent, utility, and insurance payment history as alternative credit for FHA, VA, and USDA loans — among the most flexible credit underwriting of any lender

- • 1%-down program: borrowers put down 1% and Guild contributes an additional 2% grant (up to $5,000); subject to income limits

- • HELOC up to 95% LTV with a loan limit of $750,000 and a fixed-rate option — one of the highest LTV HELOCs from a retail lender

- • Physician loan available up to $850,000 with no down payment and no PMI for residents, doctors, dentists, vets, and pharmacists

- • MyPath2Own homeownership readiness plan with up to $4,000 in closing cost or down payment assistance

Guild Mortgage stands out for first-time buyers and non-traditional credit profiles who benefit most from in-person guidance and alternative credit underwriting. The high fees are the main drawback; borrowers with strong conventional credit may find better pricing at a digital-first lender. The Bayview Asset Management acquisition has not changed day-to-day operations as of April 2026.

Movement Mortgage

Movement Mortgage, founded in 2008 and headquartered in South Carolina, originates approximately $20 billion in loans annually through more than 775 branches. It has donated $377 million to community causes through the Movement Foundation, marketing itself as an 'impact lender.' Movement scored above average in J.D. Power's 2025 mortgage origination satisfaction study. Mortgage servicing is handled by Carrington Mortgage Services, which scored below average in J.D. Power's 2025 servicer study. Rates are not published online; borrowers must contact a loan officer.

- • 775+ branch locations across the U.S. — one of the largest physical footprints among nonbank lenders

- • Above-average J.D. Power 2025 mortgage origination satisfaction score — among the highest of any lender reviewed by NerdWallet

- • Movement Foundation: the company distributes 40–50% of profits to charitable causes including charter schools and community development

- • Custom rate quotes available online without requiring full prequalification or a hard credit inquiry

- • Conventional, FHA, VA, USDA, jumbo, and renovation loans available with local loan officer support

Movement Mortgage is the best choice for buyers who want high-touch local service and don't mind connecting with a loan officer early. The J.D. Power origination satisfaction ranking is a genuine differentiator. The post-close servicing handoff to Carrington is the main concern; borrowers should be aware that payment management and servicing questions will go to a different company after closing.

Flagstar Bank

Flagstar Bank, founded in 1987 and now headquartered in Hicksville, New York (after acquisition by New York Community Bancorp in 2022), offers mortgages nationwide through its website but has physical branches only in Arizona, California, Florida, Indiana, Michigan, New Jersey, New York, Ohio, and Wisconsin. In late 2024, Flagstar sold its mortgage servicing and third-party origination platform to Mr. Cooper Group (now part of Rocket), meaning Flagstar-originated loans are serviced by others. Flagstar offers fixed-rate terms up to 40 years — unusually flexible — and a proprietary Destination Home Mortgage with no down payment and no mortgage insurance for qualifying borrowers.

- • Destination Home Mortgage: proprietary no-down-payment, no-mortgage-insurance loan for qualifying borrowers — rare in the industry

- • 40-year fixed-rate term: one of the few lenders offering this extended term, which lowers monthly payments for budget-constrained borrowers

- • Down payment assistance: Gift Program offers up to $3,500 in select markets; up to $7,500 in AZ, CA, NJ, and NY

- • Loans for borrowers without a Social Security number (ITIN loans) and for non-warrantable condos

- • Construction-to-permanent loans, FHA 203(k) renovation loans, and Fannie Mae HomeStyle Renovation available

Flagstar is worth considering for borrowers in its nine branch states who need the Destination Home zero-down program or a 40-year fixed term. For everyone else, the poor post-sale servicing reputation and sparse branch coverage make it a secondary choice. Always verify that the specific product you want is available in your state before starting an application.

PNC Bank

PNC Bank, headquartered in Pittsburgh and among the top seven banks in the U.S. with $564 billion in assets, offers mortgages in all 50 states through 2,300+ branches (primarily in eastern and central states). PNC publishes live mortgage rates online without requiring a credit check or contact information — an advantage over many competitors. Rates tend to sit near or slightly below the national average per HMDA data. The PNC Community Loan offers 3% down with no private mortgage insurance. Grant programs offer $2,500 to $15,000 in closing cost or down payment assistance to eligible low- and moderate-income borrowers. A $500 closing cost discount is available March 1–April 30, 2026 on new applications.

- • Community Loan: 3% down with no private mortgage insurance for eligible low-to-moderate income borrowers in qualifying markets

- • Grant programs: Low Income Grant ($2,500), Low-to-Moderate Income Grant ($3,000–$5,000), and PNC Grant ($5,000–$15,000) stack to cover significant upfront costs

- • Home Insight Tracker: digital portal for tracking application status, uploading documents, and communicating with the loan officer throughout closing

- • Doctor loan (Medical Professional Program): up to $1.5 million with no PMI and cash gifts allowed as part of the down payment

- • HELOC with Choice feature: allows borrowers to convert a variable-rate draw balance to a fixed rate at any point during the draw period

PNC is the best large-bank choice for low-to-moderate income first-time buyers in its branch footprint who can qualify for the grant stacking programs. The transparent rate tool is genuinely useful for comparison shopping. For borrowers outside PNC's core eastern and central territory, Chase or Bank of America provide more consistent nationwide service.

