30 Best Business Credit Cards for Entrepreneurs in 2026

Business credit cards range from traditional bank-issued rewards cards like Chase Ink and Amex Business Gold to modern corporate charge cards from Brex, Ramp, and Mercury that skip interest entirely. This guide covers 29 active products across rewards cards, fintech spend management platforms, fleet fuel cards, and global expense tools. Pricing was verified against each product's official page in March 2026.

Chase Ink Business Cards

Chase offers four Ink business cards covering every spending style. The Ink Business Preferred ($95/yr) earns 3x points on travel, shipping, and ads on the first $150,000 spent, with a 100,000-point welcome bonus after $8,000 spend. The Ink Business Cash and Ink Business Unlimited both carry no annual fee; the Cash earns 5% at office supply stores while the Unlimited earns 1.5% flat on everything. The Ink Business Premier ($195/yr) earns 2.5% on purchases of $5,000+. All four cards fall under the Chase 5/24 rule, so applicants who have opened 5+ personal cards in 24 months will be denied regardless of credit score.

- • Transferable Ultimate Rewards points: Ink Preferred and Unlimited/Cash (when paired with a Sapphire) allow 1:1 transfers to 14 airline and hotel partners including Hyatt, United, and British Airways.

- • Ink Preferred earns 3x on first $150,000 in travel, shipping, internet, and advertising purchases each account year — categories that match most SMB spend.

- • Ink Business Cash earns 5% on first $25,000 at office supply stores and phone/internet services, plus 2% at gas stations and restaurants each year.

- • No annual fee on Ink Cash and Ink Unlimited makes them viable standalone cards for lean startups or as complements to a premium Chase card.

- • Employee cards: free additional cards with individual spending limits across all four Ink products; fraud liability protection included.

Chase Ink cards are the top pick for small business owners who want travel-grade rewards with a simple annual fee, provided they can clear the 5/24 hurdle. The Ink Preferred is the single strongest SMB rewards card under $100/yr for teams spending heavily on travel and digital advertising. Teams needing expense controls and no revolving balance should look at Ramp or Brex instead.

American Express Business Gold

The American Express Business Gold Card charges a $375 annual fee and earns 4x Membership Rewards points on the top two eligible categories where your business spends the most each billing cycle, chosen automatically from six options: advertising, US media, transit, US gas stations, US restaurants, and US purchases at technology providers. The 4x rate applies to the first $150,000 in combined category spend per calendar year, then 1x. Monthly statement credits up to $20 at FedEx, Grubhub, and US office supply stores (up to $240/yr) and up to $12.95/mo for Walmart+ reduce the effective annual fee significantly. There is no preset spending limit, and balances can be paid over time on eligible purchases.

- • Automatic 4x category selection: Amex tracks your top 2 spend categories each billing cycle from 6 eligible options and applies the bonus rate without any setup.

- • Up to $240 in annual statement credits ($20/mo) on eligible FedEx, Grubhub, and US office supply store purchases — enrollment required.

- • 3x points on flights and prepaid hotels booked directly through amextravel.com.

- • No preset spending limit with Pay Over Time option on eligible purchases; useful for businesses with variable monthly expenses.

- • Employee cards can be added; 200,000-point welcome bonus available for new applicants spending $15,000 in first 3 months (offer varies).

The Amex Business Gold is the strongest mid-tier business rewards card for companies spending $5,000–$12,500/month in concentrated categories. The auto-rotating 4x is genuinely clever and removes optimization friction. If your top spend categories align with the six eligible options and you use the FedEx/Grubhub credits, the effective cost drops to a level that competes with the Chase Ink Preferred.

American Express Business Platinum

The Amex Business Platinum carries an $895 annual fee after a September 2025 refresh that added a $600 hotel credit, boosted Dell credits to $1,150, and raised the fee from $695. The card earns 5x on flights and prepaid hotels through Amex Travel, 2x on eligible purchases of $5,000+, and 1.5x on purchases $5,000+ at US construction, electronics, software, and shipping providers. Statement credits include up to $120/yr in wireless credits, up to $360/yr in Indeed credits, a $250 Adobe credit, access to 1,550+ airport lounges worldwide, and Global Entry/TSA PreCheck reimbursement. Over 200,000 Membership Rewards points are available as a welcome bonus for new applicants spending $20,000 in 3 months.

- • American Express Global Lounge Collection: access to 1,550+ airport lounges in 140+ countries, more lounge access than any other card program as of July 2025.

- • $600 hotel credit ($300 semi-annually) on prepaid Fine Hotels + Resorts or The Hotel Collection bookings through Amex Travel — new as of September 2025 refresh.

- • $1,150 Dell Technologies credit annually (up to $150 direct + $1,000 after $5,000 spend) for hardware and software purchases.

- • 35% flight points back when using Pay with Points for first/business class or your selected airline, effectively reducing redemption cost.

- • No preset spending limit; 5x on flights and prepaid hotels via Amex Travel makes this the highest-multiplier travel card in the Amex business portfolio.

The Amex Business Platinum makes financial sense only for companies spending heavily on travel and software where the credits and lounge access directly match real expenses. For a 5-person startup with occasional travel, the $895 fee is hard to justify versus the Amex Business Gold at $375. For a 50-person company with regular international travel, the lounge access and credits alone can exceed the fee.

Capital One Spark Cards

Capital One offers four main Spark business cards. The Spark Cash earns unlimited 2% cashback with a $95 annual fee (free first year) plus 5% on hotels and rental cars booked through Capital One Business Travel. The Spark Cash Plus is a charge card (pay in full monthly) with a $150 annual fee waived after $150,000 in annual spend, earning the same 2% flat plus a $2,000 welcome bonus after spending $30,000 in 3 months. The Spark Cash Select earns 1.5% with no annual fee. The Venture X Business charges $395 annually and earns 10x on hotels/cars and 5x on flights booked through Capital One, plus a $300 annual travel credit and 10,000 bonus miles on each anniversary. All Spark cards report to business credit bureaus.

- • Unlimited 2% cashback on all purchases with Spark Cash — no category tracking, no spend caps, and rewards never expire for the life of the account.

- • Spark Cash Plus operates as a charge card with no preset spending limit, adjusting based on your payment history and business cash flow.

- • Expense Management tools built into the dashboard for Venture X Business, Spark Cash Plus, and Spark Cash — including QuickBooks, QuickBooks, and Excel export.

- • 5% cashback on hotels and rental cars booked through Capital One Business Travel applies to all Spark cards, stacking on top of base rates.

- • No foreign transaction fees on all four cards, making them viable for international business travel without hidden costs.

Capital One Spark Cash is the go-to for business owners who want to collect 2% on every dollar without any complexity. It outperforms most cashback cards for undifferentiated spend. The Spark Cash Plus makes exceptional sense for businesses spending $150,000+/year, as the annual fee disappears entirely. For businesses that want a travel card, Venture X Business competes with Amex Platinum at $395 but requires heavy use of the Capital One travel portal.

Brex

Brex is a corporate charge card and spend management platform that launched in 2018, primarily targeting startups and tech companies. The Brex card has no annual fee and earns 7x on rideshare, 4x on travel booked through the Brex portal, 3x on restaurants, 2x on recurring software subscriptions, and 1x on all other purchases. Unlike traditional business cards, Brex underwrites based on company cash balance and revenue rather than a founder's personal credit, requiring at least $50,000 in a US bank account for funded startups or $1,000,000 for self-funded businesses. The platform offers three tiers: Essentials (free), Premium ($12/user/month), and Enterprise (custom). In January 2026, Capital One announced an acquisition of Brex, pending regulatory approval.

- • No personal guarantee required: credit limits are set based on company cash balance and investment history, not founder personal credit scores.

- • 7x rewards on rideshare and 2x on recurring software subscriptions — the highest category multipliers available on a no-annual-fee corporate card for startup spending patterns.

- • Instant virtual card issuance with customizable spend limits by employee, vendor, or time period, enabling immediate onboarding of new team members.

- • AI-powered automated expense management on all tiers including receipt matching, policy enforcement, and accounting field mapping to QuickBooks, NetSuite, and Xero.

- • Brex Treasury: integrated cash management with competitive yield on idle balances, positioning Brex as a primary financial hub rather than just a card provider.

Brex remains the strongest corporate card for venture-backed startups with $50K+ in the bank who want premium rewards without touching personal credit. The no-personal-guarantee structure is a genuine differentiator from every traditional bank card. However, the Capital One acquisition announcement adds meaningful uncertainty, and Ramp now offers comparable automation at zero cost with a simpler 1.5% flat cashback structure.

Ramp

Ramp launched in 2019 as a corporate charge card built around the premise of helping companies spend less rather than rewarding them for spending more. The platform is free for all users and earns 1.5% cash back on every purchase with no annual fee, no foreign transaction fees, no late fees, and no interest charges since balances are due in full monthly or daily depending on account standing. Ramp requires a minimum $25,000 in a US business bank account and is available only to corporations, LLCs, and LPs. In February 2025, Ramp launched Ramp Treasury, a cash management feature earning 4.3% APY on idle balances. Ramp Plus costs $15/user/month ($12/user/month on annual billing) for advanced automation features like custom expense policies and auto-lock cards.

- • 1.5% unlimited cash back on every purchase with zero fees — no annual fee, no foreign transaction fee, no late fee, no interest charges ever.

- • AI-powered duplicate subscription detection: Ramp analyzes vendor payments and flags redundant SaaS tools, helping companies eliminate waste before it compounds.

- • Real-time expense controls at the card level: set per-transaction limits, block specific categories, and auto-enforce policies without manual review after the fact.

- • Ramp Treasury: earn 4.3% APY on idle cash with no minimum balance or lock-up period — treats the card as a financial hub rather than just a payment tool.

- • 86% faster book-closing per Ramp's own customer data, driven by automated receipt matching, accounting sync, and AI-categorization across QuickBooks, NetSuite, and Xero.

Ramp is the single best corporate card for incorporated US businesses that want zero-cost automation and straightforward 1.5% cashback without any fee surprises. It is especially compelling when the AI-driven savings and Treasury yield are factored in alongside the flat cashback. For businesses that need to carry a balance or want category-specific high multipliers, traditional bank cards are a better fit.

BILL Divvy Corporate Card

The BILL Divvy Corporate Card is a no-annual-fee charge card integrated with the BILL Spend & Expense platform (formerly Divvy, rebranded September 2023). The card offers up to 7x rewards at restaurants and 5x on hotels — but only if you pay your balance weekly. Monthly-billing customers earn much lower rates: 1–2x on most categories. Credit lines range from $1,000 to $5,000,000 based on revenue and cash balance, with a minimum $20,000 in business cash typically required for approval. Personal credit score of 670 or higher is recommended. The BILL Spend & Expense software is free with no per-user fees; BILL's separate AP/AR products cost $49–$89/user/month if needed.

- • Payment-frequency rewards: earn up to 7x on restaurants and 5x on hotels when paying weekly, dropping to 1–2x on monthly billing — a unique structure that rewards cash-flow discipline.

- • Budget-level controls: divide your credit line into department or project budgets with granular user-level limits, more granular than most corporate card platforms.

- • Unlimited physical and virtual cards for all employees with no per-card fee, plus no limit on the number of budgets that can be created.

- • Real-time transaction visibility with an integrated mobile app rated 4.8 stars from 16,200+ reviews — same-day spend visibility for managers and approvers.

- • Credit line from $1,000 to $5,000,000 with a simple online application; approval based on revenue, cash balance, and bank account history rather than just credit score.

BILL Divvy's rewards structure is among the most compelling in corporate cards — if and only if your team can consistently pay weekly. For businesses with strong cash flow and a finance team willing to manage the payment cadence, the 7x restaurant rate is genuinely exceptional. For everyone else, the rewards drop sharply on monthly billing and the complexity makes it hard to justify over Ramp's simpler model.