Chase

Chase Home Lending, the mortgage division of JPMorgan Chase, is the largest bank in the U.S. and a top-five mortgage originator. Chase offers mortgages nationwide through 4,700+ branches and a full-featured online application. Average origination fees per 2024 HMDA data were $2,668, slightly below the national average of $2,792, and rates averaged just 0.11 percentage points above the average prime offer rate (APOR) in 2024 — making Chase a competitive large-bank option. The DreaMaker loan requires just 3% down for low-to-moderate income borrowers. Jumbo loans are available up to $9.5 million. J.D. Power ranked Chase third for mortgage origination satisfaction in 2024.

- • DreaMaker loan: 3% down with reduced mortgage insurance for income-eligible borrowers; available in 15,000+ qualifying communities nationwide

- • $5,000 homebuyer grant: available for down payment or closing costs in specific communities; also a separate $5,000 grant for Agent Express agent referrals

- • Closing guarantee: Chase pays the buyer and seller $5,000 if lender delays cause a closing past the contract date (21 days conventional, 30 days FHA/VA)

- • Rate discount up to 1% for existing Chase customers based on account assets

- • Jumbo loans up to $9.5 million; 10-year interest-only jumbo ARM is available — a product few large banks still offer

Chase is one of the better large-bank mortgage options thanks to competitive fees, J.D. Power satisfaction ranking, and the 21-day closing guarantee. The $5,000 community grant is real value for qualifying buyers. Existing Chase customers with significant deposits stand to gain the most through relationship discounts. Non-customers should compare rates with at least one additional lender before committing.

Bank of America

Bank of America is the second-largest U.S. bank and a major mortgage originator with 3,700+ branches nationwide. The America's Home Grant program provides up to $7,500 toward non-recurring closing costs in select markets, and a down payment grant covers up to 3% of the purchase price (maximum $10,000) in qualifying areas. Combined, eligible buyers can receive up to $17,500. The Affordable Loan Solution program requires just 3% down with no PMI. J.D. Power ranked Bank of America with an exceptional score in the 2025 mortgage origination satisfaction study — one of the highest of any lender on this list. Preferred Rewards customers can receive up to $600 off origination fees and rate discounts up to 0.375%.

- • Affordable Loan Solution: 3% down with no PMI, available in partnership with Freddie Mac and Self-Help Ventures Fund; no maximum income limit nationally

- • America's Home Grant: up to $7,500 in lender-provided closing cost credits in BofA branch markets

- • Home Loan Navigator: digital portal for uploading documents, e-signing, and tracking loan status in real time — available on mobile and desktop

- • Preferred Rewards: Platinum Honors tier ($1M+ in assets) receives a 0.375% rate discount and $600 origination fee reduction

- • Medical professional loans available up to undisclosed amount with no PMI and student debt exclusion from DTI calculations

Bank of America is the best large-bank pick for buyers who qualify for its grant programs or hold significant Preferred Rewards deposits. The J.D. Power satisfaction rating is exceptional and the digital tools are polished. Without Preferred Rewards or grant eligibility, rates are not as competitive as Chase or Wells Fargo — borrowers in that situation should collect competing quotes before committing.

Wells Fargo

Wells Fargo is the fourth-largest U.S. bank with $1.76 trillion in assets and 5,600+ branches, although it has actively narrowed its mortgage business since 2022 to focus on existing bank customers and underserved communities. It no longer offers HELOCs or home equity loans — cash-out refinancing is the only equity access option. The 'Dream. Plan. Home.' closing cost credit and Homebuyer Access grant provide up to $10,000 for eligible buyers. Borrowers with $250,000 or more in Wells Fargo accounts qualify for rate discounts of 0.125%–1.25%. Rates average competitively below the national median per 2024 HMDA data. Past regulatory issues include a $4 billion CFPB settlement in 2022 and a $250 million OCC fine in 2021.

- • Dream. Plan. Home. mortgage: 3% down conventional loan for low-to-moderate income borrowers; non-traditional credit accepted

- • PriorityBuyer instant preapproval: highly qualified borrowers can receive a preapproval letter within minutes online

- • 1,000+ locations offering in-person mortgage support — more than most other banks reviewed here

- • USDA loans available — one of the few large banks that still actively originates USDA rural development loans

- • Rate discount structure for existing customers starts at $20,000 in deposits ($1,000 closing credit) and scales to $250,000+ (1.25% rate reduction)

Wells Fargo is worth considering for existing customers who hold $250,000+ in deposits and can unlock meaningful rate discounts, or for rural buyers who need a USDA loan from a big bank. The lack of HELOC and home equity loan products is a real gap. For borrowers without relationship pricing, competing lenders often offer comparable or better rates with fewer regulatory red flags.

Citibank

Citibank (CitiMortgage) is the third-largest U.S. bank and a top jumbo loan lender, with jumbo mortgages accounting for 48% of Citi's purchase originations in 2024. J.D. Power ranked Citi first nationally for mortgage origination satisfaction in 2025 — the top score of any lender reviewed here. The HomeRun Mortgage requires just 3% down on single-family homes with no PMI, aimed at low-to-moderate income borrowers earning up to 120% of area median income. Existing Citi customers with as little as $1 in an account qualify for a $500 closing cost credit; those with $2 million+ in assets receive up to a 5/8% rate reduction. Citi stopped servicing its own mortgages in 2018; loans are serviced by Cenlar FSB post-closing.