Airbase (now Paylocity for Finance)

Airbase was a leading procure-to-pay platform before being acquired by Paylocity in October 2024 for $325 million. The combined product, now branded Paylocity for Finance, integrates Airbase's spend management capabilities — corporate cards, expense management, accounts payable automation, and procurement — with Paylocity's HCM platform. Pricing has historically started at approximately $5–8/user/month for the Standard plan, rising for more complex AP and procurement workflows. Airbase won recognition as the leading procure-to-pay platform for mid-market on G2 for multiple years, serving 500+ clients primarily in the 100–5,000 employee segment. The Paylocity acquisition unlocks integrated payroll-to-card workflows for existing Paylocity HCM customers.

- • Unified procure-to-pay: purchase requests, PO matching, vendor onboarding, invoice processing, and payment all flow through a single platform without switching tools.

- • Smart physical and virtual cards: pre-built spend controls and approval workflows mean cards auto-enforce policies rather than relying on after-the-fact expense reports.

- • Oracle NetSuite, Sage Intacct, and QuickBooks integrations with deep two-way sync — unlike lighter fintech cards that offer read-only exports.

- • Accounts payable automation: automated invoice processing, PO matching, and multi-step approval routing reduces invoice-to-payment time significantly.

- • Paylocity HCM integration (post-acquisition): new hire card provisioning, offboarding card deactivation, and payroll-aligned spend visibility for HR and finance teams.

Airbase/Paylocity for Finance is the right choice for mid-market companies (100–2,000 employees) that need to move beyond cards and basic expense reports into true procure-to-pay automation. The AP depth and ERP integrations are genuinely best-in-class for this segment. Smaller companies should start with Ramp; larger enterprises with more complex needs should also evaluate SAP Concur and Coupa.

Stripe Corporate Card

The Stripe Corporate Card is a charge card available to businesses that use Stripe for payment processing. The card is entirely free — no annual fee, no foreign transaction fees, no late fees, and no interest (balances must be paid in full monthly). Cardholders earn 2% cashback in their top two spending categories, automatically calculated by the system. Spending $5,000 on the Stripe Corporate Card unlocks $50,000 in free transaction processing on the Stripe platform. Credit limits are based on Stripe payment processing volume rather than personal credit scores. Virtual cards are available instantly upon approval; physical cards arrive within a few days.

- • 2% cashback in your top two spending categories, automatically identified by Stripe — no manual category selection or enrollment required.

- • Credit limits based on Stripe payment processing volume and business history, not personal credit score — suitable for high-revenue businesses with thin personal credit.

- • Free processing credit: $5,000 in card spend unlocks $50,000 in waived Stripe transaction fees, a significant value for e-commerce businesses.

- • Deep Stripe platform integration: card spend syncs natively with Stripe Dashboard, invoicing, and financial reports without third-party connectors.

- • Instant virtual card issuance with no paperwork beyond having a Stripe account — one of the fastest onboarding paths in the corporate card market.

The Stripe Corporate Card is an excellent secondary or primary card for businesses already processing payments through Stripe. The zero-fee structure and processing credit create real value for e-commerce companies, and the 2% auto-category cashback is competitive. For any business not on Stripe, there is no reason to consider this card over Ramp or Mercury, both of which offer comparable or better programs.

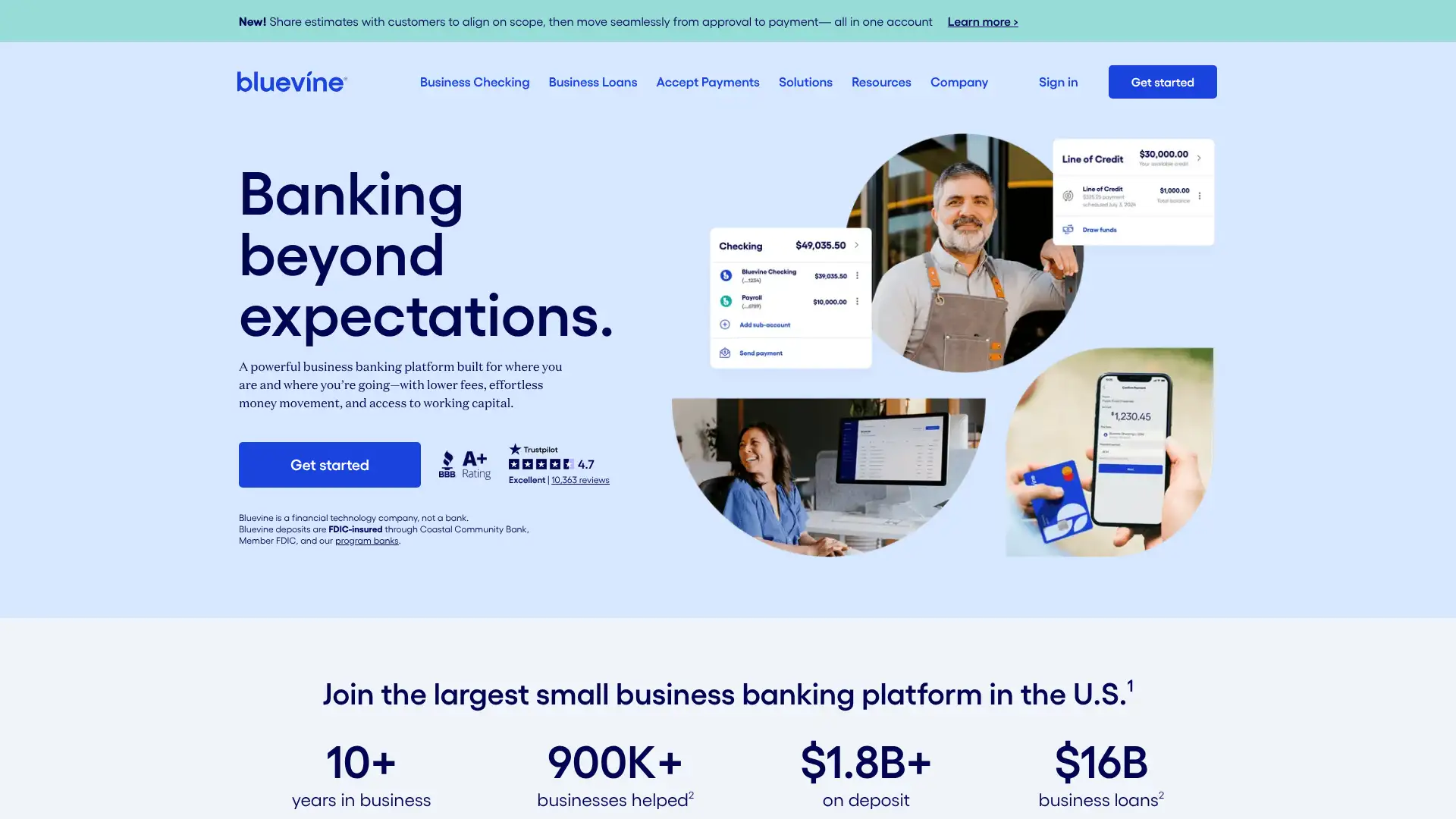

Bluevine Business Cashback Mastercard

The Bluevine Business Cashback Mastercard is a credit card available exclusively by invitation to eligible Bluevine Business Checking customers. It launched in general availability in June 2024. The card earns 1.5% unlimited cashback on all business purchases with no annual fee and no rewards caps. A 2% cashback rate is available to cardholders maintaining a Bluevine checking account balance of $5,000 or more. The card can be managed from the same Bluevine dashboard used for checking, deposits, and invoicing. QuickBooks Online integration is available for syncing card data to accounting software. Mastercard Easy Savings provides automatic rebates at thousands of merchants.

- • Up to 2% cashback on all business purchases for cardholders maintaining $5,000 or more in their Bluevine Business Checking account — making the checking-card combo the most valuable configuration.

- • No annual fee, no rewards cap, and no category restrictions — every business purchase earns the same rate regardless of merchant or spending category.

- • Unified Bluevine dashboard: manage checking, credit card, invoicing, and line of credit (up to $250,000) from a single platform without switching between apps.

- • Mastercard Easy Savings: automatic rebates at thousands of merchants including fuel, hotels, and dining — applied without enrollment or redemption steps.

- • Employee cards with individual spend limits and virtual card support for immediate team onboarding, with QuickBooks Online sync for accounting reconciliation.

The Bluevine Business Cashback Mastercard is a solid no-fee card for existing Bluevine banking customers who want to consolidate their financial tools. The 2% rate with a $5K balance is genuinely competitive, but the invitation-only model and checking balance requirement limit its accessibility. For businesses not already banking with Bluevine, Ramp or Mercury offer comparable cashback without the balance requirement.

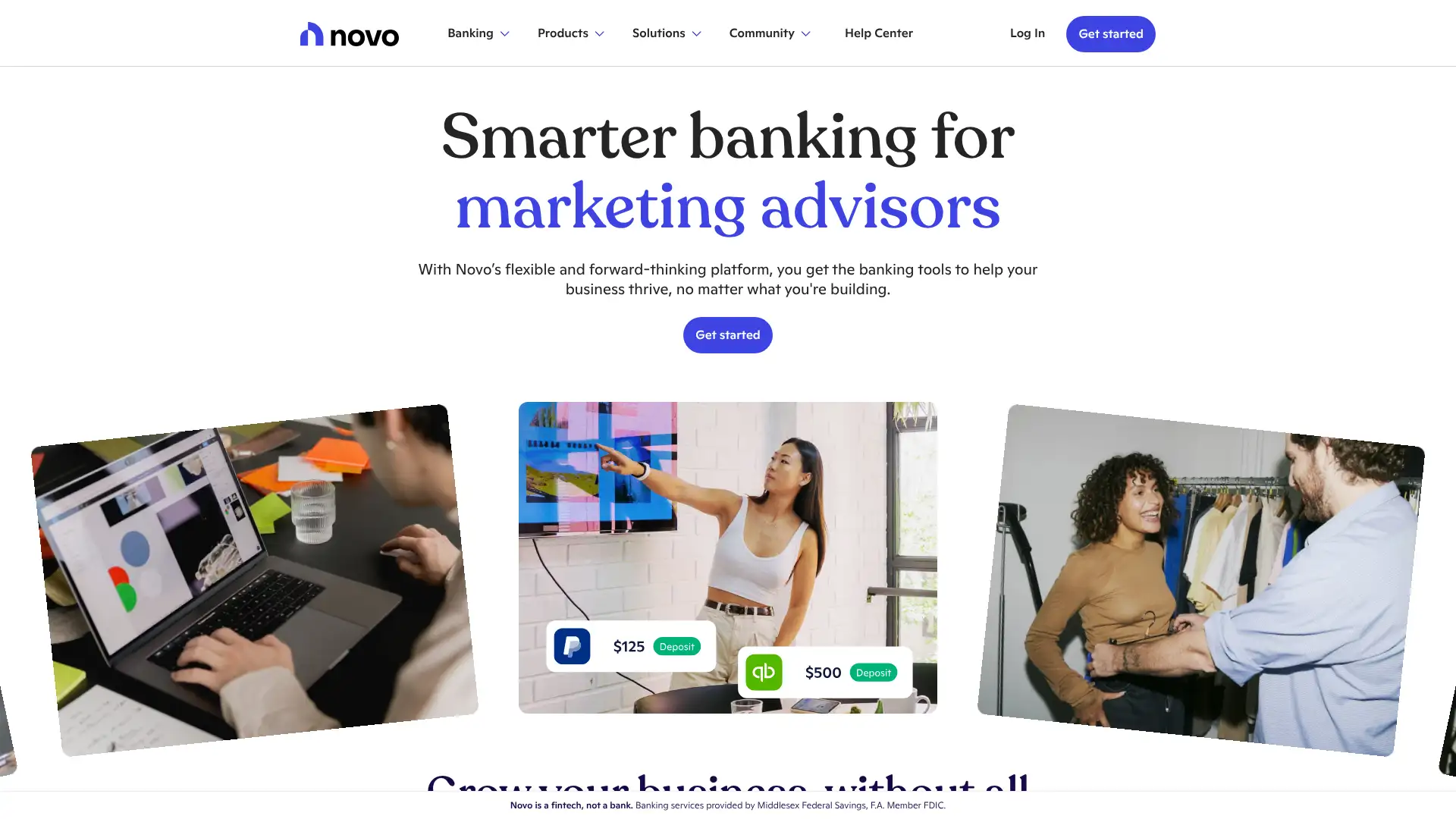

Novo Business Credit Card

Novo's Business Credit Card, issued by Continental Bank pursuant to a Mastercard license, offers up to 2% cashback on all eligible purchases for accounts maintaining a $5,000+ Novo checking balance, dropping to 1% for balances under $5,000. There is no annual fee and no rewards cap. The card is available to select Novo customers through invitation only and is managed from the same Novo dashboard used for checking, bookkeeping, and invoicing. Novo serves over 250,000 customers and is backed by banking services from Middlesex Federal Savings. The card includes Mastercard Business Card perks such as auto-rental collision damage waiver, extended warranty, and various partner discounts including Slack and Budget car rental.