- • HomeRun Mortgage: 3% down, no PMI, flexible credit requirements for single-family homes and condos in select metro areas including Atlanta, Austin, Dallas, Denver, Houston, Philadelphia, and Cambridge

- • SureStart preapproval: Citi commits to the loan amount with higher certainty than a standard preapproval — billed as a 'commitment to lend'

- • Jumbo strength: jumbo loans account for 48% of Citi's purchase originations; available up to $5 million nationally

- • Rate transparency: Citi publishes current mortgage rates on its website and updates them daily, making comparison shopping straightforward

- • $500 closing cost credit for any Citi customer, with additional savings scaling to 5/8% rate reduction at $2M+ balance

Citi is the strongest big-bank pick for existing customers and jumbo loan borrowers who want the best-rated origination experience. The HomeRun no-PMI 3%-down program is a real differentiator. The outsourced servicing model and F BBB rating are the main concerns. Borrowers should verify that Cenlar FSB's servicing model is acceptable before committing.

U.S. Bank

U.S. Bank, founded in 1863 and headquartered in Minneapolis, is one of the largest banks in the country with more than 2,100 branches in 26 states. It offers mortgages in all 50 states and publishes current rates online without requiring contact information. Average origination fees per HMDA data were approximately $1,352 — among the lowest of any large bank reviewed here and well below the $2,792 national average. The Access Home Loan and American Dream programs provide closing cost assistance for low-income borrowers, with up to $12,500 available through special programs. Existing customers with a U.S. Bank Smartly, Gold, or Platinum checking account can receive up to $1,000 off closing costs.

- • Low origination fees: $1,352 average per HMDA data is less than half the national average, translating to material upfront savings

- • American Dream and Access Home Loan programs: up to $12,500 in combined down payment and closing cost assistance for income-eligible buyers

- • Same-day preapproval available online — one of the faster large bank preapproval processes

- • FHA minimum credit score is 640 at U.S. Bank — 60 points higher than the 580 required by federal guidelines and many competitors

- • USDA loans, construction loans, and investment property loans available — broader product menu than most banks reviewed here

U.S. Bank is the strongest large bank for borrowers focused on minimizing origination fees, particularly those who already bank there and can access the $1,000 closing credit. The above-average mortgage rates partially offset the low fees; borrowers should compare total costs (rate + fees) rather than judging on origination fee alone.

TD Bank

TD Bank is a large regional bank with more than 1,500 locations operating in 15 states plus Washington D.C. (primarily Northeast, Mid-Atlantic, and Southeast). It is not available in most of the central and western U.S. Mortgage rates per 2024 HMDA data ran 0.93 percentage points above the average prime offer rate (APOR), a widening from 0.71 in 2023. Average origination fees per 2024 FFIEC data were approximately $822. TD Bank offers conventional, FHA, VA, USDA, and jumbo loans plus construction loans, home equity loans, and HELOCs starting at $25,000. A 0.25% rate discount on HELOCs and home equity loans is available for TD checking or savings account holders with autopay.

- • HELOC starting at $25,000 with no minimum draw required and option to convert to fixed rate — more flexible than many bank HELOCs

- • Home equity loans in 5-, 10-, 15-, 20-, and 30-year terms; available for primary residences, second homes, and investment properties

- • Construction loans offered — a product many large banks have discontinued

- • Medical professional loans with low down payments and no PMI for doctors, dentists, and other licensed professionals

- • Mortgage available in all 15 states plus D.C. where TD has branches; digital application available to all

TD Bank is the right choice for existing TD customers in its 15-state footprint who want low origination fees, strong home equity products, and specialty options like construction or medical professional loans. The rate spread is a meaningful drawback; compare TD's APR against Chase and PNC before deciding, particularly for larger loan amounts where rate differences compound significantly.

Regions Bank

Regions Bank is a large regional bank headquartered in Birmingham, Alabama, with approximately 1,300 branches primarily in the South and Midwest. It offers conventional, FHA, VA, USDA, and jumbo mortgages plus construction, renovation, and physician loans. Regions publishes mortgage rates online. Average origination fees per HMDA data are below the national average, though rates tend to run slightly above average. The bank participates in multiple down payment assistance programs, including the Federal Home Loan Bank's NeighborWorks program in some markets. Regions services most of the loans it originates in-house.

- • Rates published online for conventional, FHA, VA, and USDA loans — useful for early comparison shopping

- • Construction loans and physician loans available, broadening the product menu beyond standard retail bank offerings

- • In-house loan servicing: Regions retains servicing on most originated mortgages, reducing the risk of payment disruptions from servicer transfers

- • Over 1,300 branch locations concentrated in Alabama, Arkansas, Florida, Georgia, Illinois, Indiana, Iowa, Kentucky, Louisiana, Mississippi, Missouri, North Carolina, South Carolina, Tennessee, and Texas

- • USDA loans available — one of the few regional banks to actively originate this product, useful for rural buyers in its footprint

Regions is a solid option for borrowers who live near a Regions branch in the South or Midwest and prefer a traditional bank relationship with low fees and in-house servicing. Borrowers focused on rates should run a comparison with Truist, which regularly appears among the lowest-rate lenders in this geography per Yahoo Finance's weekly rate survey.