- • Up to 2% cashback on all eligible business purchases when Novo checking balance is $5,000 or more; 1% cashback with a balance under $5,000 — no category restrictions or caps.

- • Single-dashboard management: credit card, checking, bookkeeping with AI-powered expense categorization, invoicing, and Reserves savings all in one Novo interface.

- • Mastercard business perks including Mastercard Easy Savings (automatic merchant rebates), digital wallet support, and fraud monitoring with real-time alerts.

- • AI-powered expense categorization and tax preparation tools built into the Novo platform reduce end-of-year bookkeeping time for sole proprietors and small teams.

- • Partner discounts with Slack, Dropbox, Zoho, Booking.com, and more, accessible directly through the card — adding value beyond standard cashback.

The Novo Business Credit Card is a strong complementary product for small business owners already committed to the Novo banking ecosystem. If you maintain a $5,000+ balance anyway, the 2% cashback rate with no fee is excellent. However, the invitation-only model and balance-linked rate structure make it less accessible than Ramp's straightforward 1.5% flat cashback with no balance requirement.

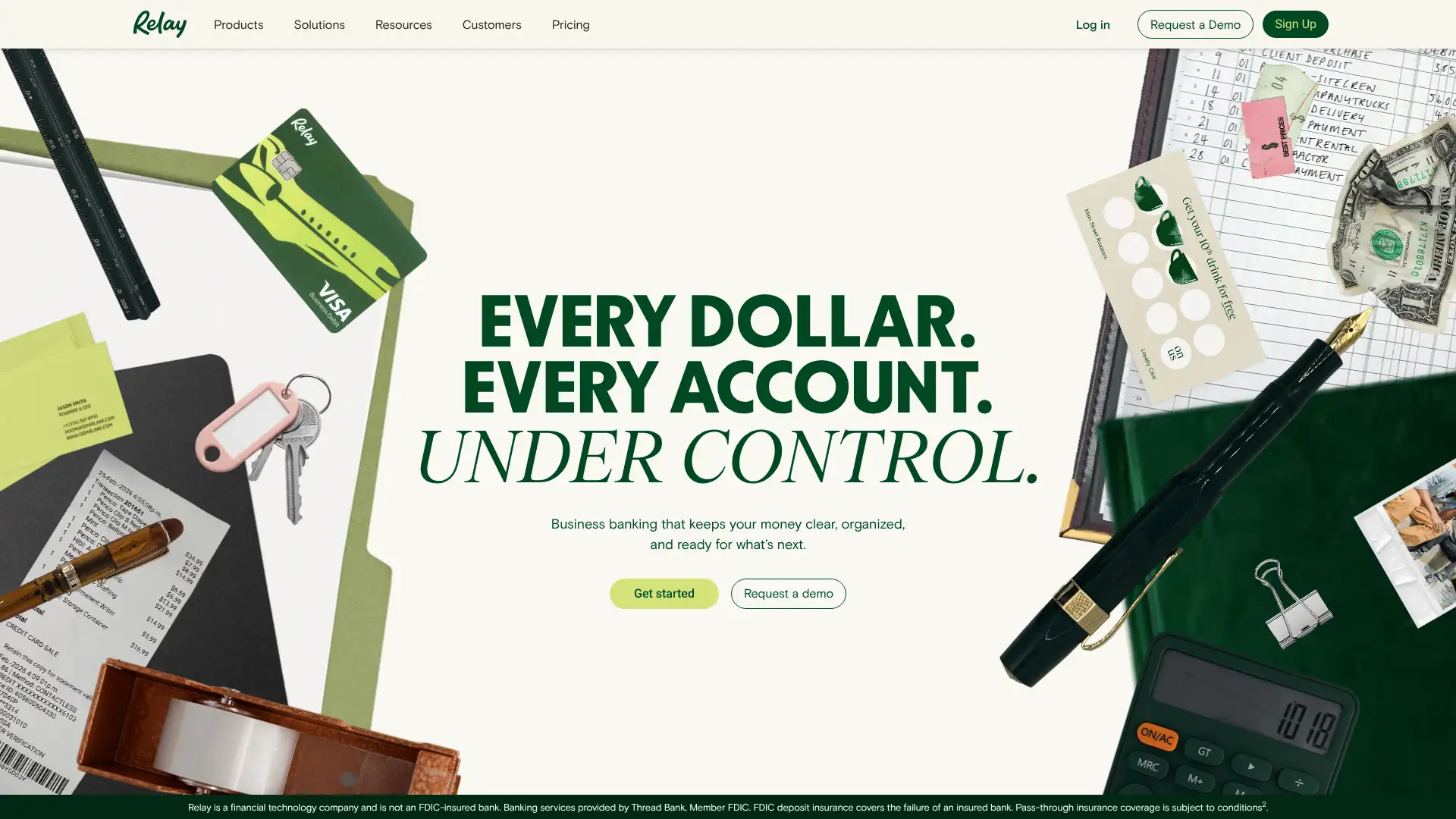

Relay Visa Credit Card

Relay is an online banking platform used by 60,000+ small businesses, specifically popular among Profit First practitioners who need multiple checking accounts to allocate revenue across expense buckets. The Relay Visa Credit Card launched in September 2024 and is available by invitation to eligible Relay customers (businesses in operation for at least 1 year, not sole proprietors, with $240,000+ annual revenue). The card charges no annual fee, earns 1.5% cashback on all purchases, and automatically pays the full balance at the end of each 30-day billing cycle from the connected Relay checking account. There is no ability to carry a balance; a 3% late fee applies to unpaid balances. Relay has three banking plans: Starter (free), Grow ($30/mo), and Scale ($90–120/mo).

- • Automatic monthly pay-in-full: the Relay credit card debits your Relay checking account at the end of each billing cycle, eliminating the risk of carrying revolving debt and interest charges.

- • 1.5% cashback on all credit card purchases with no category restrictions — cashback is credited to the connected Relay checking account.

- • Up to 20 checking accounts and 50 debit/credit cards per business: ideal for businesses using envelope budgeting or Profit First methodology with separate accounts for tax, payroll, and operating expenses.

- • Receipt capture with SMS reminders: every transaction triggers an automated text reminder to upload a receipt, building a receipt archive without manual follow-up.

- • QuickBooks Online and Xero integration on Grow and Scale plans with automated expense categorization, reducing month-end reconciliation time.

Relay's credit card is a logical extension for small businesses already committed to the Relay banking platform, especially those using Profit First or multi-account cash management. The auto pay-in-full structure is disciplined and the 20-account banking model is genuinely unique. The eligibility restrictions (1+ year, $240K revenue, no sole proprietors) keep it out of reach for the smallest businesses.

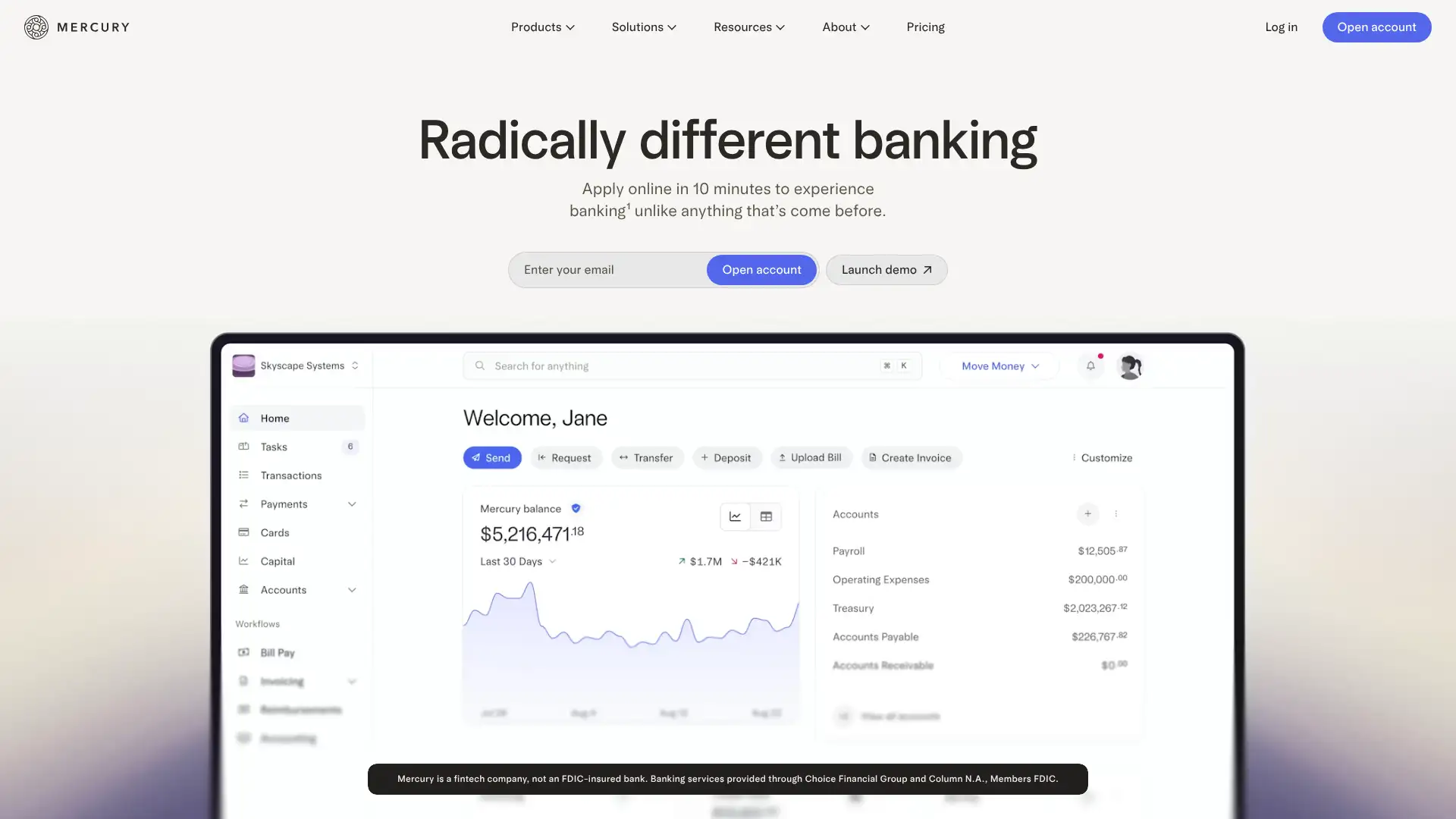

Mercury IO Card

Mercury is a banking platform for startups with 80,000+ business customers. The IO Card, issued by Patriot Bank (Member FDIC) pursuant to a Mastercard license, is Mercury's corporate credit card offering 1.5% cashback on all purchases with no annual fee, no personal credit check, and no personal guarantee. As of October 2025, Mercury expanded IO access to eligible companies from day one of opening a Mercury account, removing the previous $50,000 minimum balance requirement for initial access — though balances still influence credit limits. Daily repayment terms apply to new accounts with lower balances; monthly repayment unlocks at $15,000 in Mercury account balances. Foreign transaction fees apply on non-USD transactions.

- • Day-one access: eligible companies can now get an IO card immediately upon opening a Mercury account, no prior balance required — a major accessibility improvement from the previous $50K threshold.

- • 1.5% cashback automatically deposited into the Mercury account when the balance is paid — no manual redemption, no points, no portal login required.

- • Credit limit based on Mercury account balances and external bank accounts (linkable as of October 2025) — higher balances unlock higher limits without a personal credit check.