SoFi

SoFi is a San Francisco-based online financial services company that acquired Wyndham Capital Mortgage in 2023 and has funded more than $9 billion in mortgages since entering the market in 2014. It is available in all 50 states for purchases, but does not offer refinances in New York. SoFi charges a standard origination fee of $1,495, reduced to $995 for SoFi members ($500 discount) and $495 for SoFi Plus members ($1,000 discount). Rates trend below national averages per HMDA data. The 91-day rate lock with a free float-down is among the longest in the industry, and the $10,000 close-on-time guarantee is the highest among lenders reviewed here.

- • 91-day rate lock with free float-down: if market rates drop by 0.25% or more, borrowers can re-lock at the lower rate at no cost — the longest standard lock period reviewed here

- • $10,000 close-on-time guarantee: the highest on-time closing protection of any lender in this list, paid if a SoFi-caused delay pushes closing past the contract date

- • HomeStory rebate: up to $9,500 cashback at closing for buyers who work with a SoFi partner agent (average actual rebate is approximately $1,700)

- • VA loans: SoFi waives its origination fee entirely for VA borrowers — only the VA funding fee applies

- • Jumbo loans up to $3 million with no PMI, including for loan amounts above the $832,750 conforming limit

SoFi is the strongest choice for existing SoFi members who want to minimize origination fees and protect their rate during a long home search. The 91-day float-down lock and $10,000 closing guarantee are genuinely differentiating. Non-members should weigh whether the $995 post-discount fee is competitive against Better's $0 origination or AimLoan's flat $995 fee.

Citizens Bank

Citizens Bank is a regional bank headquartered in Providence, Rhode Island, with branches in 14 states plus Washington D.C. (primarily Northeast and Midwest). It offers conventional, FHA, VA, and jumbo mortgages as well as construction-to-permanent loans, HELOCs, and cash-out refinancing. Citizens publishes sample rates online for conventional loans. The HELOC can close in as little as seven days with no up-front fees or closing costs — one of the fastest HELOCs on the market. No home equity loans are available. Average mortgage rates per HMDA data are above the national median. J.D. Power scored Citizens Bank at approximately the industry average for mortgage servicer satisfaction in 2024.

- • HELOC with 7-day close and no closing costs: one of the fastest home equity line of credit approvals in the industry

- • Construction-to-permanent loan: a single loan that covers both the building phase and the permanent mortgage, reducing closing costs and paperwork

- • Rate discounts for autopay or paperless billing — modest savings for borrowers who opt into these options

- • Online prequalification with personalized rate display — visible without completing a full application

- • Available in 14 states and D.C., with digital services offered nationwide for borrowers outside the branch footprint

Citizens Bank is worth a look specifically for borrowers who need fast HELOC access or a construction-to-permanent loan in its 14-state footprint. For standard purchase mortgages, the above-average rates make it less competitive than Chase or Truist. Get quotes from at least one other lender before committing to a Citizens mortgage.

Truist

Truist Bank, formed from the 2019 merger of BB&T and SunTrust, is the ninth-largest U.S. bank by assets and headquartered in Charlotte, North Carolina. It operates in 17 states plus Washington D.C. with branches concentrated in the Southeast and Mid-Atlantic. Truist ranked as the 24th-largest mortgage lender in 2024 and has expanded plans to open 100 new branches in high-growth cities through 2030. Mortgage rates tend to run below the national average per Bankrate's affiliate data. Truist offers a zero-down Community Homeownership Incentive Program (CHIP) for income-qualifying buyers in some markets, and up to $10,000 in grants for buyers in D.C., Richmond, Atlanta, and surrounding areas. J.D. Power scored Truist far below average in the 2025 mortgage origination satisfaction study.

- • CHIP program: zero to 3%-down conventional loan with no mortgage insurance for income-qualifying borrowers in FL, GA, NC, SC, and VA markets

- • Physician loan up to $2 million with 89.99% financing and no PMI for practicing doctors and dentists; up to $1 million with 0% down for residents and interns

- • USDA loans available: one of the few large bank-affiliated lenders that still actively originates USDA rural development mortgages

- • Jumbo loans up to $5 million available at competitive rates for well-qualified buyers

- • Sample rates published online with the ability to see pricing with and without discount points — one of the clearest rate displays of any bank reviewed

Truist offers some of the most competitive rates among large banks per recent surveys, and its CHIP, USDA, and physician programs cover hard-to-find borrower scenarios. The extremely low J.D. Power origination satisfaction score is the main red flag. Borrowers should set clear expectations with their loan officer upfront and confirm fee details in writing before proceeding.

Fifth Third Bank

Fifth Third Bank is a Cincinnati-based bank with nearly 1,100 branches and $212 billion in assets, placing it among the top 20 largest U.S. banks. It offers mortgages in its Midwest and Southeast branch footprint plus selected other states. The Rate Drop Protector program allows borrowers who purchase now to refinance later with no lender closing costs if rates fall — a useful hedge in a volatile rate environment. Fifth Third offers up to $3,600 in non-repayable down payment assistance through its Community Mortgage Loan. J.D. Power scored Fifth Third above the industry average in the 2025 mortgage servicer satisfaction study. Physician loans are available up to $2.5 million.