- • Unlimited virtual cards with customizable monthly limits for vendors, subscriptions, and teams, plus one physical card per employee.

- • Google Workspace integration: invite new team members and their IO cards are provisioned automatically — a significant time-saver for growing distributed teams.

Mercury IO is the most accessible no-personal-guarantee corporate card for very early-stage startups, now that day-one access has been unlocked. The combination of free banking, instant IO card, automatic 1.5% cashback, and business credit reporting makes it a strong all-in-one choice for founders who want simplicity. As the company grows and needs richer expense controls or higher category rewards, Brex or Ramp become more compelling.

Wallester Business

Wallester is an Estonian-licensed fintech and official Visa Principal Member founded in 2018, serving businesses across the EEA, UK, UAE, Singapore, USA, and Canada. The Wallester Business platform issues instant virtual and physical Visa cards tied to IBAN accounts, supports 10 currencies with zero-fee conversion between internal accounts, and integrates with accounting tools via a REST API. The Free tier includes 300 virtual cards and unlimited physical cards with no monthly fee, making it exceptionally accessible for growing teams. Wallester processes cards in EUR, USD, GBP, SEK, NOK, CZK, HUF, RON, PLN, and DKK, covering most major European currencies.

- • 300 free virtual Visa cards on the free tier, with zero-fee real-time currency conversion across 10 supported currencies — ideal for teams paying international vendors.

- • Visa Principal Member status: Wallester issues cards directly on the Visa network, providing near-perfect acceptance rates and faster transaction processing than indirect issuers.

- • Tokenization for Apple Pay, Google Pay, Garmin Pay, and Fidesmo Pay — all cards can be added to digital wallets immediately upon issuance.

- • REST API access for ERP, CRM, and accounting integration: bulk card creation, automated limit adjustments, and real-time data export to Xero, QuickBooks, or Sage.

- • Multi-currency IBAN accounts: hold and spend in EUR, USD, GBP, and 7 other currencies without currency conversion fees on internal transfers.

Wallester Business is the strongest free option for European companies that need large numbers of virtual cards for subscription management, vendor payments, or distributed teams. The 300-card free tier, instant issuance, and zero-fee currency conversion are genuinely best-in-class for the price. Companies that need rewards or a richer expense management workflow should evaluate Pleo or Payhawk.

Jeeves

Jeeves is a global financial platform founded in 2019, backed by $380 million from Andreessen Horowitz, CRV, Tencent, and Y Combinator. It operates as a corporate charge card and expense management platform in 30+ countries including the US, Canada, UK, EU, Mexico, Colombia, and Brazil. The Jeeves card earns 1% cashback on all purchases, operates with no monthly fees and no personal guarantee, and issues unlimited virtual and physical cards. Cross-border payments reach 150+ countries in 40 currencies. Card rails vary by region: Visa-powered in some markets (issued by Celtic Bank via Stripe in the US), Mastercard in Canada, and local rails elsewhere. Jeeves has raised $380 million to fuel international expansion and serves 3,000+ companies globally.

- • Cards in local currencies for 30+ countries: Jeeves issues cards denominated in local currency (USD, CAD, GBP, EUR, MXN, BRL, COP, and more) in each supported market.

- • Cross-border payments to 150+ countries in 40 currencies, with same-day settlement between North America and LATAM — typically faster than SWIFT wire transfers.

- • 1,300+ airport lounge access via LoungeKey for cardholders — a premium perk rarely included on no-fee corporate cards.

- • Up to 5% yield on multi-currency cash balances held in the Jeeves account, making idle funds productive for companies with international treasury needs.

- • Expense management included at no cost: receipt capture via mobile app, QuickBooks and Xero integration, and AI-powered bill payment with multi-language invoice scanning.

Jeeves is the strongest option for multinational startups and growth companies that genuinely operate across North America, LATAM, and Europe simultaneously. No competitor matches its breadth of local currency cards across emerging markets. For US-only or primarily European businesses, Ramp, Brex, or Payhawk deliver more value with better support and clearer pricing.

Tribal Credit

Tribal Credit is a corporate charge card and expense management platform targeting SMBs and startups in Mexico, Colombia, Brazil, Canada, the US, UK, and the EU. Founded in 2019 and backed by investors including Andreessen Horowitz and Stanford University alumni networks, Tribal offers credit cards on Visa and Mastercard networks with up to 90 days of credit on purchases — one of the longer repayment windows in the market. Tribal Pay (formerly called bill pay) extends credit for vendor payments at a 3.37% fee on balances utilized over 60 days. The platform offers virtual and physical cards with no annual fees or monthly software fees, and cardholders can earn up to 4% cashback on travel and 1% on other purchases. It targets the 100–5,000 employee segment in markets where traditional bank credit is difficult to access.

- • Up to 90 days of credit on card purchases — significantly longer than the standard 30-day charge card cycle, providing more cash flow flexibility for businesses with slower-paying clients.

- • Tribal Pay: use credit to pay local and international vendors at 3.37% for balances over 60 days — effectively a short-term credit facility for AP without a traditional bank loan.

- • Multi-currency card support with local cards issued in Mexico, Canada, Colombia, Brazil, UK, EU, and US — covering the broadest LATAM presence of any corporate card.

- • Unlimited virtual cards with one-time or recurring-use settings; each subscription or vendor can have a unique card number, limiting fraud exposure.

- • Up to 4% cashback on travel bookings through Tribal Travel (Expedia alliance) and 1% on all other card spend.

Tribal Credit is the strongest corporate card option for startups and SMBs based in LATAM or operating across Mexico, Colombia, and Brazil where other fintech cards have limited local presence. The 90-day credit window and local currency issuance are unique. For US-based businesses, Ramp or Brex provide superior features at comparable or lower cost.

Pliant

Pliant is a Berlin-based corporate credit card fintech founded in 2020, an EU-licensed e-money institution and Visa Principal Member. It serves 3,500+ businesses across Germany, Austria, and wider Europe with physical and virtual Visa credit cards — a genuine revolving credit line rather than a prepaid card, distinguishing it from platforms like Wallester or Pleo. Pliant offers two physical card tiers: black Visa Platinum Business cards and premium metal Visa Infinite Business cards with airport lounge access. Cashback rates vary by repayment frequency, and multi-currency support covers 11 currencies. Pricing has three tiers: Starter (up to 25 users, €0 per user), Premium (~€5/user/month), and Enterprise (custom). Black physical cards cost approximately €30/month each on lower plans.

- • Genuine Visa credit card (not prepaid): Pliant extends real credit lines, supporting hotel and rental car reservations that require credit cards as holds — critical for frequent business travelers.

- • Visa Infinite Business metal cards with worldwide airport lounge access, comprehensive travel insurance, and extended warranty — the highest tier in Visa's business portfolio.

- • Cashback on all transactions at rates varying by repayment frequency, with partner bonus cashback on IT equipment, hotel, and office supply categories.

- • Multi-currency billing in 11 currencies with competitive FX rates; separate billing cycles can be set for different card groups or legal entities.

- • Integration with Circula, Datev, Lexoffice, Microsoft Dynamics 365, and other German accounting tools — strong localization for DACH market workflows.

Pliant is the top choice for German and Austrian businesses that need real Visa credit cards — not prepaid — combined with strong local accounting software integrations. The Visa Infinite Business metal card is genuinely premium for European travel. The per-physical-card fees need careful calculation for larger teams to avoid cost surprises.

Payhawk

Payhawk is a London-headquartered spend management platform founded in 2018, serving 1,500+ companies across the UK, Europe, and the US. The platform issues Visa Commercial cards (both credit and debit) and provides expense management, invoice processing, bill payment, and procurement — all as a single subscription. Payhawk issues cards in 7 currencies (GBP, EUR, USD, BGN, RON, DKK, PLN) with FX rates of 1.99% on other currencies. The Summer 2025 release added AI-powered expense notes that auto-suggest descriptions for transactions, saving early access customers 45 hours across 17,000 automated notes. Pricing in the UK starts at £149/month for a 24-month contract for companies under 20 employees; per-user pricing starts at approximately €10/seat/month for the Pro plan (minimum 8 seats) and €15/seat/month for Premium (minimum 12 seats).

- • Cards in 7 currencies with local IBAN accounts in GBP and EUR — free local payments within each supported currency, with 1.99% FX on other currencies.

- • AI Office of the CFO: AI agents for financial control, travel, procurement, and payments launched in 2025 — automates expense notes, anomaly detection, and budget tracking.

- • Multi-entity support: manage cards, expense policies, and approval workflows across separate legal entities from a single Payhawk dashboard — essential for holding companies.

- • Carbon emission tracking: automatically calculates Scope 3 emissions per transaction, enabling ESG reporting directly from card spend data.

- • 50+ HRIS integrations (Hibob, Deel, Personio, BambooHR, ADP, Workday) — new hire card provisioning and leavers' card deactivation triggered automatically.

Payhawk is the top choice for European companies in the 50–500 employee range that need multi-entity management, multi-currency cards, and integrated expense automation in one platform. The AI features and HRIS integrations add genuine operational value. For very small teams or companies under 20 employees, the minimum seat pricing is less competitive than Pleo or Spendesk.

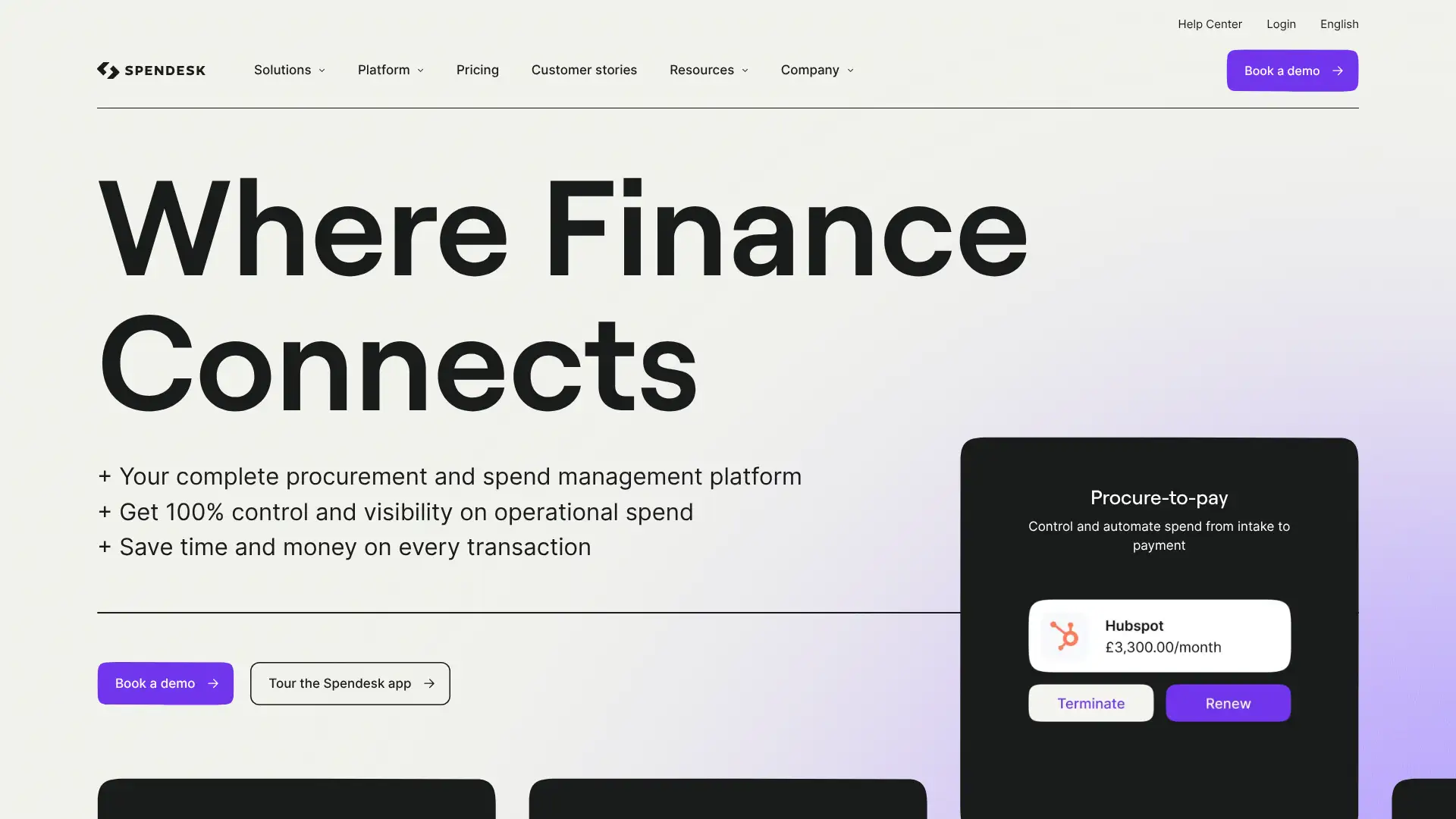

Spendesk

Spendesk is a Paris-based spend management platform founded in 2016, trusted by 20,000+ business users including SoundCloud, Doctolib, and Deezer. The platform processes €20 billion annually and was the first European solution to fully integrate procurement and spend management into a single workflow. Spendesk offers company cards (physical and virtual), automated invoice handling, approval workflows, and budgeting. The pricing model was updated in 2025 to a base platform fee covering unlimited cards, users, and control settings — moving away from per-user pricing. The exact platform fee is custom-quoted and requires a demo. ISO 27001:2022 certified, PCI-DSS and GDPR compliant. Customers report 5% annual cost reduction through better spend visibility.