- • Rate Drop Protector: eligible purchase borrowers can refinance with no Fifth Third lender closing costs if rates fall — a rare commitment from a large bank

- • Community Mortgage Loan: up to $3,600 in non-repayable down payment assistance with no income limit in many markets

- • Physician loan up to $2.5 million with low down payment and no PMI; available to residents, fellows, and practicing physicians and dentists

- • Above-industry-average J.D. Power servicer satisfaction score in 2025 — meaningful for long-term loan management

- • 0.25% rate discount available for borrowers who set up automatic payments from a Fifth Third account

Fifth Third is the best choice for Midwest and Southeast buyers who want to purchase now in a rate-uncertain environment and want protection if rates fall. The Rate Drop Protector benefit is meaningfully differentiated. Borrowers outside its branch footprint or who need USDA financing should consider alternatives.

NBKC Bank

NBKC Bank is a community bank founded in 1999 and headquartered in Leawood, Kansas, with four branches in the Kansas City metropolitan area but a national mortgage footprint across all 50 states. It offers conventional, jumbo, FHA, and VA loans plus a 1-0 buydown program. The flat $250 origination fee on conventional loans is among the lowest hard-dollar origination charges of any lender reviewed here. NBKC offers a $5,000 close-on-time guarantee split between buyer and seller. VA loans accounted for more than a quarter of NBKC's 2024 originations. NerdWallet and Bankrate both rate NBKC with an A+ BBB rating and strong customer satisfaction from loan officers.

- • Flat $250 conventional origination fee: a hard-dollar charge that is transparent and far below the national average

- • 1-0 buydown product: lender-funded 1% rate reduction for the first year — positions borrowers for a potential refinance if rates continue falling

- • VA loan expertise: VA loans account for over 25% of originations, indicating deep familiarity with the VA approval process

- • A+ BBB rating with 4.85/5 from 500+ customer reviews — among the strongest third-party ratings of any lender reviewed here

- • Live chat and phone support available Monday–Friday 9 AM–8 PM ET; exceptionally fast loan officer response noted in reviews

NBKC is the best choice for VA borrowers and conventional loan borrowers who are comfortable with an online lender and want to minimize origination costs. The $250 flat fee and strong customer satisfaction scores are genuinely differentiating. The limited product menu (no USDA, no renovation, no HELOC) means borrowers with those needs must look elsewhere.

Carrington Mortgage

Carrington Mortgage Services, headquartered in Anaheim, California, specializes in government-backed and non-QM mortgages for borrowers who fall outside conventional credit standards. FHA loans made up a large portion of Carrington's 2024 originations. The lender accepts credit scores as low as 500 for FHA loans with 10% down, lower than the 580 many lenders require. Carrington is also the servicing partner for Movement Mortgage loans. It offers bank statement programs, asset depletion loans, and investment property mortgages for borrowers who do not qualify through traditional income documentation. Carrington scored below average in J.D. Power's 2025 mortgage servicer satisfaction study.

- • 500 minimum FICO for FHA loans: accepts credit scores 80 points below what lenders like U.S. Bank or Guild require, expanding access significantly

- • Bank statement mortgage: uses 12–24 months of bank statements to qualify self-employed borrowers without traditional tax return income verification

- • Asset depletion loan: allows retired borrowers or those with liquid assets to qualify using assets converted to income, without W-2 or pay stubs

- • DSCR (Debt Service Coverage Ratio) investment loan: qualifies real estate investors based on property rental income rather than personal income

- • Available in all 50 states with both retail and wholesale channels, and Carrington is the servicer for Movement Mortgage's loan portfolio

Carrington is the right choice for borrowers with credit scores in the 500–580 range who need FHA access that most lenders won't provide, or for self-employed and investor borrowers who need non-QM products from a single lender. The below-average servicer satisfaction is the main concern; set expectations upfront and confirm fee and rate details in writing.

AmeriSave

AmeriSave Mortgage Corporation, founded in 2002 and headquartered in Atlanta, is a direct online lender that has funded more than $130 billion to over 773,600 borrowers across its history. It accepts credit scores as low as 500 for FHA loans and is licensed in all 50 states except New York. The Lock & Drop buydown program reduces your rate by 1% for the first year and includes a $750 credit toward a future refinance. Average interest rates trend below the national median per HMDA data, but origination fees run above average. No mobile app is available for loan management.

- • Lock & Drop: 1%-lower rate for the first year of the mortgage, funded by the lender, with a $750 credit included for a future refinance

- • FHA loan volume: FHA loans make up a disproportionately large share of AmeriSave's originations compared to most nonbank lenders — indicating institutional expertise

- • HELOC requiring full draw at origination: AmeriSave's HELOC requires borrowers to withdraw the entire line at closing — a full-draw requirement that is unusual and worth confirming before applying

- • HELOCs up to $350,000 and home equity loans up to $500,000 with a 20-year fixed term available

- • Over 20 years in business since 2002, making it one of the more established digital mortgage companies

AmeriSave is a solid option for FHA borrowers and buyers who want a pure digital experience with rates below the national average. The full-draw HELOC and no mobile app are meaningful limitations for existing homeowners. Borrowers in New York must use a different lender entirely.

AimLoan

AimLoan (American Internet Mortgage, NMLS #2890), founded in 1998 by Vince Kasperick and headquartered in San Diego, is a veteran direct-to-consumer online lender that has funded approximately $25 billion in home loans over 26 years. It charges a flat $995 lender fee on conventional and VA loans, and rates are published online 24/7 without requiring contact information — a level of transparency rare in the industry. AimLoan funded roughly $250 million in loans in 2024 (smaller scale than major lenders), and is most active in Arizona, California, Florida, North Carolina, Texas, and Virginia. It does not offer FHA loans or USDA loans. Consistently positive customer reviews note fast closings and clear communication.

- • 24/7 live rate quotes: rates and APRs are published online and updated daily without requiring contact information or a credit pull

- • Flat $995 lender fee on conventional and VA loans — transparent, predictable, and below the national average origination charge

- • Rates regularly among the lowest on Zillow Mortgage Marketplace per third-party reviews; at the time of a 2025 review, offered the lowest APR in sample scenarios

- • HomeReady mortgage (Fannie Mae conventional with 3% down) available as a substitute for FHA for borrowers who don't qualify for standard conventional

- • Licensed in all 50 states and D.C.; fully online with phone support available; loan officers are salaried, not commissioned

AimLoan is the strongest choice for rate-focused, self-directed borrowers who want to shop rates without giving up their contact information and want to minimize lender fees on conventional or VA loans. The lack of FHA and USDA is a hard cutoff for borrowers who need those programs. For straightforward conforming loans, AimLoan's transparency and low fees make it a top comparison point.

Rate

Rate, founded in 2000 and headquartered in Chicago, is one of the largest retail mortgage lenders in the U.S. with over 700 offices in all 50 states. It acquired Stearns Lending in early 2021 and has grown significantly. The platform offers a fully digital mortgage process with live rate quotes online without requiring contact information for conventional loans. Rate publicly discloses closing costs on its website more explicitly than most competitors. Products include conventional, FHA, VA, USDA, jumbo, renovation (203(k) and HomeStyle), and non-QM loans. Average processing times tend to be faster than the 42-day industry average.

- • Digital Mortgage platform: fully online application, document upload, e-sign, and loan tracking from any device

- • Fee transparency: Rate discloses expected closing cost ranges on its website, including lender fees, before requiring a full application

- • FHA 203(k) and Fannie Mae HomeStyle renovation loans available: covers both government and conventional renovation financing in one lender

- • USDA loans and non-QM (including bank statement and DSCR) available — one of the widest product menus among tech-forward retail lenders

- • 700+ offices nationwide provides in-person support where digital-only lenders fall short

Rate is a strong midpoint option for borrowers who want a tech-forward digital experience with the option to walk into a branch. The fee transparency and product breadth (renovation, USDA, non-QM) make it worth comparing. Borrowers should verify their personalized rate and fee quote against at least two other lenders before committing.

LendingTree Mortgage

LendingTree is a marketplace platform founded in 1996 and headquartered in Charlotte, North Carolina, that connects borrowers with over 500 vetted mortgage lenders. It does not originate loans directly; instead, borrowers submit a single form and receive competing offers from multiple lenders simultaneously. A 2025 LendingTree analysis found that buyers in major metro areas saved an average of $80,024 over the life of a 30-year mortgage by comparing lenders through platforms like LendingTree. Submitting information does not trigger a hard credit pull on the LendingTree platform itself, though individual lenders will run hard inquiries when borrowers proceed with applications. LendingTree's home equity revenue grew 38% year-over-year in Q2 2025.

- • 500+ lender network: one of the largest partner lender networks of any mortgage marketplace, including Rocket Mortgage, Zillow Home Loans, and AmeriSave

- • Single form, multiple competing offers: one prequalification form surfaces multiple loan quotes side by side, enabling true comparison shopping

- • No hard credit pull: the LendingTree platform uses a soft inquiry to generate initial offers; only the chosen lender performs a hard pull

- • Mortgage calculators, refinance breakeven tools, and credit monitoring tools available alongside rate comparisons

- • Rate analysis: LendingTree regularly publishes HMDA-sourced data showing which lenders charge the lowest average rates — useful for verifying advertised claims

LendingTree is the most powerful rate comparison tool for borrowers who want maximum lender exposure and are comfortable managing a high volume of follow-up contact. It is a shopping tool, not a lender; always independently verify the reliability and terms of any lender you choose to proceed with. If unsolicited calls are a concern, Credible's quieter model may suit better.

Credible

Credible is an online marketplace founded in 2012 and headquartered in San Francisco that partners with a curated network of mortgage lenders. Unlike LendingTree, Credible does not share borrower contact information with lenders until the borrower actively chooses to proceed — a 'no-spam' approach that reduces unwanted outreach. Prequalified rates are generated with a soft credit pull and shown side-by-side in a clear dashboard. Credible's lender network is smaller than LendingTree's 500+ but is focused on vetted, reputable lenders. The platform is free to borrowers; revenue comes from lender referral fees.