- • Unlimited users, cards, and transactions on a flat platform fee — no per-seat charges that make scaling expensive as headcount grows.

- • First European platform to integrate procurement and spend management: purchase requests, PO matching, invoices, vendor payments, and card expenses all in one workflow.

- • AI-powered expense management: automatic receipt validation, OCR invoice capture, and spend allocation reduce manual finance team work.

- • 700,000+ businesses on the Spendesk network benefit from automated smart matching of invoices and card transactions — reducing month-end reconciliation effort.

- • Native integrations with Datev, Sage, QuickBooks, NetSuite, Xero, and custom export tools; ISO 27001 and PCI-DSS certified infrastructure.

Spendesk is the most mature all-in-one spend management platform for European SMBs with 50–1,000 employees who need genuine procurement-to-payment workflows. The unlimited users model is particularly attractive for scaling companies. The lack of public pricing is a real friction point for buyers who want to evaluate cost before scheduling a demo.

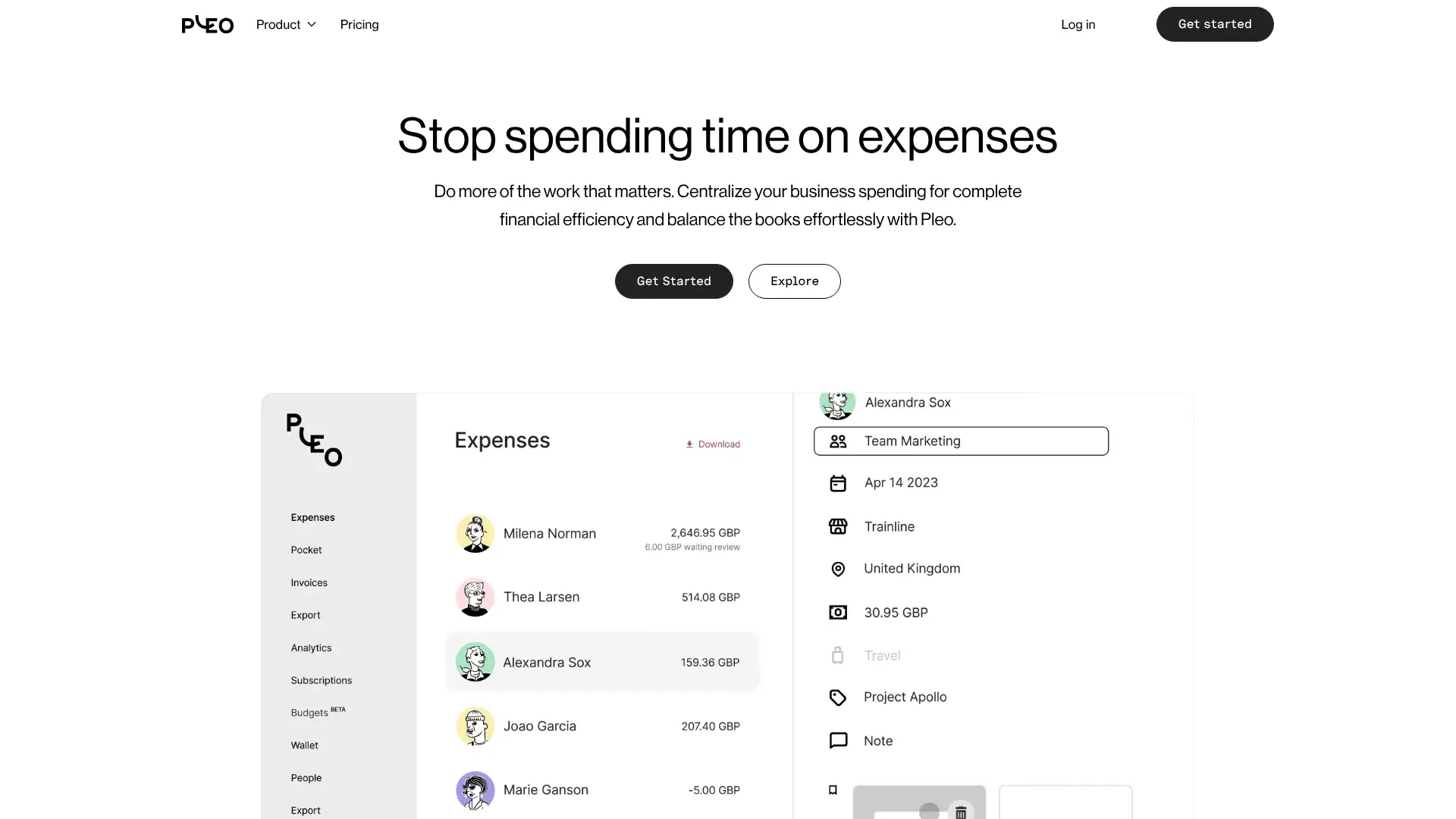

Pleo

Pleo is a Copenhagen-founded business spending platform trusted by 37,000+ companies across 14 European countries including Denmark, Sweden, Germany, Spain, Ireland, UK, France, and the Netherlands. It provides physical and virtual Mastercard expense cards with automated bookkeeping, invoice management, and reimbursements. Unlike Wallester or Spendesk, Pleo positions itself as a complete end-to-end spending experience. The Starter plan is free. Essential costs $39/month (billed annually) for 3 users plus $11/additional user; Advanced costs $89/month for 3 users plus $14.50/additional user; Beyond costs $179/month for 5 users plus $17.50/additional user. Cashback ranges from 0.5% to 1% on card spend, capped at the monthly plan fee.

- • Automatic receipt-fetching from email inboxes: Pleo scans connected email accounts to find matching receipts for card transactions, reducing the need for manual uploads.

- • Mileage calculator: automatically calculates fuel costs for car journeys based on distance and rate, simplifying HMRC-compliant mileage claims for UK businesses.

- • Direct employee reimbursement: link employee bank accounts for instant reimbursement of out-of-pocket expenses, eliminating the traditional monthly expense report cycle.

- • 50+ accounting integrations including Xero, QuickBooks, Sage, Billy, Visma, Datev, and Microsoft Dynamics — covering most major European accounting platforms.

- • Centralized invoice management: process, approve, and pay supplier invoices from the same platform used for expense cards.

Pleo is the strongest entry point for European SMBs that want a polished, modern expense management experience with a free tier to start. It's especially well-suited for teams of 5–30 employees in the UK, DACH, and Nordics. As headcount grows past 30, per-user costs make Spendesk or Payhawk increasingly more cost-effective.

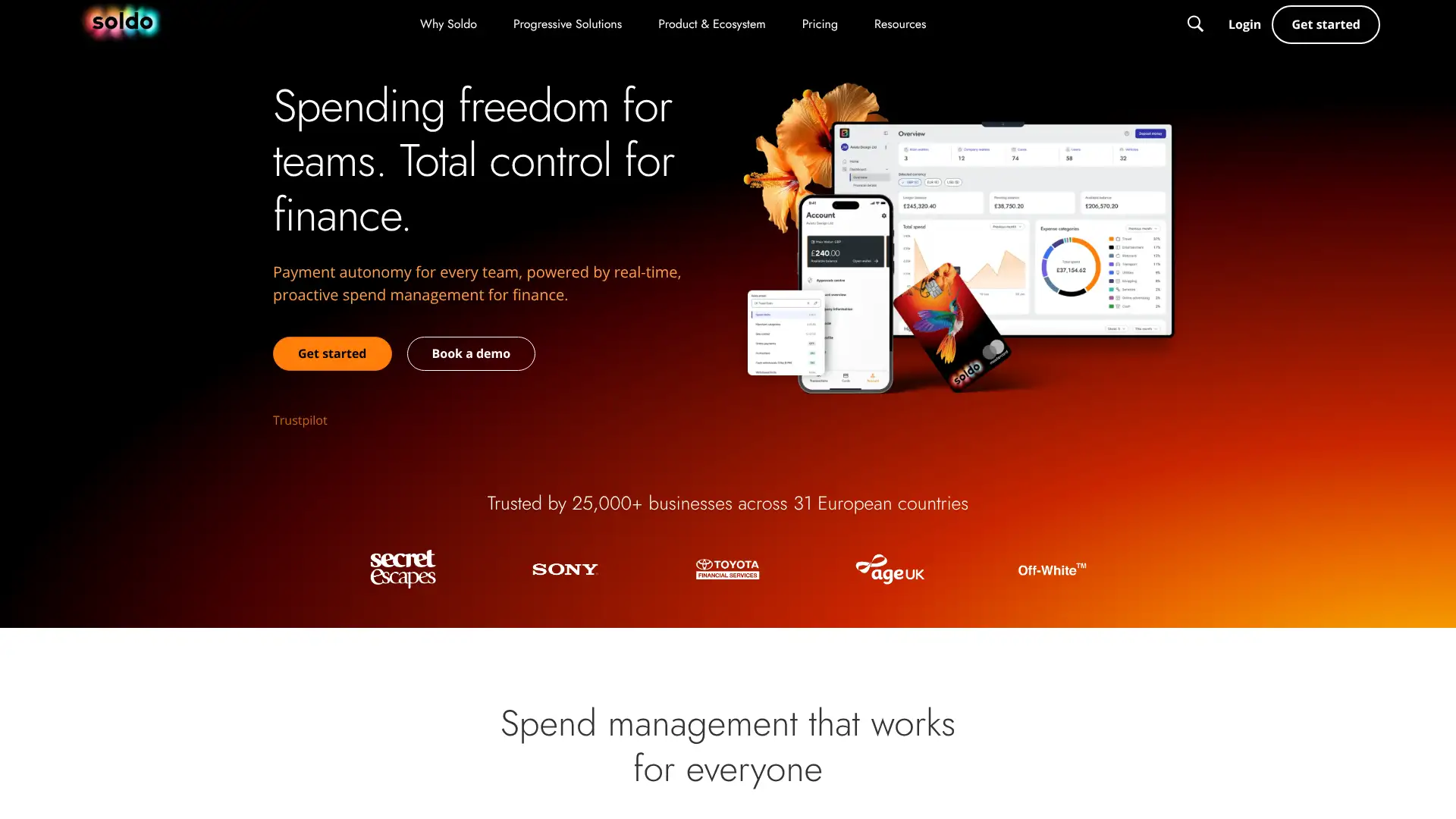

Soldo

Soldo is a UK-based spend management platform founded in 2015 by Carlo Gualandri, used by 26,000+ businesses including Sony, Age UK, and Off-White. It provides prepaid Mastercard cards (not credit cards) linked to an expense management platform with multi-level budget controls. Cards can be issued in GBP, EUR, or USD. The Standard plan starts at £21/month (ex-VAT) for 3 users and 20 cards; the Plus plan adds multi-currency wallets, advanced reporting, and more wallet controls. The Unlimited plan is enterprise-priced. Soldo does not offer a free plan but runs 30-day trials on Standard and Plus. A 1% FX fee applies on transactions made in a currency not matching the card denomination.