- • No-spam model: borrower contact information is withheld from lenders until the borrower explicitly initiates contact with a specific lender

- • Soft credit pull: Credible generates personalized, prequalified rates using a soft inquiry — no impact to credit score during shopping

- • Side-by-side comparison dashboard: displays rate, APR, monthly payment, and estimated closing costs in a format that makes comparison straightforward

- • Rate shopping for purchase, refinance, and home equity loans on one platform

- • Best for: borrowers with standard income and property types; complex scenarios (self-employed, non-QM) may receive fewer or less competitive offers

Credible is the best mortgage marketplace for borrowers who value privacy and a lower-pressure shopping experience. It sacrifices lender breadth for comfort. Use Credible to get an initial comparison, then verify the most competitive offer you find against one or two direct lender quotes before committing.

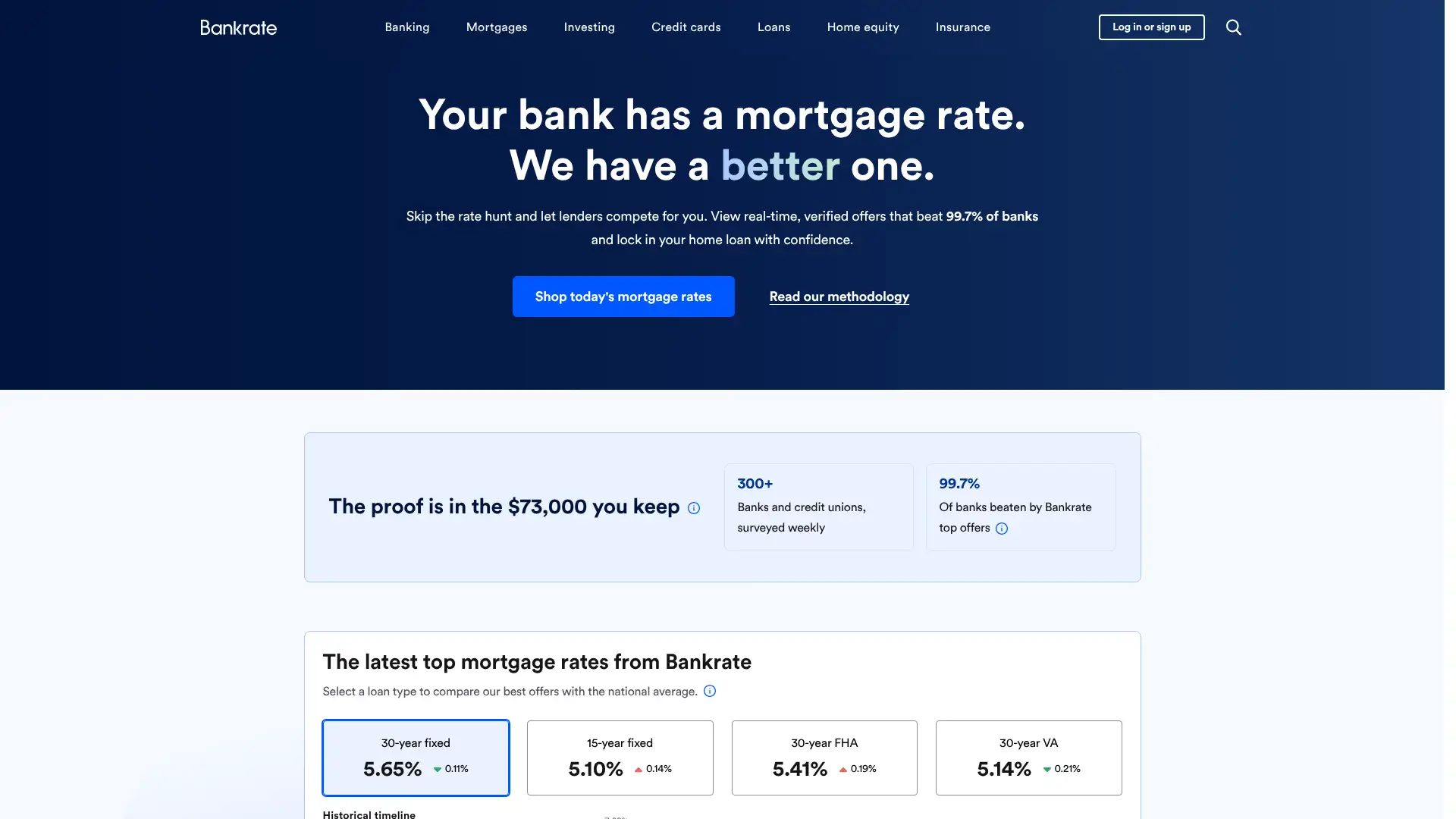

Bankrate Mortgage

Bankrate is a financial content and comparison platform founded in 1976 (originally print, online since 1996), owned by Red Ventures. Its mortgage section publishes the national average 30-year fixed mortgage APR (6.58% as of April 6, 2026) based on a survey of the largest banks and thrifts across hundreds of U.S. markets. Bankrate's rate tables show live offers from partner lenders including interest rate, APR, and estimated monthly payment. Borrowers can filter by loan type, term, and credit score range. Unlike pure marketplaces, Bankrate combines editorial reviews, rate data, and lender comparisons — making it valuable as both a research tool and a lead generation platform.

- • Daily national rate survey: tracks 30-year fixed, 15-year fixed, ARM, FHA, VA, and jumbo rates from major lenders across hundreds of U.S. markets

- • Top offer rate table: shows live competitive lender offers alongside the national average so borrowers can immediately see the gap

- • Editorial lender reviews: 100+ in-depth mortgage lender reviews written by staff journalists, rated on affordability, availability, and customer experience

- • Mortgage calculator suite: payment calculator, amortization, refinance breakeven, and affordability tools available without registration

- • Rate alert service: borrowers can sign up for daily email updates when mortgage rates change

Bankrate is the most useful starting point for any borrower doing mortgage research because of its authoritative daily national rate survey and comprehensive lender reviews. Use it to benchmark what competitive rates look like before engaging with individual lenders. For actual loan applications, proceed to the lender directly or use LendingTree to collect multiple competing offers at once.

Zillow Home Loans

Zillow Home Loans is the direct mortgage arm of Zillow Group, launched in 2019 to complement the company's home search platform. Zillow was acquired by Rocket Companies along with Redfin in mid-2025, completing Rocket's push to control the full homeownership journey from search to financing. Zillow publishes rates online for conventional, FHA, VA, and ARM loans. Average origination charges per 2024 HMDA data were $4,039 with total loan costs of $8,111 — above the national average. Rates averaged 0.40 percentage points above the APOR in 2024. No HELOCs are offered directly (partner lenders are matched), and no USDA loans are available.

- • Seamlessly integrated with Zillow home search: saved homes, affordability calculators, and mortgage preapproval appear in the same platform

- • Rates published online for multiple loan types without requiring contact information — useful for early comparison

- • Down payment assistance programs in select markets visible through Zillow's online questionnaire

- • Post-Rocket acquisition: buyers working with a Redfin agent can receive a 1% year-one rate reduction or $6,000 closing credit when financing through Rocket/Zillow

- • Available for purchase mortgages in all 50 states and D.C.; refinances also available

Zillow Home Loans makes the most sense for buyers who are deeply embedded in the Zillow platform and want to complete purchase, search, and financing in one ecosystem — especially if they are working with a Redfin agent and can access the 1% rate reduction. Borrowers focused purely on rate and fee minimization should compare at least one nonbank lender and one bank lender directly before choosing Zillow.

NerdWallet Mortgage

NerdWallet is a personal finance platform founded in 2009 that has expanded from editorial content into mortgage comparison and brokerage services. Its 'Mortgage Experts' service pairs borrowers with licensed brokers who help navigate lender selection and the application process — a hybrid between a pure marketplace and a managed-service model. NerdWallet's annual Best-Of mortgage awards (published early each year) are among the most cited rankings in the industry and are based on rates, fees, loan variety, and customer experience metrics. The platform does not originate loans but can be used to compare rates and connect with partner lenders.

- • Annual Best Mortgage Lenders ranking: in-depth editorial ratings updated quarterly covering rates, fees, loan types, and customer experience for 50+ lenders

- • Mortgage Experts service: licensed mortgage brokers available to help compare lenders, check eligibility, and guide the application without an additional fee to the borrower

- • Rate comparison tables: real-time partner lender rate quotes alongside editorial reviews on one page

- • Mortgage calculators and articles: comprehensive educational library covering first-time buyer programs, down payment assistance, FHA vs. conventional, and more

- • Consistent methodology: NerdWallet discloses its rating criteria including HMDA rate data, J.D. Power scores, and customer service testing

NerdWallet is the best comparison starting point for first-time buyers who need both education and rate comparisons in one place. The Mortgage Experts broker service is genuinely useful for borrowers who feel overwhelmed by lender selection. Experienced borrowers who simply want maximum competing offers should also use LendingTree in parallel.

Redfin Mortgage

Redfin Mortgage — formerly Bay Equity Home Loans — was acquired by Rocket Companies when Rocket completed its $1.75 billion purchase of Redfin in July 2025. The Redfin mortgage operation has since been rolled into the Rocket Mortgage brand. Buyers who use a Redfin agent and finance through Rocket Mortgage can choose either a 1% interest rate reduction for the first year of the loan or a lender credit of 0.75% of the loan amount (up to $6,000) at closing. Redfin's real estate listings, agent network, and Rocket's mortgage origination are now integrated on the Redfin platform. Borrowers who click 'Get Financing' on Redfin listings are directed to Rocket Mortgage.

- • Redfin-Rocket integration: the largest real estate brokerage platform and America's largest mortgage lender now operate as a single homeownership ecosystem

- • Preferred Pricing incentive: 1% year-one rate buydown or $6,000 closing credit for buyers combining Redfin agent and Rocket Mortgage financing

- • Redfin Sign & Save: 0.25% cash back for buyers who sign an exclusive buyer agency agreement with a Redfin agent before their second home tour

- • Home search and financing on one platform: saved homes, preapproval, and rate estimates are integrated into Redfin's search experience

- • Redfin Concierge: up to $50,000 line of credit for pre-listing home improvements, with rates from 8.99% to 16.99% (available in most states except NV and MS)

Redfin Mortgage (now Rocket Mortgage) is a compelling package specifically for buyers who are already planning to use a Redfin agent. The 1% year-one rate reduction or $6,000 credit is real money. Buyers who are not committed to a Redfin agent should compare Rocket Mortgage directly alongside two or three additional lenders to ensure they are getting the most competitive rate — the incentive only pays off if Rocket's base rate is also competitive for your credit profile.