- • Multi-level wallet controls: assign separate wallets to teams, projects, or departments with auto top-up rules — more granular than most corporate card controls.

- • Cards in 3 currencies (GBP, EUR, USD) with the ability to issue multi-currency cards for international teams, reducing FX costs for cross-currency EU purchases.

- • Prepaid card structure means funds are ring-fenced before spending — employees can only spend what has been loaded, eliminating credit risk and overspend at the platform level.

- • Accounting integrations with QuickBooks, Xero, Sage, NetSuite, and SAP; Soldo's direct Xero integration is particularly deep and highly rated by UK accountants.

- • Subscription cards and online ad cards: special-use virtual cards with auto-renewal tracking and cancellation reminders for recurring vendor payments.

Soldo is a reliable, well-established choice for UK and European SMBs that prefer prepaid cards over credit cards and need detailed wallet-level budget controls. Its Xero integration is particularly strong for UK accountants. US businesses or companies needing broader global coverage should look at Payhawk or Jeeves instead.

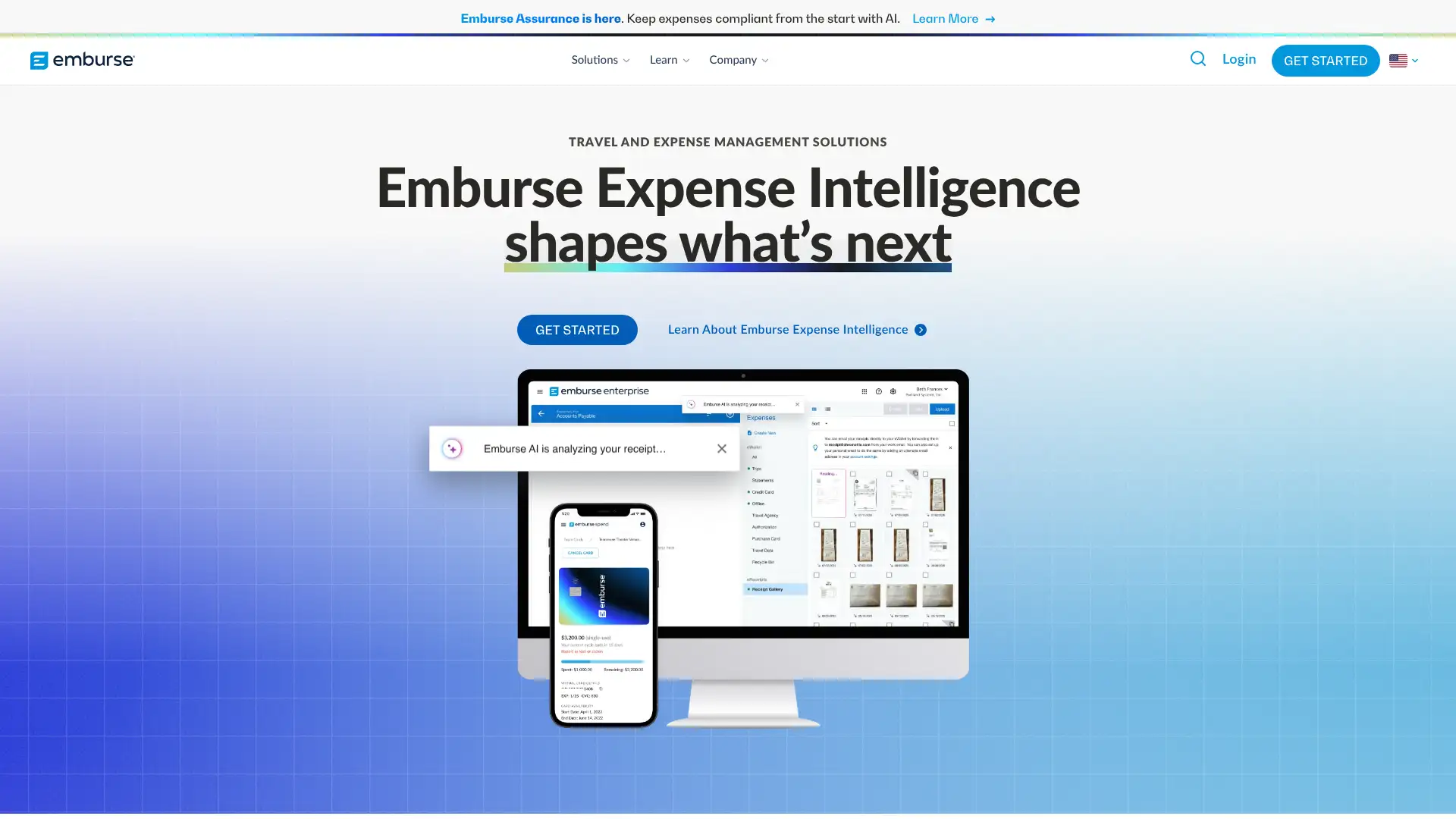

Emburse

Emburse is a travel and expense management platform that merged multiple acquired companies (including Certify, Chrome River, and Nexonia) into a unified brand. Emburse Spend is its primary SMB product, starting at $8/user/month, combining expense management with Emburse Cards — virtual and physical prepaid cards with granular spending rules. The card program allows companies to issue cards instantly, set per-card limits, restrict merchant categories, and auto-reconcile receipts with QuickBooks, NetSuite, Sage Intacct, and Xero. A 1% cash rebate is available when qualifying spend volumes are met. Emburse Spend includes a 30-day free trial. Only US-incorporated businesses (Inc., LLC, or Partnership) are eligible.

- • Virtual and physical prepaid cards with self-enforcing spending rules: card-level controls block unauthorized categories automatically at point of sale rather than flagging after the fact.

- • Transaction-based expense submission: employees submit each expense at the time of the transaction rather than in monthly batches, enabling same-day reimbursement rather than waiting for cycle end.

- • Native integrations with QuickBooks Online and Desktop, Oracle NetSuite, Sage Intacct, and Xero; custom export tools cover most other major ERPs.

- • 1% cash rebate on eligible Emburse Cards spend when qualifying volume thresholds are met — offsetting the software subscription cost for higher-spending companies.

- • Guided onboarding with weekly live demo calls and an optional implementation specialist add-on; no IT resources required for standard deployment.

Emburse Spend is a practical mid-market choice for US SMBs that want to move beyond shared corporate credit cards and manual expense reports without paying enterprise prices. The $8/user starting point is competitive and the integrated prepaid cards solve receipt reconciliation effectively. For businesses that want cashback rewards or revolving credit, a traditional bank card paired with Ramp's free expense tools offers more value.

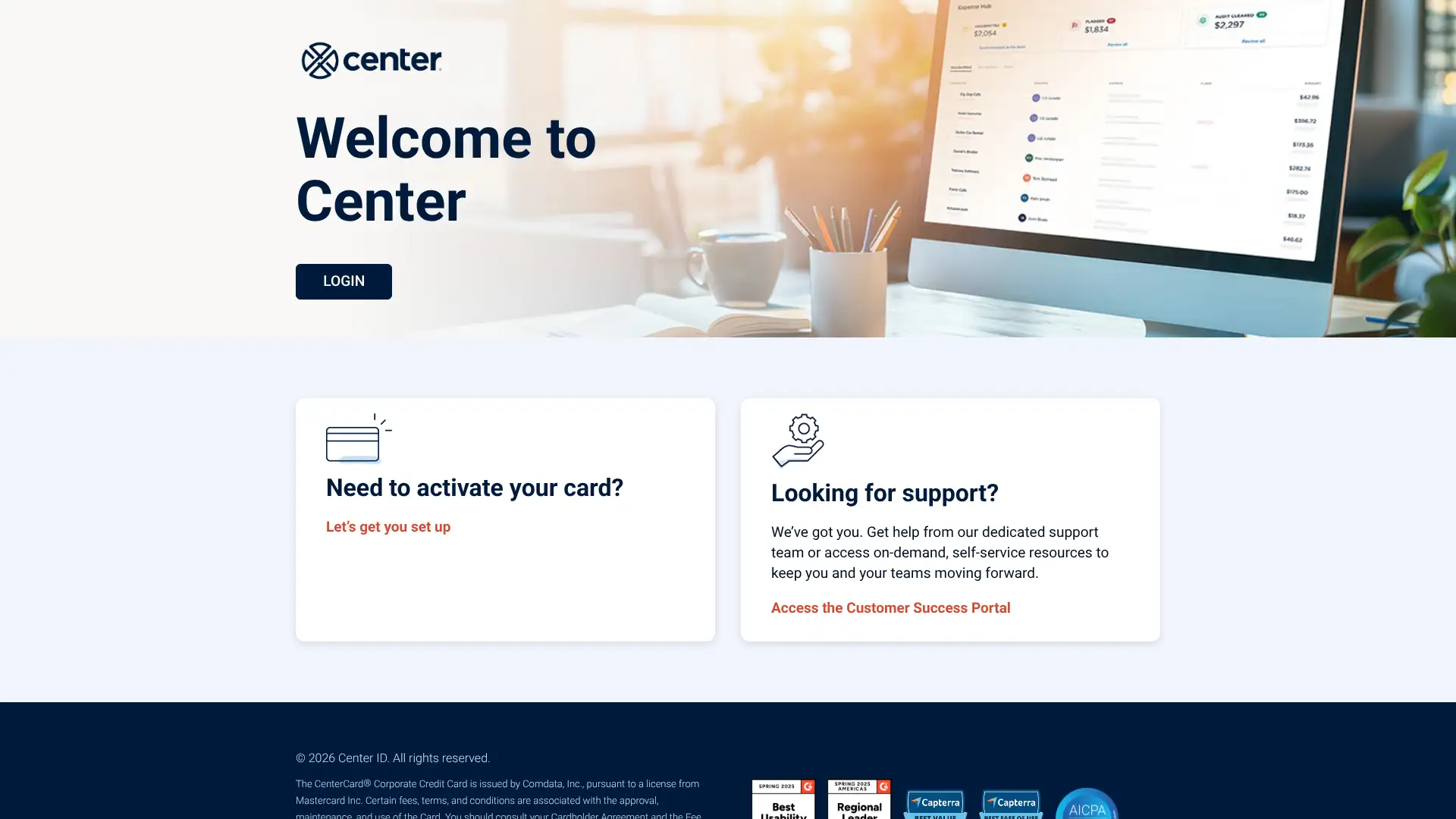

CenterCard

CenterCard is a corporate Mastercard and expense management platform headquartered in Bellevue, Washington. Unlike subscription-based competitors, Center uses a usage-based pricing model funded entirely by interchange fees — the software is completely free to use. The platform targets mid-size companies (typically 50–500 employees) in the US and Canada and includes a mobile app for receipt capture, corporate travel booking, and real-time expense management. Customers like 1-800-PACK-RAT report 85% reductions in reconciliation time, and Clearwater Construction cut credit card charge processing time by 40%. Integrations include NetSuite, Sage Intacct, and major ERPs; each customer receives a dedicated deployment manager.

- • Zero-cost software model: Center earns revenue from Mastercard interchange fees rather than software subscriptions, making the entire platform — including corporate cards, travel booking, and expense management — free to the customer.

- • Real-time spend capture: every CenterCard swipe triggers an instant mobile prompt for the employee to snap a receipt and categorize the expense, eliminating month-end expense report marathons.

- • Policy enforcement at point of purchase: spend controls are applied as transactions happen, blocking out-of-policy purchases before they occur rather than flagging them in reports.

- • Dedicated deployment manager for every customer — a high-touch onboarding experience that is standard, not an add-on, regardless of account size.

- • Integrated corporate travel booking: employees can book flights, hotels, and rental cars within policy directly from the CenterCard app, capturing all travel spend in one platform.

CenterCard's free, interchange-funded model makes it an exceptional value for mid-size US and Canadian companies that want enterprise-grade expense management without a software budget. The dedicated deployment manager and real-time capture are standout features. The mobile app quality issues and lack of API access are legitimate concerns for tech-forward finance teams who need deep integrations.

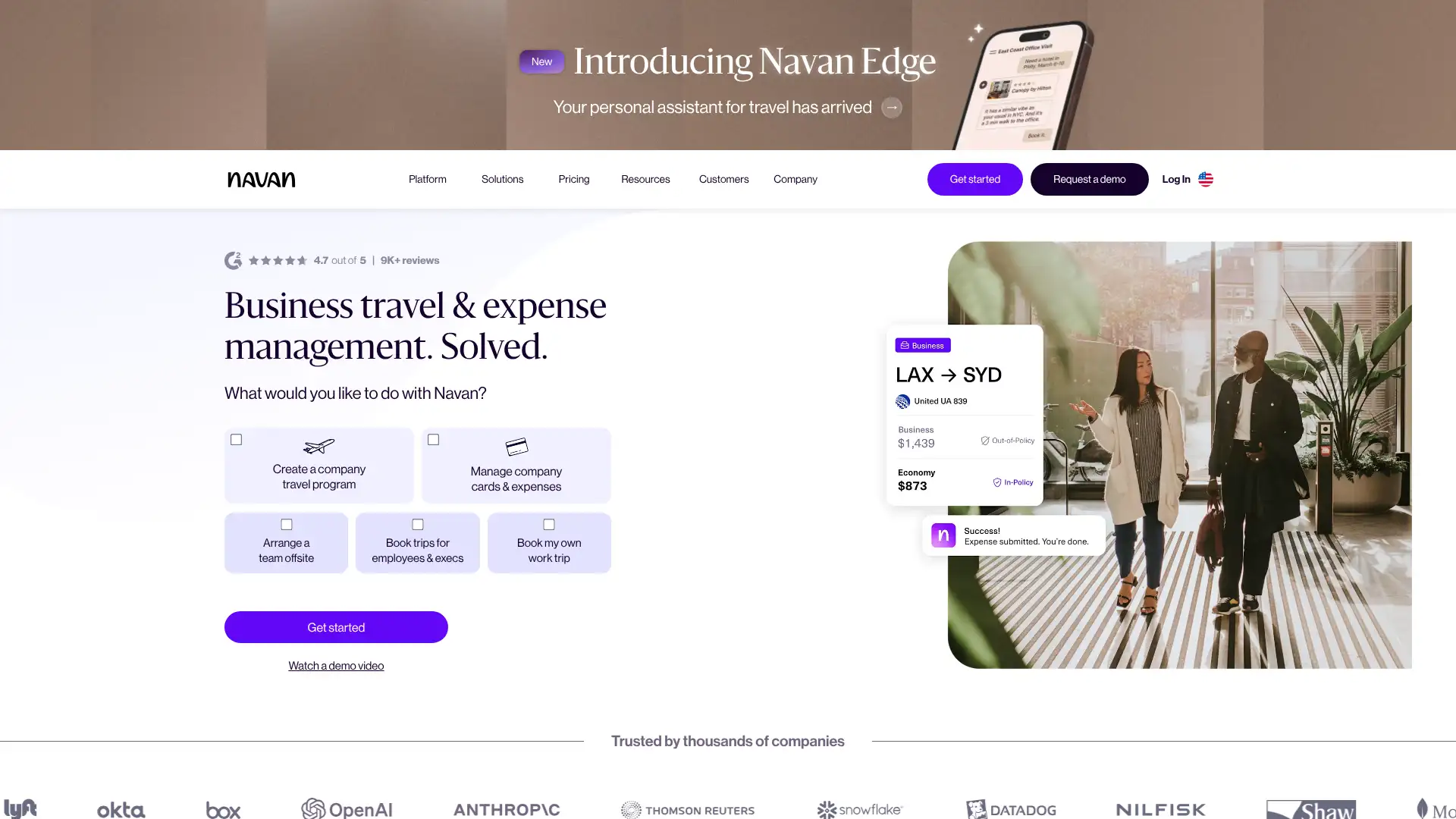

Navan

Navan (formerly TripActions) is an all-in-one travel management and expense platform serving 10,000+ companies globally. It combines flight, hotel, car, and rail booking with expense management and the Navan Corporate Card (up to 1.5% cashback, no annual fee) or Navan Connect (works with existing Visa/Mastercard/Amex cards). The platform is free for companies under 200 employees for core travel and expense features; expense management costs $15/user/month for the first 5 users (free) and scales with additional users. Navan went public on Nasdaq (NAVN) in October 2025. A 2025 Forrester Total Economic Impact study for a composite 5,000-employee organization found 376% three-year ROI and 16% average travel savings.

- • Navan Rewards: employees earn up to $100 personal travel credit per booking when they choose options below budget — company-funded incentive program that makes compliance automatic and voluntary.

- • Integrated travel inventory: flights, hotels, cars, and trains from negotiated corporate rates alongside public fares, covering 700+ airlines and millions of hotel properties.

- • Navan Corporate Card: 1.5% cashback on all purchases with no annual fee; or Navan Connect to keep existing corporate cards while using Navan's expense automation.

- • AI-powered policy enforcement: custom travel policies (max hotel rates by city, advance booking requirements, approved airlines) are applied automatically at booking, not after the fact.

- • 24/7 travel support with Ava AI assistant resolving 54% of support interactions automatically as of November 2025; human agents available when AI cannot resolve.

Navan is the top all-in-one choice for companies with meaningful travel budgets (over $10,000/month in travel spend) that want to consolidate booking, expense, and card management into one platform. The free tier for under-200-employee companies makes it an easy first step. For companies without heavy travel programs, Ramp's free expense automation with 1.5% cashback delivers more ROI at lower cost.

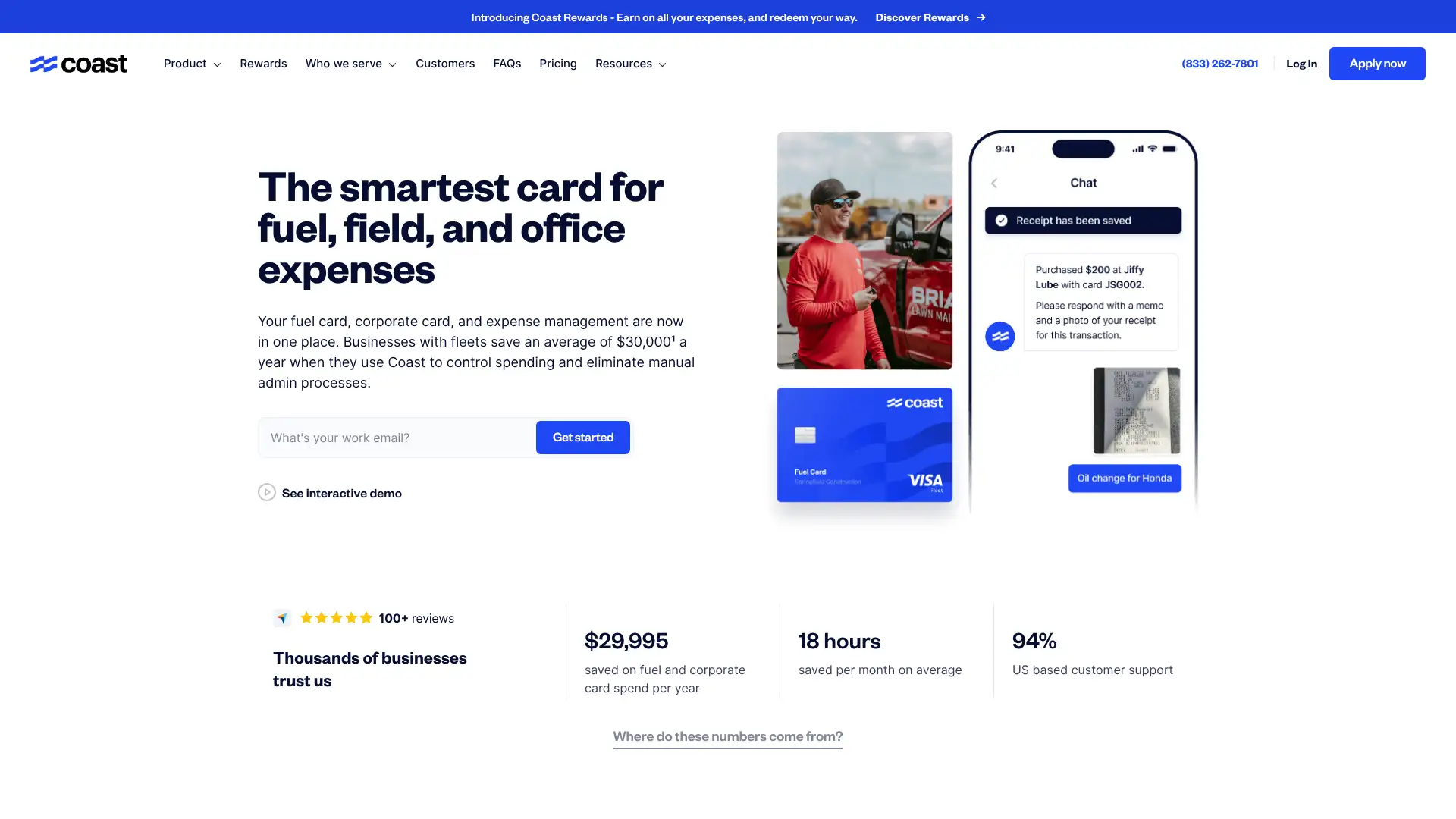

Coast

Coast is a Visa fleet card and expense management platform founded in 2020 that operates differently from traditional fleet cards: instead of a closed network, it accepts everywhere Visa is accepted — covering 99% of US fuel stations. The pricing is transparent at $4/active user/month (charged only for users with at least one transaction). Rebates range from 3¢ to 9¢ per gallon at 30,000+ Coast partner stations (including Exxon, Circle K, and 7-Eleven), plus 1% cash back on non-fuel fleet expenses like tires, oil changes, and maintenance. Security uses SMS card unlock instead of a PIN, requiring drivers to text a unique code before authorizing fuel purchases — significantly reducing fraud. Customers report average annual savings of $30,000 for fleets of 10+ vehicles.

- • Universal Visa acceptance: drivers can fuel at any Visa-accepted station — no restricted network, no detours, and no 'no available station' situations common with closed-loop fleet cards.

- • SMS card unlock security: drivers text a verification code before each fuel purchase, reducing fuel fraud through a layer that can't be cloned or skimmed like a PIN pad.

- • GPS auto-decline: transactions are automatically blocked when the vehicle GPS does not match the station location, catching unauthorized card use without manual review.

- • Real-time reporting and analytics: Coast surfaces patterns like vehicles getting worse mileage or employees consistently overspending, automatically flagging them without manual report-building.

- • Telematics integrations with Samsara, Geotab, Verizon Connect, and others for two-way data sync — odometer readings auto-populate from telematics, eliminating manual entry.

Coast is the best fleet card for businesses that need universal fuel station access, transparent pricing, and modern fraud prevention. The SMS security model is genuinely superior to PIN-based authorization for preventing unauthorized use. Fleets primarily fueling at Pilot, Flying J, or TA Petro truck stops will find better per-gallon rebates from WEX or Comdata.

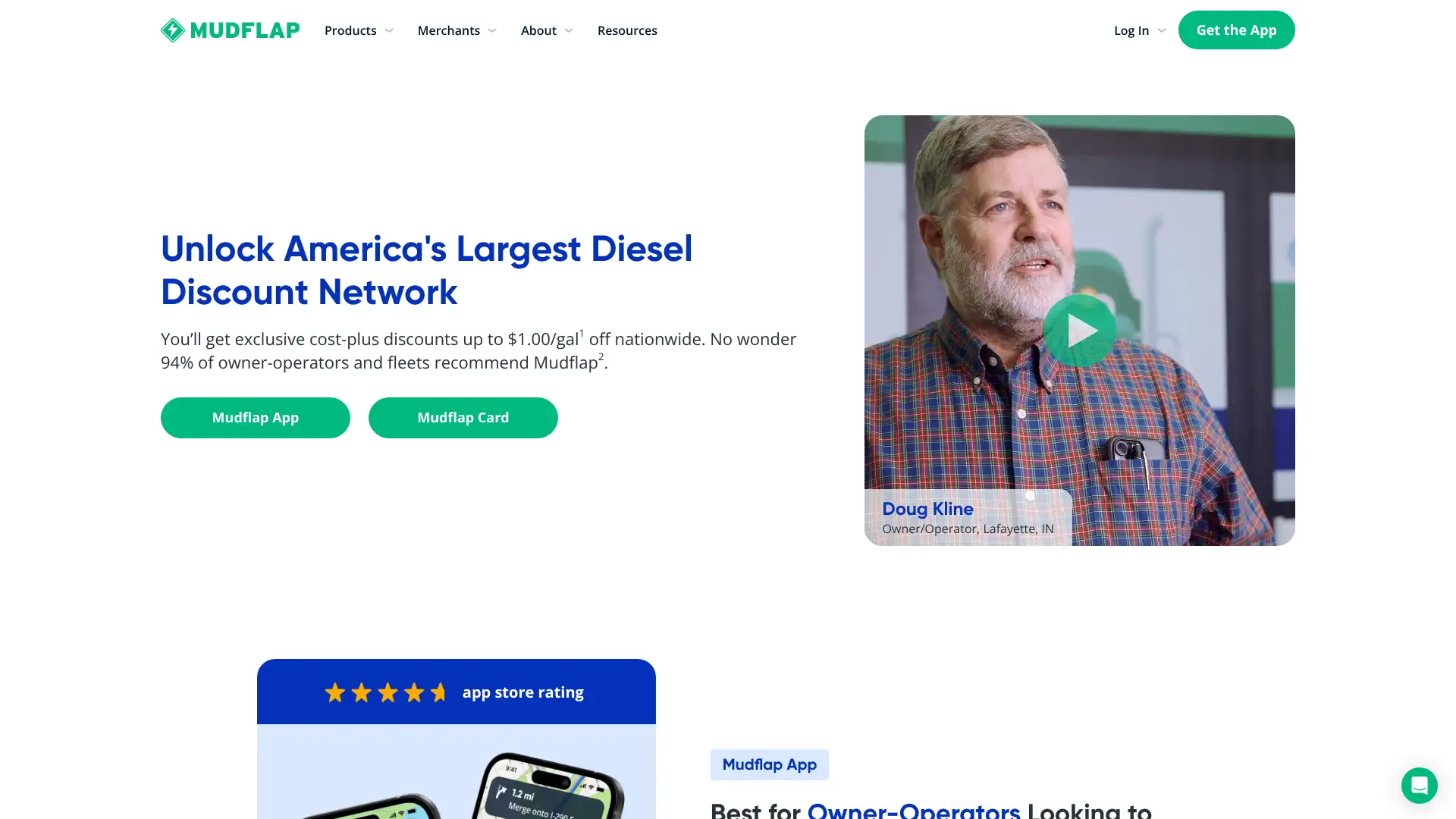

Mudflap

Mudflap started in 2020 as a mobile app helping independent truckers find diesel discounts at partner truck stops, growing to 515,000+ drivers by 2025. The Mudflap Fleet Card, issued by Celtic Bank via Visa, is the company's formal card product for fleets, launched in 2023. The card has zero annual fees, zero monthly card fees, and zero setup fees — the only charges are late payment fees (3–6% of the delinquent balance). The card earns up to $1 off per gallon at 3,500+ Mudflap network truck stops (including Kwik Trip, Road Ranger, and AMBEST) with an average saving of 57¢/gallon in the Midwest between May–July 2024, plus a 2¢/gallon rebate at all other Visa-accepted locations. Businesses must be registered corporations or LLCs to apply; sole proprietors using the Mudflap app can access discounts through their personal debit card without the fleet card.

- • Up to $1 off per gallon at 3,500+ Mudflap partner truck stops — the largest potential per-gallon discount of any fleet card reviewed; average savings of 57¢/gallon in the Midwest.

- • Zero-fee structure: no monthly fees, no per-transaction fees, no portal fees — the only fee is a late payment penalty, making this the most cost-effective fleet card in the market.

- • Mudflap app integration: use the app to pre-lock discounted prices up to 24 hours in advance; app navigation routes drivers to the cheapest Mudflap stop along their route.

- • Fleet management dashboard: set daily or weekly spending limits, restrict by spend category, add and remove drivers instantly, and download IFTA-friendly reports.

- • Telematics-powered controls: confirm vehicle is near the station and tank capacity matches gallons purchased before authorizing each transaction.

Mudflap is the single best fleet card for owner-operators and small OTR trucking fleets whose drivers can consistently route through Mudflap's independent truck stop network. The zero-fee structure and average 57¢/gallon savings are compelling for diesel-heavy operations. Large fleets that depend on Pilot/Flying J, Love's, or TA Petro stops need WEX or Comdata instead.

Corpay (Corpay One)

Corpay is a global S&P 500 corporate payments company offering commercial card programs and AP automation to businesses of all sizes. The Corpay One Mastercard is its SMB-focused charge card — no monthly fee, no annual fee, 1.5% cashback on eligible purchases paid through the Corpay One platform (1% on other expenses), and a personal guarantee required from the cardholder. For larger enterprises, Corpay's commercial card program offers customized rebate structures negotiated based on spend volume, with account managers and dedicated implementations. Cards are issued by Fifth Third Bank or Regions Bank pursuant to Mastercard licenses. There is no minimum card count for SMBs; large fleet and procurement card programs are built to enterprise specifications.

- • Rebate structure negotiated on enterprise programs: Corpay works with large companies to maximize cashback on AP and procurement card spend, potentially exceeding standard fixed rates on high-volume accounts.

- • Daily monitoring and proactive alerts: Corpay monitors transactions daily rather than monthly, catching fraud and policy violations far earlier than end-of-month statement review.

- • MCC (Merchant Category Code) spend controls: block specific categories or limit to approved vendors at the card level — standard for fleet and procurement card programs.

- • Multi-issuer choice: Corpay One cards are issued by Fifth Third Bank or Regions Bank, both regulated FDIC institutions with strong SMB banking infrastructure.

- • 100+ integrations including NetSuite, Sage, QuickBooks, and Microsoft Dynamics; Corpay's AP automation handles invoice processing, PO matching, and payment routing.

Corpay is a solid choice for US businesses that want an institutional-grade corporate card program backed by FDIC bank issuers. The enterprise commercial card programs offer real value for high-volume spenders through custom rebates. For SMBs, the personal guarantee and per-transaction fees on the Corpay One card make Ramp's free charge card a more attractive starting point.

Comdata Fleet Cards

Comdata is one of the largest and oldest fleet payment providers in North America, offering fuel and expense cards for commercial trucking and fleet operations. The Comdata Card (proprietary fleet) and Comdata Mastercard Fleet provide access to pre-negotiated fuel discounts at 8,000+ truck stops, including Love's, Pilot/Flying J, TA/Petro, and thousands of independents. For small fleets (20 or fewer vehicles), Comdata offers up to 40¢ off per gallon on diesel at TA Petro and 8¢ at Pilot/Flying J and Love's. Monthly fees are approximately $8/card/month (higher than Coast and WEX), reflecting Comdata's broader back-office fleet management services including IFTA filing, cash loading, and scales. The Comdata OnRoad Mastercard provides universal card acceptance for non-fuel fleet expenses.

- • 8,000+ truck stop network including all major chains (Love's, Pilot/Flying J, TA/Petro) — the most comprehensive closed-loop network in trucking fleet cards.

- • Up to 40¢ off per gallon on diesel at TA Petro for small fleets — the highest specific network discount available, exceeding WEX's 15¢ maximum at comparable locations.

- • ICD (iConnectData) portal: real-time fleet management dashboard with card ordering, fuel purchase summaries, spending limits, and invoice downloads — purpose-built for carrier operations.

- • Integrated IFTA reporting and tax filing support — reduces the quarterly IFTA filing burden for carriers with multi-state fuel purchases, a requirement Comdata handles natively.

- • Comdata OnRoad Mastercard: dual-function card that allows drivers to access company funds and personal funds from one card, managing advances, fuel, and maintenance from a single account.

Comdata's 40¢/gallon discount at TA Petro and 8,000-location network make it the strongest choice for large OTR trucking fleets where maximizing per-gallon savings at the highest-volume stops justifies the higher monthly card fee. For smaller fleets or mixed light-duty operations, the $8/card fee becomes hard to justify versus Coast's $4 or Mudflap's free tier.

WEX Fleet Cards

WEX Inc. (formerly Wright Express) is one of the largest fleet payment companies globally, processing over $45 billion in transactions annually and serving 600,000+ businesses. The WEX Fleet Card is the company's primary small business offering — accepted at 95% of US fuel stations and 45,000 service locations. Rebates range from 3¢ to 15¢ per gallon within the WEX EDGE Savings Network, plus 1¢–3¢ per gallon everywhere else. The WEX FlexCard allows businesses to carry a monthly balance rather than paying in full. Fees are approximately $2–4/card/month based on volume; WEX does not publish a standard fee schedule publicly. As of 2025, WEX has expanded into EV charging through WEX EV Solutions covering 150,000+ public charge points — the only fleet card provider with this level of EV integration.

- • 95% US fuel station acceptance across all Visa-accepted locations — the broadest coverage of any fleet card, including major grocery store gas stations that Comdata's network misses.

- • WEX EDGE Savings Network: exclusive discounts on tires, hotels, wireless service, and fuel beyond just the pump — providing non-fuel savings that compound with rebates.

- • WEX EV Solutions: access to 150,000+ public EV charge points under the same card and reporting dashboard as ICE fuel purchases — the only fleet card with integrated EV charging at this scale.

- • ClearView analytics platform: spend pattern analysis, driver behavior monitoring, and fuel efficiency tracking with configurable reporting across the entire fleet.

- • Fleet SmartHub mobile app and WEX Connect app allow drivers to locate the cheapest nearby stations and managers to monitor transactions in real time.

WEX is the most versatile fleet card in the market — wide acceptance, EV integration, and proven scale make it a safe default for mixed fleets and companies transitioning to electric vehicles. The lack of public pricing is a legitimate frustration. Large trucking fleets focused purely on diesel savings at major truck stops will often find better per-gallon economics with Comdata; smaller fleets with straightforward needs should evaluate Coast's more transparent pricing.

SVB Innovator Card

Silicon Valley Bank (SVB), a division of First-Citizens Bank since its acquisition in March 2023, offers the SVB Innovator Card — a corporate charge card purpose-built for technology, life sciences, and healthcare startups. The card earns unlimited Membership Rewards-style points with no cap, redeemable for travel, Apple devices, and cash back, plus a revenue share option for high-spending clients. The balance must be paid in full each month (charge card structure). Credit limits are scalable based on startup stage and SVB banking relationship rather than personal credit alone. SVB Innovator Card includes AI-powered mobile expense reporting and T&E management tools. SVB banks 60% of Forbes Fintech 50 companies and 40% of Forbes AI 50 companies as of 2025, reflecting its depth in the innovation economy.

- • Scalable credit from pre-seed to Series B+: SVB underwrites based on startup stage, investor backing, and banking relationship — early-stage companies can qualify before they have revenue.

- • Revenue share option: high-volume clients can opt for cash-back revenue share rather than points, turning card spend directly into operating income.

- • AI-powered T&E expense management built into the card — real-time transaction capture, receipt storage, and reporting without needing a separate expense platform.

- • No personal guarantee required in most cases: SVB evaluates the company's financial profile and banking relationship rather than relying primarily on founder personal credit.

- • Integration with SVB's broader financial ecosystem — startup banking, venture debt, and the Innovator Card are all managed through the same SVB relationship manager.

The SVB Innovator Card is the strongest choice for venture-backed tech and life sciences startups already banking with SVB that want a charge card with scalable limits and rewards matched to startup spending patterns. For startups not banking with SVB, Brex and Mercury offer comparable no-personal-guarantee charge cards with more transparent pricing and no banking relationship requirement.